Vous aimerez peut-être aussi

- Case 25 Star River Electronics LTDDocument8 pagesCase 25 Star River Electronics LTDHenry Rizqy0% (1)

- Harley DavidsonDocument8 pagesHarley DavidsonQuyen Tran ThaoPas encore d'évaluation

- Group-13 Case 12Document80 pagesGroup-13 Case 12Abu HorayraPas encore d'évaluation

- Coming Home Funeral Services: Ericsson Internal - Mar 15 - Page 1Document3 pagesComing Home Funeral Services: Ericsson Internal - Mar 15 - Page 1KaranSinghPas encore d'évaluation

- The Boeing Company Financial Analysis - 3Document33 pagesThe Boeing Company Financial Analysis - 3Marina LubkinaPas encore d'évaluation

- Kasus 1 - Flinder Valves and Controls IncDocument6 pagesKasus 1 - Flinder Valves and Controls IncChitaraniKartikadewiPas encore d'évaluation

- Jacobs Division PDFDocument5 pagesJacobs Division PDFAbdul wahabPas encore d'évaluation

- Case 32 - CPK AssignmentDocument9 pagesCase 32 - CPK AssignmentEli JohnsonPas encore d'évaluation

- 8 GMM Comparative Case Study Balonia and BanchuriaDocument16 pages8 GMM Comparative Case Study Balonia and BanchuriaTina WuPas encore d'évaluation

- Tire City IncDocument3 pagesTire City IncAlberto RcPas encore d'évaluation

- Questions For Cases Winter 2011Document2 pagesQuestions For Cases Winter 2011AhmedMalikPas encore d'évaluation

- Jun18l1-Ep04 QDocument18 pagesJun18l1-Ep04 QjuanPas encore d'évaluation

- Quiz 1 The Body Shop International PLCDocument13 pagesQuiz 1 The Body Shop International PLCNaman Nepal100% (1)

- Syndicate 1 Nike Cost of Capital FinalDocument2 pagesSyndicate 1 Nike Cost of Capital FinalirfanmuafiPas encore d'évaluation

- Oasis Hong Kong Case FinalDocument58 pagesOasis Hong Kong Case FinalAtika Siti AminahPas encore d'évaluation

- Boeing 7E7 Case Questions PDFDocument1 pageBoeing 7E7 Case Questions PDFErick ClarkPas encore d'évaluation

- 02 Eaton Questions PDFDocument1 page02 Eaton Questions PDFSulaiman AminPas encore d'évaluation

- Fonderia Case Assignment - Syndicate 6 - FIXEDDocument5 pagesFonderia Case Assignment - Syndicate 6 - FIXEDAyustina GiustiPas encore d'évaluation

- Marriott CaseDocument1 pageMarriott CasejenniferPas encore d'évaluation

- AOL.com (Review and Analysis of Swisher's Book)D'EverandAOL.com (Review and Analysis of Swisher's Book)Pas encore d'évaluation

- TN38 Primus Automation Division 2002Document11 pagesTN38 Primus Automation Division 2002mylittle_pg100% (1)

- Primus Automotion Devision Case 2002Document9 pagesPrimus Automotion Devision Case 2002Devin Fortranansi FirdausPas encore d'évaluation

- This Spreadsheet Supports The Analysis of The Case "Flinder Valves and Controls Inc." (Case 43)Document19 pagesThis Spreadsheet Supports The Analysis of The Case "Flinder Valves and Controls Inc." (Case 43)ntl2180% (1)

- Case 9Document15 pagesCase 9didiPas encore d'évaluation

- KCHRDocument3 pagesKCHRAftab AhmeedPas encore d'évaluation

- Aurora PaperDocument6 pagesAurora PaperZhijian Huang100% (1)

- CM FinanceforUndergradsDocument5 pagesCM FinanceforUndergradsChaucer19Pas encore d'évaluation

- Samsung CaseDocument16 pagesSamsung Caseamunhu145Pas encore d'évaluation

- Nike Equity ManagementDocument11 pagesNike Equity ManagementVikrant KumarPas encore d'évaluation

- Deluxe Corporation Case StudyDocument3 pagesDeluxe Corporation Case StudyHEM BANSALPas encore d'évaluation

- Case 32 - Analysis GuidanceDocument1 pageCase 32 - Analysis GuidanceVoramon PolkertPas encore d'évaluation

- Integrative Case 10 1 Projected Financial Statements For StarbucDocument2 pagesIntegrative Case 10 1 Projected Financial Statements For StarbucAmit PandeyPas encore d'évaluation

- The WM Wringley JR CompanyDocument3 pagesThe WM Wringley JR Companyavnish kumarPas encore d'évaluation

- Bond Problem - Fixed Income ValuationDocument1 pageBond Problem - Fixed Income ValuationAbhishek Garg0% (2)

- Northern Forest ProductsDocument15 pagesNorthern Forest ProductsHương Lan TrịnhPas encore d'évaluation

- Team Members: S No Parameter Zencap Blackgem PreferredDocument2 pagesTeam Members: S No Parameter Zencap Blackgem PreferredKshitishPas encore d'évaluation

- Solusi Flinder 3Document4 pagesSolusi Flinder 3Lalang PalambangPas encore d'évaluation

- Mid Term Exam MCQs For 5530Document6 pagesMid Term Exam MCQs For 5530Amy WangPas encore d'évaluation

- Gainesboro Machine ToolsDocument2 pagesGainesboro Machine ToolsedselPas encore d'évaluation

- Timken Case Study: The Merits of An Acquisition of Rulmenti Grei and The Risks For TimkenDocument7 pagesTimken Case Study: The Merits of An Acquisition of Rulmenti Grei and The Risks For TimkenHa DoanPas encore d'évaluation

- Case 42 West Coast DirectedDocument6 pagesCase 42 West Coast DirectedHaidar IsmailPas encore d'évaluation

- BMA 12e PPT Ch13 16 PDFDocument68 pagesBMA 12e PPT Ch13 16 PDFLuu ParrondoPas encore d'évaluation

- FY07FY Financial Management and PoliciesDocument5 pagesFY07FY Financial Management and Policiesjablay29030% (1)

- SS KuniangDocument8 pagesSS KuniangvaiidyaPas encore d'évaluation

- Accounting Analysis HyfluxDocument2 pagesAccounting Analysis HyfluxNicholas LumPas encore d'évaluation

- Chapter 18Document17 pagesChapter 18queen hassaneenPas encore d'évaluation

- M&A and Corporate Restructuring) - Prof. Ercos Valdivieso: Jung Keun Kim, Yoon Ho Hur, Soo Hyun Ahn, Jee Hyun KoDocument2 pagesM&A and Corporate Restructuring) - Prof. Ercos Valdivieso: Jung Keun Kim, Yoon Ho Hur, Soo Hyun Ahn, Jee Hyun Ko고지현100% (1)

- Motorola RAZR - Case PDFDocument8 pagesMotorola RAZR - Case PDFSergio AlejandroPas encore d'évaluation

- Airbus A3XX Case QuestionsDocument1 pageAirbus A3XX Case QuestionsPradnya SalvePas encore d'évaluation

- Financial DetectiveDocument16 pagesFinancial DetectiveNadya AzzuraPas encore d'évaluation

- Capital Structure of ENCANADocument6 pagesCapital Structure of ENCANAsujata shahPas encore d'évaluation

- Example of Investment Analysis Paper PDFDocument24 pagesExample of Investment Analysis Paper PDFYoga Nurrahman AchfahaniPas encore d'évaluation

- Dollarization in Vietnam (Complete)Document15 pagesDollarization in Vietnam (Complete)Thuy Duong DuongPas encore d'évaluation

- Case 43Document3 pagesCase 43Stella TralalatrililiPas encore d'évaluation

- Appendix TN1 TN43 Flinder Valves and Controls IncDocument1 pageAppendix TN1 TN43 Flinder Valves and Controls IncStephanie WidjayaPas encore d'évaluation

- Turnaround StrategyDocument2 pagesTurnaround Strategyamittripathy084783Pas encore d'évaluation

- Case 13Document12 pagesCase 13Superb AdnanPas encore d'évaluation

- This Spreadsheet Supports Analysis of The Case, "American Greetings" (Case 43)Document52 pagesThis Spreadsheet Supports Analysis of The Case, "American Greetings" (Case 43)mehar noorPas encore d'évaluation

- Gamification in Consumer Research A Clear and Concise ReferenceD'EverandGamification in Consumer Research A Clear and Concise ReferencePas encore d'évaluation

- ASEAN Corporate Governance Scorecard Country Reports and Assessments 2019D'EverandASEAN Corporate Governance Scorecard Country Reports and Assessments 2019Pas encore d'évaluation

- Industrial Analysis-Financial Services: Presented To - Prof. Tarun Agarwal SirDocument19 pagesIndustrial Analysis-Financial Services: Presented To - Prof. Tarun Agarwal SirGEETESH KUMAR JAINPas encore d'évaluation

- Arvog Finance Corporate Presentation 2022Document9 pagesArvog Finance Corporate Presentation 2022Dinesh KandpalPas encore d'évaluation

- Ias 36 ImpairementDocument24 pagesIas 36 Impairementesulawyer2001Pas encore d'évaluation

- Directional Options TradingDocument24 pagesDirectional Options Tradingmaoychris0% (1)

- AD312 Sample Final Exam 2020 (With Answers)Document2 pagesAD312 Sample Final Exam 2020 (With Answers)Ekin MadenPas encore d'évaluation

- Management AccountingDocument155 pagesManagement AccountingBbaggi Bk100% (2)

- Islamic Banking Situational Mcqs PDFDocument24 pagesIslamic Banking Situational Mcqs PDFNajeeb Magsi100% (1)

- Chapter 02Document11 pagesChapter 02Saad mubeenPas encore d'évaluation

- 21127, Ahmad, Assignment 5, IFDocument5 pages21127, Ahmad, Assignment 5, IFmuhammad ahmadPas encore d'évaluation

- Underwriting: Types of Underwriting (1) FirmunderwritingDocument8 pagesUnderwriting: Types of Underwriting (1) FirmunderwritingThakker NimeshPas encore d'évaluation

- 805, Rohan D Bharambe, A Comparative Analysis On E-Banking Between ICICI and HDFC BankDocument79 pages805, Rohan D Bharambe, A Comparative Analysis On E-Banking Between ICICI and HDFC BankPranav PastePas encore d'évaluation

- Untitled SpreadsheetDocument12 pagesUntitled SpreadsheetNoble JonesPas encore d'évaluation

- Marketing - Ansoff MatrixDocument8 pagesMarketing - Ansoff Matrixmatthew mafaraPas encore d'évaluation

- Chapter 1 Research IVYDocument22 pagesChapter 1 Research IVYPrincess IvyPas encore d'évaluation

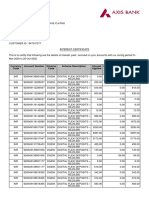

- Interest CertificateDocument2 pagesInterest CertificatesumitPas encore d'évaluation

- DD MFR FinalDocument105 pagesDD MFR Finalbig johnPas encore d'évaluation

- Zabala Auto SupplyDocument7 pagesZabala Auto SupplyLeighsen VillacortaPas encore d'évaluation

- Jurnal 2 - Alaeto Henry Emeka (2020) - Determinants - of - Dividend - Polic - NigeriaDocument31 pagesJurnal 2 - Alaeto Henry Emeka (2020) - Determinants - of - Dividend - Polic - NigeriaGilang KotawaPas encore d'évaluation

- SM1001904 Chapter-5 Caselets PDFDocument4 pagesSM1001904 Chapter-5 Caselets PDFsai bhargavPas encore d'évaluation

- Mod 4.2Document27 pagesMod 4.2NitishPas encore d'évaluation

- Ma 6Document32 pagesMa 6Tausif Narmawala0% (1)

- Laabh BookletDocument33 pagesLaabh BookletSri RamPas encore d'évaluation

- Sunson Textile Manufacturer TBK.: Company Report: January 2019 As of 31 January 2019Document3 pagesSunson Textile Manufacturer TBK.: Company Report: January 2019 As of 31 January 2019Anisah AmeliaPas encore d'évaluation

- Banker Customer Relationship - Exam2 PDFDocument3 pagesBanker Customer Relationship - Exam2 PDFrahulpatel1202Pas encore d'évaluation

- Notes On MicrofinanceDocument8 pagesNotes On MicrofinanceMapuia Lal Pachuau100% (2)

- Cash Receipts Record (Crrec) : InstructionsDocument1 pageCash Receipts Record (Crrec) : InstructionsdinvPas encore d'évaluation

- 4.3.2.5 Elaborate - Determining AdjustmentsDocument4 pages4.3.2.5 Elaborate - Determining AdjustmentsMa Fe Tabasa0% (1)

- My Cash: Balance TotalDocument9 pagesMy Cash: Balance TotalDahlan MuksinPas encore d'évaluation

- Technical Indicators: - Stochastic Oscillator - Relative Strength Index - Moving Average Convergence-DivergenceDocument32 pagesTechnical Indicators: - Stochastic Oscillator - Relative Strength Index - Moving Average Convergence-DivergenceChartSniperPas encore d'évaluation

- Fabm2 - Statement of Comprehensive Income (Practice Problems) - Answer KeyDocument3 pagesFabm2 - Statement of Comprehensive Income (Practice Problems) - Answer KeyMounicha Ambayec100% (4)