Vous aimerez peut-être aussi

- Identifying Critical Points and Improvement Strategies in Supply Chain, Using Scor Model, Theory of Constraint, and Six SigmaDocument16 pagesIdentifying Critical Points and Improvement Strategies in Supply Chain, Using Scor Model, Theory of Constraint, and Six SigmaHossein ParsianPas encore d'évaluation

- Budgetary Participation and Managerial Performance: The Impact of Information and Environmental VolatilityDocument12 pagesBudgetary Participation and Managerial Performance: The Impact of Information and Environmental VolatilityHossein ParsianPas encore d'évaluation

- Effects of Stress On Auditors' Organizational Commitment, Job Satisfaction, and Job PerformanceDocument12 pagesEffects of Stress On Auditors' Organizational Commitment, Job Satisfaction, and Job PerformanceHossein ParsianPas encore d'évaluation

- The Impact of Future Market On Money Demand in IranDocument7 pagesThe Impact of Future Market On Money Demand in IranHossein ParsianPas encore d'évaluation

- The Effect of Nominal and Real Reporting Difference in Predicting Cash Flows of Companies in Tehran Stock ExchangeDocument6 pagesThe Effect of Nominal and Real Reporting Difference in Predicting Cash Flows of Companies in Tehran Stock ExchangeHossein ParsianPas encore d'évaluation

- The Effects of Targeted Subsidies Public Firms On Their Performance in Tehran Stock ExchangeDocument7 pagesThe Effects of Targeted Subsidies Public Firms On Their Performance in Tehran Stock ExchangeHossein ParsianPas encore d'évaluation

- A Study On Relationship Between Earnings Before Tax, Interest and Operational Cash Flows With Stockholders' EquityDocument8 pagesA Study On Relationship Between Earnings Before Tax, Interest and Operational Cash Flows With Stockholders' EquityHossein ParsianPas encore d'évaluation

- The Effect of Oil Price Volatilities On Macroeconomic Variables in Iran (Structural Vector Auto Regression Approach)Document11 pagesThe Effect of Oil Price Volatilities On Macroeconomic Variables in Iran (Structural Vector Auto Regression Approach)Hossein ParsianPas encore d'évaluation

- The Relationship between Earnings before Interest and Tax and Operating Cash Flow and Stock Return in Information Asymmetry Conditions at Pharmaceutical Companies of Abidi and DarouPakhsh Applying Markov-switching ApproachDocument13 pagesThe Relationship between Earnings before Interest and Tax and Operating Cash Flow and Stock Return in Information Asymmetry Conditions at Pharmaceutical Companies of Abidi and DarouPakhsh Applying Markov-switching ApproachHossein ParsianPas encore d'évaluation

- The Effect of Free Cash Flow On Dividend Policy With Considering Life Cycle of CorporationsDocument23 pagesThe Effect of Free Cash Flow On Dividend Policy With Considering Life Cycle of CorporationsHossein ParsianPas encore d'évaluation

- The Relationship Between Dividend Payouts Ratio and Future Earnings Growth, A Case of Listed Company in IRAN MarketDocument7 pagesThe Relationship Between Dividend Payouts Ratio and Future Earnings Growth, A Case of Listed Company in IRAN MarketHossein ParsianPas encore d'évaluation

- The Role of Economic Factors in Profitability of Accepted Companies in Stock Exchange of TehranDocument9 pagesThe Role of Economic Factors in Profitability of Accepted Companies in Stock Exchange of TehranHossein ParsianPas encore d'évaluation

- Integrating Neural Network and Colonial Competitive Algorithm: A New Approach For Predicting Bankruptcy in Tehran Security ExchangeDocument11 pagesIntegrating Neural Network and Colonial Competitive Algorithm: A New Approach For Predicting Bankruptcy in Tehran Security ExchangeHossein ParsianPas encore d'évaluation

- A Study On The Effect of Free Cash Flow and Profitability Current Ratio On Dividend Payout Ratio: Evidence From Tehran Stock ExchangeDocument8 pagesA Study On The Effect of Free Cash Flow and Profitability Current Ratio On Dividend Payout Ratio: Evidence From Tehran Stock ExchangeHossein ParsianPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- FINAL PROSPECTUS - ATRAM Equity Opportunity Fund May 2018 PDFDocument54 pagesFINAL PROSPECTUS - ATRAM Equity Opportunity Fund May 2018 PDFriro zelrickPas encore d'évaluation

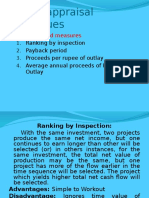

- Project appraisal techniques analysisDocument44 pagesProject appraisal techniques analysisRaghupathi Venkata SujathaPas encore d'évaluation

- Securitisation: Sabyasachi MukherjeeDocument40 pagesSecuritisation: Sabyasachi MukherjeeguptevaibhavPas encore d'évaluation

- Full Download Test Bank For Organic Chemistry 6th Edition Janice Smith PDF Full ChapterDocument36 pagesFull Download Test Bank For Organic Chemistry 6th Edition Janice Smith PDF Full Chapterprivitywoolhall.8hvcd100% (18)

- LANDBANK CASH CARD APPLICATIONDocument2 pagesLANDBANK CASH CARD APPLICATIONFernando Viscara Jr.Pas encore d'évaluation

- Global Economic Meltdown and Its Impact On India-FinalDocument19 pagesGlobal Economic Meltdown and Its Impact On India-FinalSuraj ShettyPas encore d'évaluation

- Online FinTech Fundamentals CourseDocument4 pagesOnline FinTech Fundamentals CourseDharini Raje SisodiaPas encore d'évaluation

- IBBL's General Banking, Investment & FX OperationsDocument81 pagesIBBL's General Banking, Investment & FX Operationsjony811467% (3)

- Assessing A New Venture's Financial Strength and Viability: ©2010 Pearson EducationDocument24 pagesAssessing A New Venture's Financial Strength and Viability: ©2010 Pearson EducationAyesha LatifPas encore d'évaluation

- (ACYFAR2) Toribio Critique Paper K36.editedDocument12 pages(ACYFAR2) Toribio Critique Paper K36.editedHannah Jane ToribioPas encore d'évaluation

- Berkshire Hathaway Balance Sheet Analysis (EXCELLENT)Document38 pagesBerkshire Hathaway Balance Sheet Analysis (EXCELLENT)Michael Cano LombardoPas encore d'évaluation

- Receipt For Your PaymentDocument2 pagesReceipt For Your PaymentMime MendozaPas encore d'évaluation

- Cfas ReviewerDocument10 pagesCfas ReviewerMarian grace DivinoPas encore d'évaluation

- PreviewDocument5 pagesPreviewFaz AliPas encore d'évaluation

- RAM A Study On Equity Research Analysis at India Bulls LimitedDocument44 pagesRAM A Study On Equity Research Analysis at India Bulls Limitedalapati173768Pas encore d'évaluation

- The Premier BankDocument1 pageThe Premier BankfgfdghfPas encore d'évaluation

- C S4FTR 2020 1669389459Document63 pagesC S4FTR 2020 1669389459Thirumalai ShanmugamPas encore d'évaluation

- Course Module - Chapter 9 - Interest in Joint VenturesDocument9 pagesCourse Module - Chapter 9 - Interest in Joint VenturesMarianne DadullaPas encore d'évaluation

- FM303 Tutorial Question Week 5Document3 pagesFM303 Tutorial Question Week 5Smriti LalPas encore d'évaluation

- Dac 212:principles of Taxation Revision Questions Topics 1-4Document6 pagesDac 212:principles of Taxation Revision Questions Topics 1-4Nickson AkolaPas encore d'évaluation

- Additional Note Cash BudgetDocument6 pagesAdditional Note Cash BudgetRaudhatun Nisa'Pas encore d'évaluation

- Project On Working Capital Management On Cement IndustriesDocument74 pagesProject On Working Capital Management On Cement IndustriesJofin JosePas encore d'évaluation

- 1 - Investment Techniques - An IntroductionDocument33 pages1 - Investment Techniques - An Introductionachu powellPas encore d'évaluation

- EY Young Tax Professional Wins AwardDocument5 pagesEY Young Tax Professional Wins AwardXiaxun OngPas encore d'évaluation

- Chapter 18 - Equity Valuation ModelsDocument44 pagesChapter 18 - Equity Valuation ModelsQingXu1986Pas encore d'évaluation

- 9781617975202Document221 pages9781617975202Mohamed Abd ElrahmanPas encore d'évaluation

- Hoba-Assignment 1-SolutionDocument8 pagesHoba-Assignment 1-SolutionVenis TuralloPas encore d'évaluation

- BUSANA1 Chapter1 - Simple Interest and DiscountDocument82 pagesBUSANA1 Chapter1 - Simple Interest and DiscountIzzeah RamosPas encore d'évaluation

- Joe's camera shop accounting questionsDocument2 pagesJoe's camera shop accounting questionsOkasha AliPas encore d'évaluation

- Ysch Oolg Ist.c Om: Principles of Accounts General ObjectivesDocument6 pagesYsch Oolg Ist.c Om: Principles of Accounts General ObjectivesGabriel UdokangPas encore d'évaluation