Vous aimerez peut-être aussi

- Key Ratios For Analyzing Oil and Gas Stocks: Measuring Performance - InvestopediaDocument3 pagesKey Ratios For Analyzing Oil and Gas Stocks: Measuring Performance - Investopediapolobook3782Pas encore d'évaluation

- RBC Equity Research Imperial PDFDocument11 pagesRBC Equity Research Imperial PDFHong Ee GohPas encore d'évaluation

- BP Strategic and Financial AnalysisDocument25 pagesBP Strategic and Financial AnalysisBatu Cem EkizPas encore d'évaluation

- Fuel Pumps & Fuel Tanks (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryD'EverandFuel Pumps & Fuel Tanks (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryPas encore d'évaluation

- RE: Maintaining The Methodological Integrity of The Renewable Fuel Standard (RFS)Document4 pagesRE: Maintaining The Methodological Integrity of The Renewable Fuel Standard (RFS)CREWPas encore d'évaluation

- Key Ratios For Analyzing Oil and Gas Stocks - Measuring PerformanceDocument3 pagesKey Ratios For Analyzing Oil and Gas Stocks - Measuring Performancek7hussainPas encore d'évaluation

- Comparing pricing strategies of two gasoline stationsDocument2 pagesComparing pricing strategies of two gasoline stationsVanessa GabroninoPas encore d'évaluation

- TheoilsectorDocument24 pagesTheoilsectorjamilkhannPas encore d'évaluation

- OPEC supply cuts and oil price forecasts for 2009-2010Document1 pageOPEC supply cuts and oil price forecasts for 2009-2010mazenkhodr1983Pas encore d'évaluation

- 2015 Outlook On Oil and Gas:: My Take: by John EnglandDocument4 pages2015 Outlook On Oil and Gas:: My Take: by John EnglandsendarnabPas encore d'évaluation

- Effects of Decreasing in Oil Prices On Global and Saudia Arab EconomyDocument48 pagesEffects of Decreasing in Oil Prices On Global and Saudia Arab EconomyMomal TanveerPas encore d'évaluation

- Canadian Oil Out LookDocument10 pagesCanadian Oil Out LookbbliancePas encore d'évaluation

- SPE-191766-MS Assessment of Petroleum Sensitive Countries Economic Reforms in Reaction To Fluctuating Oil PricesDocument13 pagesSPE-191766-MS Assessment of Petroleum Sensitive Countries Economic Reforms in Reaction To Fluctuating Oil PricesGabriel SPas encore d'évaluation

- CRS Report For Congress: Oil Industry Profits: Analysis of Recent PerformanceDocument25 pagesCRS Report For Congress: Oil Industry Profits: Analysis of Recent PerformanceSubhas ChakrabartiPas encore d'évaluation

- Advantages and Economic Benefits of Crude Oil TransportationDocument12 pagesAdvantages and Economic Benefits of Crude Oil TransportationRüstəm Emrah QədirovPas encore d'évaluation

- Oil & Gas Valuation Case Study: Ultra Petroleum (UPL) and Its Acquisition of The Uinta Basin Acreage - SHORT Recommendation Notes and DisclaimersDocument21 pagesOil & Gas Valuation Case Study: Ultra Petroleum (UPL) and Its Acquisition of The Uinta Basin Acreage - SHORT Recommendation Notes and DisclaimersihopethisworksPas encore d'évaluation

- Report On M & A Enterprise Valuation FinalDocument14 pagesReport On M & A Enterprise Valuation FinalAnithaPas encore d'évaluation

- TL Potential Winners of Low Oil Part1Document11 pagesTL Potential Winners of Low Oil Part1dpbasicPas encore d'évaluation

- Energy Sector Outlook: What We Are Watching: MarketDocument5 pagesEnergy Sector Outlook: What We Are Watching: MarketdpbasicPas encore d'évaluation

- Ratio AnalysisDocument27 pagesRatio AnalysisChinaBandaru100% (1)

- Alberta Royalty Rates ExplainedDocument2 pagesAlberta Royalty Rates ExplainedWilson Pepe GonzalezPas encore d'évaluation

- 02-04-2010 1Q Earnings Release FINALDocument22 pages02-04-2010 1Q Earnings Release FINALSueFloydPas encore d'évaluation

- Oil and Natural Gas SectorDocument16 pagesOil and Natural Gas Sectorsmritim_3Pas encore d'évaluation

- BP Stock ReportDocument2 pagesBP Stock Reportapi-269271900Pas encore d'évaluation

- New Bunker Adjustment Factor (BAF) : Customer AdvisoryDocument4 pagesNew Bunker Adjustment Factor (BAF) : Customer AdvisoryJulius Eric PajarilloPas encore d'évaluation

- UOP-Maximizing-Diesel-in-Existing-Assets-Tech-Paper3 - NPRA 2009 Dieselization Paper FinalDocument24 pagesUOP-Maximizing-Diesel-in-Existing-Assets-Tech-Paper3 - NPRA 2009 Dieselization Paper FinalsantiagoPas encore d'évaluation

- Group Project - Sensitivity AnalysisDocument8 pagesGroup Project - Sensitivity AnalysisSalomon Cure CorreaPas encore d'évaluation

- The U.S. Shale Oil Boom, The Oil Export Ban, and The Economy: A General Equilibrium AnalysisDocument61 pagesThe U.S. Shale Oil Boom, The Oil Export Ban, and The Economy: A General Equilibrium Analysisag rPas encore d'évaluation

- An Effort To Devise A Strategy For Pricing of Petroleum ProductsDocument12 pagesAn Effort To Devise A Strategy For Pricing of Petroleum ProductsHimanshu SharmaPas encore d'évaluation

- OPEC+ Production Cut Impact on Oil Prices & MarketDocument6 pagesOPEC+ Production Cut Impact on Oil Prices & MarketRG MoPNGPas encore d'évaluation

- Dissertation Oil PricesDocument4 pagesDissertation Oil PricesDoMyCollegePaperForMeColumbia100% (1)

- JP Morgan Oil Gas BasicsDocument69 pagesJP Morgan Oil Gas BasicsSwapnil Wankhede100% (1)

- Nigeria's Government Considers Petroleum Industry Bill 2020, A New Framework For The Oil and Gas SectorDocument6 pagesNigeria's Government Considers Petroleum Industry Bill 2020, A New Framework For The Oil and Gas Sectorpradeep s gillPas encore d'évaluation

- Petroleum Subsidies: A Case Against SubsidiesDocument25 pagesPetroleum Subsidies: A Case Against Subsidiesanmol_bajajPas encore d'évaluation

- KiritParekhCommitteeReport AngelDocument5 pagesKiritParekhCommitteeReport AngelshshashankPas encore d'évaluation

- OPEC Oil Outlook 2030Document22 pagesOPEC Oil Outlook 2030Bruno Dias da CostaPas encore d'évaluation

- Oil & Gas Valuation Case Study: Ultra Petroleum (UPL) and Its Acquisition of The Uinta Basin Acreage - SHORT Recommendation Notes and DisclaimersDocument21 pagesOil & Gas Valuation Case Study: Ultra Petroleum (UPL) and Its Acquisition of The Uinta Basin Acreage - SHORT Recommendation Notes and DisclaimersDiego VegaPas encore d'évaluation

- SPE-193470-MS Analysis of Government and Contractor Take Statistics in The Proposed Petroleum Industry Fiscal BillDocument14 pagesSPE-193470-MS Analysis of Government and Contractor Take Statistics in The Proposed Petroleum Industry Fiscal Billipali4christ_5308248Pas encore d'évaluation

- Shale Oil and EffectsDocument20 pagesShale Oil and EffectsDag AlpPas encore d'évaluation

- Yeni Microsoft Office Word DocumentDocument2 pagesYeni Microsoft Office Word DocumentzulkadirPas encore d'évaluation

- Gasoline and Diesel Price ForecastDocument5 pagesGasoline and Diesel Price ForecastabdulazizPas encore d'évaluation

- Annual ReportDocument192 pagesAnnual ReporttsanshinePas encore d'évaluation

- IndiaDocument11 pagesIndiaMd Riz ZamaPas encore d'évaluation

- Peabody Energy - Bmo Presentation SubmittedDocument24 pagesPeabody Energy - Bmo Presentation SubmittedsinnlosPas encore d'évaluation

- Index File FYI: Download The Original AttachmentDocument57 pagesIndex File FYI: Download The Original AttachmentAffNeg.Com100% (1)

- Lags, Costs, and Shocks Model Volatility Oil IndustryDocument52 pagesLags, Costs, and Shocks Model Volatility Oil Industryfatalbert555Pas encore d'évaluation

- RWF 5Document2 pagesRWF 5Petr KozinetsPas encore d'évaluation

- WGWNovember 2011Document8 pagesWGWNovember 2011Fais RockPas encore d'évaluation

- Conocophillips (Cop) - 2007 Integrated Oil & Gas OutlookDocument4 pagesConocophillips (Cop) - 2007 Integrated Oil & Gas OutlookSaul StermanPas encore d'évaluation

- Refining GRMDocument12 pagesRefining GRMVivek GoyalPas encore d'évaluation

- Letter To President ObamaDocument4 pagesLetter To President ObamaFuelsAmericaPas encore d'évaluation

- Research of The WeekDocument14 pagesResearch of The WeekValeed ChPas encore d'évaluation

- India - Oil & Gas: Major Reforms Push, Oil Psus Key BeneficiariesDocument9 pagesIndia - Oil & Gas: Major Reforms Push, Oil Psus Key BeneficiariesgirishrajsPas encore d'évaluation

- Hooked On Hydrocarbons: How Susceptible Are Gulf Sovereigns To Concentration Risk?Document9 pagesHooked On Hydrocarbons: How Susceptible Are Gulf Sovereigns To Concentration Risk?api-227433089Pas encore d'évaluation

- Us Tax Credits and Incentives For Oil and Gas ProducersDocument13 pagesUs Tax Credits and Incentives For Oil and Gas ProducersRaycharlesPas encore d'évaluation

- Solar Powered Agro Industrial Project of Cassava Based Bioethanol Processing UnitD'EverandSolar Powered Agro Industrial Project of Cassava Based Bioethanol Processing UnitPas encore d'évaluation

- Carburettors, Fuel Injection & Parts (Car OE & Aftermarket) World Summary: Market Values & Financials by CountryD'EverandCarburettors, Fuel Injection & Parts (Car OE & Aftermarket) World Summary: Market Values & Financials by CountryPas encore d'évaluation

- Fuel & Feedstock Gases World Summary: Market Values & Financials by CountryD'EverandFuel & Feedstock Gases World Summary: Market Values & Financials by CountryPas encore d'évaluation

- FOCUS REPORT: U.S. Shale Gale under Threat from Oil Price PlungeD'EverandFOCUS REPORT: U.S. Shale Gale under Threat from Oil Price PlungeÉvaluation : 2 sur 5 étoiles2/5 (1)

- AGletter BPDocument3 pagesAGletter BPTeamWildrosePas encore d'évaluation

- Balancing Pool FOIPS - HighlightsDocument60 pagesBalancing Pool FOIPS - HighlightsTeamWildrosePas encore d'évaluation

- Political Staff DirectoryDocument23 pagesPolitical Staff DirectoryTeamWildrosePas encore d'évaluation

- Power Purchase Agreement ClauseDocument1 pagePower Purchase Agreement ClauseTeamWildrosePas encore d'évaluation

- Revised Terms of Reference LetterDocument3 pagesRevised Terms of Reference LetterTeamWildrosePas encore d'évaluation

- 2015 Code Red DataDocument19 pages2015 Code Red DataTeamWildrosePas encore d'évaluation

- MacIntyre Letter To Jill ClaytonDocument2 pagesMacIntyre Letter To Jill ClaytonTeamWildrosePas encore d'évaluation

- Balancing Pool FOIPSDocument330 pagesBalancing Pool FOIPSTeamWildrosePas encore d'évaluation

- Revised Terms of ReferenceDocument2 pagesRevised Terms of ReferenceTeamWildrosePas encore d'évaluation

- Fentanyl Letter To PM TrudeauDocument3 pagesFentanyl Letter To PM TrudeauTeamWildrosePas encore d'évaluation

- Sundre Hospital LetterDocument2 pagesSundre Hospital LetterTeamWildrosePas encore d'évaluation

- Kaminski Resignation Letter (Redacted Version)Document3 pagesKaminski Resignation Letter (Redacted Version)TeamWildrosePas encore d'évaluation

- Ethics Commissioner Letter From NixonDocument4 pagesEthics Commissioner Letter From NixonTeamWildrosePas encore d'évaluation

- Brian Jean Letter To Prime Minister Re: Moratorium On Tanker TrafficDocument2 pagesBrian Jean Letter To Prime Minister Re: Moratorium On Tanker TrafficTeamWildrosePas encore d'évaluation

- Speech To CD Howe InstituteDocument6 pagesSpeech To CD Howe InstituteTeamWildrosePas encore d'évaluation

- Speech To The Albany ClubDocument6 pagesSpeech To The Albany ClubTeamWildrosePas encore d'évaluation

- Hoffman Dental Fee Reform, February 19, 2016Document3 pagesHoffman Dental Fee Reform, February 19, 2016TeamWildrosePas encore d'évaluation

- NDP February 19 Fundraiser FormDocument1 pageNDP February 19 Fundraiser FormTeamWildrosePas encore d'évaluation

- Equalization Mandate LetterDocument2 pagesEqualization Mandate LetterTeamWildrosePas encore d'évaluation

- MSC Family Friendly RecommendationsDocument2 pagesMSC Family Friendly RecommendationsTeamWildrosePas encore d'évaluation

- Healthier Albertans, Healthier CommunitiesDocument9 pagesHealthier Albertans, Healthier CommunitiesTeamWildrosePas encore d'évaluation

- Comparison of PrinciplesDocument3 pagesComparison of PrinciplesTeamWildrosePas encore d'évaluation

- Taxpayer Paid FundraiserDocument5 pagesTaxpayer Paid FundraiserTeamWildrosePas encore d'évaluation

- Jean Letter Prime Minister TrudeauDocument2 pagesJean Letter Prime Minister TrudeauTeamWildrosePas encore d'évaluation

- Hospital Response From Minister of HealthDocument1 pageHospital Response From Minister of HealthTeamWildrosePas encore d'évaluation

- Bill 6 (What Is Law and What Is Regulation)Document5 pagesBill 6 (What Is Law and What Is Regulation)TeamWildrosePas encore d'évaluation

- Letter Mason CapitalCall2016 PDFDocument3 pagesLetter Mason CapitalCall2016 PDFTeamWildrosePas encore d'évaluation

- Pitt - LTR To Child and Youth Advocate 2015 12 21 (00000003)Document1 pagePitt - LTR To Child and Youth Advocate 2015 12 21 (00000003)TeamWildrosePas encore d'évaluation

- Internal Bill 6 DocumentDocument2 pagesInternal Bill 6 DocumentTeamWildrosePas encore d'évaluation

- Notice of Standing Order 30Document1 pageNotice of Standing Order 30TeamWildrosePas encore d'évaluation

- Mangliya Plant, Indore (M.P.) : BY: Gloria Dsouza Mba MDocument29 pagesMangliya Plant, Indore (M.P.) : BY: Gloria Dsouza Mba MGloria DsouzaPas encore d'évaluation

- Managerial Economics Term PaperDocument12 pagesManagerial Economics Term PaperJason BournePas encore d'évaluation

- Brief History About The Edible Oil IndustryDocument7 pagesBrief History About The Edible Oil IndustryPatrice ScottPas encore d'évaluation

- The North South DialogueDocument2 pagesThe North South DialogueVaibhav SharmaPas encore d'évaluation

- Ukraine Conflict Impact - Mar 1st 2022 - BNI - COEDocument26 pagesUkraine Conflict Impact - Mar 1st 2022 - BNI - COEMuhammad Nur Mulianto PutraPas encore d'évaluation

- Aerospace Defense Outlook Dawn of New DayDocument32 pagesAerospace Defense Outlook Dawn of New Dayvigneshkumar rajanPas encore d'évaluation

- The Economist (Intelligence Unit) - Energy Outlook 2023Document9 pagesThe Economist (Intelligence Unit) - Energy Outlook 2023Dainanta Yudhisthira RadiadaPas encore d'évaluation

- AN Analysis of Impact of Crude Oil Prices On Indian EconomyDocument28 pagesAN Analysis of Impact of Crude Oil Prices On Indian EconomySrijan SaxenaPas encore d'évaluation

- Not All Oil Price Shocks Are Alike - Disentangling Demand and Supply Shocks in The Crude Oil Market (Lutz Kilian)Document22 pagesNot All Oil Price Shocks Are Alike - Disentangling Demand and Supply Shocks in The Crude Oil Market (Lutz Kilian)Andrés JiménezPas encore d'évaluation

- Futures Trading in Crude OilDocument14 pagesFutures Trading in Crude OilBhuvanesh Bhawre100% (1)

- IMF Regional Economic Outlook Sub-Saharan Africa April 2016Document137 pagesIMF Regional Economic Outlook Sub-Saharan Africa April 2016The Independent MagazinePas encore d'évaluation

- "Who Cares Wins": One Year On (November 2005)Document27 pages"Who Cares Wins": One Year On (November 2005)IFC SustainabilityPas encore d'évaluation

- Exchange Rate Fluctuations, Oil Prices and Economic Performance - Empirical Evidence From Nigeria (#350905) - 361408Document5 pagesExchange Rate Fluctuations, Oil Prices and Economic Performance - Empirical Evidence From Nigeria (#350905) - 361408Hammed AremuPas encore d'évaluation

- India's Growing Edible Oil Imports and Business OpportunitiesDocument19 pagesIndia's Growing Edible Oil Imports and Business Opportunitiessreeramchellappa100% (1)

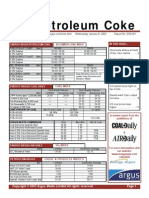

- Pet CokeDocument12 pagesPet Cokezementhead100% (1)

- KPMG Riesgos Financieros Revelaciones Cuantitativas EngDocument16 pagesKPMG Riesgos Financieros Revelaciones Cuantitativas EngPedroLayaPas encore d'évaluation

- Rupee Vs USD War: Prepared By: Courtney Tapiwa Mugodi Bba ViDocument9 pagesRupee Vs USD War: Prepared By: Courtney Tapiwa Mugodi Bba ViCourtney Tapiwa MugodiPas encore d'évaluation

- Impact of Russia Ukraine War On Daily Necessities of BangladeshDocument29 pagesImpact of Russia Ukraine War On Daily Necessities of BangladeshA R HRIDOY AKONPas encore d'évaluation

- ACI Airport Worldwide Traffic Report - Oct15Document33 pagesACI Airport Worldwide Traffic Report - Oct15freeflyairPas encore d'évaluation

- Market ScanDocument23 pagesMarket ScanGhasem2010Pas encore d'évaluation

- Performance Profiles of Major Energy Producers 020605Document110 pagesPerformance Profiles of Major Energy Producers 020605mmvvvPas encore d'évaluation

- Peabody Energy - Bmo Presentation SubmittedDocument24 pagesPeabody Energy - Bmo Presentation SubmittedsinnlosPas encore d'évaluation

- Covid19 AssignmentDocument5 pagesCovid19 AssignmentRish JayPas encore d'évaluation

- Understanding the Oil Industry Dynamics Using Porter's Five Forces FrameworkDocument11 pagesUnderstanding the Oil Industry Dynamics Using Porter's Five Forces FrameworkamareshgautamPas encore d'évaluation

- 03 Elasticity Tutorial - 2020 2Document10 pages03 Elasticity Tutorial - 2020 2Muhd UkasyahPas encore d'évaluation

- Annual Report 2015-42 E PDFDocument314 pagesAnnual Report 2015-42 E PDFSohini ChatterjeePas encore d'évaluation

- GSP 2204 (Nig Econ)Document19 pagesGSP 2204 (Nig Econ)olaoluwalawal19Pas encore d'évaluation

- 2019 Erp Pe P1Document104 pages2019 Erp Pe P1simi263Pas encore d'évaluation

- The Exxon-Mobil Merger: An Archetype: J. Fred WestonDocument20 pagesThe Exxon-Mobil Merger: An Archetype: J. Fred WestonTRANPas encore d'évaluation