Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- We Are All in This Together in The Global Currency ResetDocument10 pagesWe Are All in This Together in The Global Currency Resetkaren hudesPas encore d'évaluation

- Agreement of TakeoverDocument4 pagesAgreement of TakeoverMadhurima DuttaPas encore d'évaluation

- Customer Satisfaction towards RTGS & NEFTDocument70 pagesCustomer Satisfaction towards RTGS & NEFTRajibKumar100% (1)

- Insurance Law DigestDocument3 pagesInsurance Law DigestMorphuesPas encore d'évaluation

- Accounts Clerk Position JD Kpi KraDocument3 pagesAccounts Clerk Position JD Kpi KraCA AMIT JAINPas encore d'évaluation

- New Zealand Student Visa Application Form - InZ1012Document16 pagesNew Zealand Student Visa Application Form - InZ1012Paki12345100% (1)

- Cio FMCGDocument608 pagesCio FMCGshreya lakshminarayananPas encore d'évaluation

- Bses PDFDocument1 pageBses PDFShivam VishvakarmaPas encore d'évaluation

- Active Passive+sol 4Document121 pagesActive Passive+sol 4aayushcooolzPas encore d'évaluation

- Properties of TrianglesDocument8 pagesProperties of TrianglesaayushcooolzPas encore d'évaluation

- English Grammar (WWW - Qmaths.in)Document169 pagesEnglish Grammar (WWW - Qmaths.in)aayushcooolzPas encore d'évaluation

- Properties of TrianglesDocument8 pagesProperties of TrianglesaayushcooolzPas encore d'évaluation

- Sachin Tendulkar's CVDocument3 pagesSachin Tendulkar's CVhemant117100% (1)

- Empresas Que Cotizan en La BolsaDocument174 pagesEmpresas Que Cotizan en La Bolsasandra_maciasPas encore d'évaluation

- The Greatest Texas Bank Job: Felonious Balonias - ToxiczombiedevelopmentsDocument4 pagesThe Greatest Texas Bank Job: Felonious Balonias - ToxiczombiedevelopmentsBaqi-Khaliq BeyPas encore d'évaluation

- QUESTIONNAIRE SURVEY ON SBI BANK CUSTOMER SATISFACTIONDocument3 pagesQUESTIONNAIRE SURVEY ON SBI BANK CUSTOMER SATISFACTIONSelsiya AmulrajPas encore d'évaluation

- ALM Policy SummaryDocument9 pagesALM Policy Summarytreddy249Pas encore d'évaluation

- Role of Intermediaries in Insurance Sector-1Document32 pagesRole of Intermediaries in Insurance Sector-1Prakash Kumar100% (6)

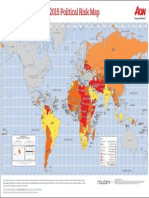

- Mapa Del Riesgo Político en 2015Document1 pageMapa Del Riesgo Político en 2015EpinternetPas encore d'évaluation

- Section I PDFDocument2 pagesSection I PDFAnonymous 7ZYHilD100% (1)

- Geragos & Geragos, APC v. The Travelers Indemnity Company of Connecticut Et Al (4!9!2020)Document7 pagesGeragos & Geragos, APC v. The Travelers Indemnity Company of Connecticut Et Al (4!9!2020)Law&Crime100% (1)

- SBI's Core Banking Systems and Networking TechnologiesDocument26 pagesSBI's Core Banking Systems and Networking TechnologiesUdit AnandPas encore d'évaluation

- Central Bank Regulation of Kenyan Commercial BanksDocument3 pagesCentral Bank Regulation of Kenyan Commercial BanksWesleyPas encore d'évaluation

- McMurdo-The Economics of Overthrow (CIA Library) PDFDocument12 pagesMcMurdo-The Economics of Overthrow (CIA Library) PDFmukhzinrashidPas encore d'évaluation

- ABM Annual Report 2014Document80 pagesABM Annual Report 2014Tan Gim GimPas encore d'évaluation

- Audit ReportDocument6 pagesAudit ReportRehan SaleemPas encore d'évaluation

- I AnnexureDocument4 pagesI AnnexureRiSHI KeSH GawaIPas encore d'évaluation

- Mba Shubhi Kapoor PDFDocument1 pageMba Shubhi Kapoor PDFVaibhav GuptaPas encore d'évaluation

- Name of Investors (Bidders) Interest Rate (%) Auction Volume (Billion Dong)Document2 pagesName of Investors (Bidders) Interest Rate (%) Auction Volume (Billion Dong)Trần Phương AnhPas encore d'évaluation

- 3310-Ch 4-End of Chapter Solutions-STDocument46 pages3310-Ch 4-End of Chapter Solutions-STArvind Mano100% (1)

- Bad News Letter ExamplesDocument11 pagesBad News Letter ExamplesBOsch VakilPas encore d'évaluation

- Explanation of deductions for certain payments under Section 37Document2 pagesExplanation of deductions for certain payments under Section 37NISHANTH JOSEPas encore d'évaluation

- Curriculum Vitae Summary for Atul KumarDocument3 pagesCurriculum Vitae Summary for Atul KumarRaushan RajPas encore d'évaluation

- Customer Perception About Product Services of Canara BankDocument62 pagesCustomer Perception About Product Services of Canara BankÂShu KaLràPas encore d'évaluation

- ch21 SolDocument21 pagesch21 SolJohn Nigz PayeePas encore d'évaluation