Vous aimerez peut-être aussi

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Week 5 - 8 Q4 New BaldozaDocument28 pagesWeek 5 - 8 Q4 New BaldozaChelsea Mae AlingPas encore d'évaluation

- Mini Proj RCT 222 PDFDocument34 pagesMini Proj RCT 222 PDF4073 kolakaluru mounishaPas encore d'évaluation

- Methodology of Model Creation: Mgr. Peter Kertys, VÚB A. SDocument11 pagesMethodology of Model Creation: Mgr. Peter Kertys, VÚB A. SJuan Diego Monasí CórdovaPas encore d'évaluation

- Cost Behavior and Forecasting: Seventh EditionDocument130 pagesCost Behavior and Forecasting: Seventh EditionKefas AnugrahPas encore d'évaluation

- Deep Learning Linear ModelsDocument49 pagesDeep Learning Linear Modelsthecoolguy96Pas encore d'évaluation

- Group4 - PBM - Sec CDocument13 pagesGroup4 - PBM - Sec Ckiran venugopalPas encore d'évaluation

- Calculator Techniques Part 1Document31 pagesCalculator Techniques Part 1Chris Angelo TorillosPas encore d'évaluation

- Chapter12 Regression PolynomialRegressionDocument12 pagesChapter12 Regression PolynomialRegressionSantosh Kumar GatadiPas encore d'évaluation

- The Relationship Between Motor Competence and Health-Related Fitness in Children and AdolescentsDocument11 pagesThe Relationship Between Motor Competence and Health-Related Fitness in Children and AdolescentsDwi AnggareksaPas encore d'évaluation

- Practical Research 2: QUARTER 2-MODULE 4: Understanding Data and Ways To Systematically Collect DataDocument27 pagesPractical Research 2: QUARTER 2-MODULE 4: Understanding Data and Ways To Systematically Collect DataKaye Antonette FloresPas encore d'évaluation

- Ekonometrika p9 PDFDocument4 pagesEkonometrika p9 PDFzalfa npbPas encore d'évaluation

- International Journal of Africa Nursing Sciences: Bayisa Bereka Negussie, Gebisa Bayisa OliksaDocument6 pagesInternational Journal of Africa Nursing Sciences: Bayisa Bereka Negussie, Gebisa Bayisa OliksaRaissa NoorPas encore d'évaluation

- Generating Routing-Driven Power Distribution NetworksDocument8 pagesGenerating Routing-Driven Power Distribution NetworksFudencio da SilvaPas encore d'évaluation

- Assumptions of Multiple Linear RegressionDocument18 pagesAssumptions of Multiple Linear RegressionDr. Krishan K. PandeyPas encore d'évaluation

- PHD Thesis (Imad Chbib)Document305 pagesPHD Thesis (Imad Chbib)Shruti DhanjalPas encore d'évaluation

- Econometrics NotesDocument2 pagesEconometrics NotesDaniel Bogiatzis GibbonsPas encore d'évaluation

- Foreign Language Attributions and Achievement in FDocument12 pagesForeign Language Attributions and Achievement in FLina MardiyanaPas encore d'évaluation

- An Empirical Study of Brand Switching For A Retail ServiceDocument30 pagesAn Empirical Study of Brand Switching For A Retail ServiceMohammad FouadPas encore d'évaluation

- Day31-Multiple Linear RegressionDocument4 pagesDay31-Multiple Linear RegressionForeverPas encore d'évaluation

- STATA Assignment 1 InstructionsDocument2 pagesSTATA Assignment 1 InstructionsRO BWNPas encore d'évaluation

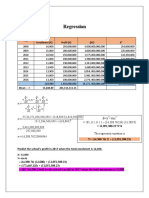

- Regression: 6. Year Total Enrollment (X) Profit (Y) (XY) XDocument2 pagesRegression: 6. Year Total Enrollment (X) Profit (Y) (XY) XShayne PagwaganPas encore d'évaluation

- 1 ORSolution Manual Ch01Document8 pages1 ORSolution Manual Ch01henryPas encore d'évaluation

- AI Complete Notes - Unit 1 To Unit 5Document62 pagesAI Complete Notes - Unit 1 To Unit 5Praveer Srivastava100% (2)

- Fraser Et Al (2015)Document5 pagesFraser Et Al (2015)Camila MujicaPas encore d'évaluation

- PDFDocument1 254 pagesPDFTrigun TejaPas encore d'évaluation

- Bus105 Pcoq 1Document15 pagesBus105 Pcoq 1Gish KK.GPas encore d'évaluation

- IQRM Book 2020 Jan 28 PDFDocument267 pagesIQRM Book 2020 Jan 28 PDFMELISSAPas encore d'évaluation

- Fmii 12115Document28 pagesFmii 12115NaimaPas encore d'évaluation

- Ordinary Least Square Technique: Advantage of The Principle of Least SquaresDocument9 pagesOrdinary Least Square Technique: Advantage of The Principle of Least SquaresGiri PrasadPas encore d'évaluation

- Da Unit-1Document23 pagesDa Unit-1Shruthi SayamPas encore d'évaluation