Vous aimerez peut-être aussi

- EMS CONTENT PresentationDocument3 pagesEMS CONTENT PresentationAthiwe NokwePas encore d'évaluation

- Factors of Production - The Economic Lowdown Podcast Series: TranscriptDocument2 pagesFactors of Production - The Economic Lowdown Podcast Series: TranscriptdsdsdPas encore d'évaluation

- Village Palampur Ix Notes - 2Document4 pagesVillage Palampur Ix Notes - 2Sanjay GenwaPas encore d'évaluation

- Tugas EconDocument4 pagesTugas EconninaPas encore d'évaluation

- TT EconomicDocument4 pagesTT EconomicTrần HeavenPas encore d'évaluation

- EcotaxaDocument8 pagesEcotaxaMark Leo Lamigo JacintoPas encore d'évaluation

- Tiếng Anh Quản TrịDocument8 pagesTiếng Anh Quản TrịHuynh LocPas encore d'évaluation

- Revisionbook For EcoDocument76 pagesRevisionbook For EcorohinPas encore d'évaluation

- Factors of ProductionDocument2 pagesFactors of ProductionSesinaPas encore d'évaluation

- Question:Factors of ProductionDocument2 pagesQuestion:Factors of ProductionMd. Tanvir HasanPas encore d'évaluation

- Factors of Production DefinitionDocument6 pagesFactors of Production DefinitionNumera SaleemPas encore d'évaluation

- Economics Principles 2007 Chpts 1-2 PDFDocument50 pagesEconomics Principles 2007 Chpts 1-2 PDFValeria0% (1)

- Factors of Production: Land, Labor, Capital and EntrepreneurshipDocument4 pagesFactors of Production: Land, Labor, Capital and EntrepreneurshipAman Deep SinghPas encore d'évaluation

- Intro to Economics: Scarce Resources & Economic DecisionsDocument37 pagesIntro to Economics: Scarce Resources & Economic Decisionsnunyu bidnesPas encore d'évaluation

- Eco-Notes-Chp 3.1Document36 pagesEco-Notes-Chp 3.1c9871515Pas encore d'évaluation

- Toppers Institute Kanpur Theory of Production and CostDocument42 pagesToppers Institute Kanpur Theory of Production and Costblack horsePas encore d'évaluation

- 3 B Revision NotesDocument169 pages3 B Revision NotesAurelia KimPas encore d'évaluation

- Production Factors and Types ExplainedDocument46 pagesProduction Factors and Types ExplainedNicolas RangelPas encore d'évaluation

- ProdMngt - 6 - Details of The ReportDocument45 pagesProdMngt - 6 - Details of The ReportNico PaoloPas encore d'évaluation

- ECO 001 Basic MicroeconomicsDocument16 pagesECO 001 Basic MicroeconomicsMickaela GulisPas encore d'évaluation

- Features of Economic AnalysisDocument48 pagesFeatures of Economic Analysisrjeffry03Pas encore d'évaluation

- The Economic ProblemDocument2 pagesThe Economic ProblemquratulainPas encore d'évaluation

- Chapter 6.Pptx NiosDocument20 pagesChapter 6.Pptx Niosamita venkateshPas encore d'évaluation

- Factors of Production: Land, Labour, Capital and EntrepreneurDocument2 pagesFactors of Production: Land, Labour, Capital and EntrepreneurAbrar RanaPas encore d'évaluation

- Project On Factors of ProductionDocument3 pagesProject On Factors of ProductionPriyanshiPas encore d'évaluation

- Business Concepts and DefinitionsDocument2 pagesBusiness Concepts and DefinitionsDevPas encore d'évaluation

- Economics - Assignment - Sangeeta DixitDocument11 pagesEconomics - Assignment - Sangeeta DixitVIKAS PAIDIPEDDIGARIPas encore d'évaluation

- IGCSE Economics Introduction and ScarcityDocument4 pagesIGCSE Economics Introduction and ScarcityJohnPas encore d'évaluation

- Assignment 1 (Microeconomics For Prova)Document7 pagesAssignment 1 (Microeconomics For Prova)Kamrul Hasan ShaonPas encore d'évaluation

- Study of The EconomyDocument5 pagesStudy of The EconomyMuhammad WasimPas encore d'évaluation

- How To ProduceDocument1 pageHow To ProduceXedric JuantaPas encore d'évaluation

- Economics O LevelDocument9 pagesEconomics O LevelClaudia GomesPas encore d'évaluation

- History AssignmentDocument4 pagesHistory Assignmentbekanmusic05Pas encore d'évaluation

- Unit 3 ProductionDocument32 pagesUnit 3 ProductionFitha FathimaPas encore d'évaluation

- Costing of Production SystemsDocument19 pagesCosting of Production SystemsAjala Oladimeji DurotoluwaPas encore d'évaluation

- Igcse Economics Gwatipedza - 240108 - 154623Document353 pagesIgcse Economics Gwatipedza - 240108 - 154623tauinafricaPas encore d'évaluation

- Write About Any of The Factors of Production in Detail ?: Land Labor Capital EntrepreneurshipDocument4 pagesWrite About Any of The Factors of Production in Detail ?: Land Labor Capital EntrepreneurshipEsha khanPas encore d'évaluation

- Theory of Production 1Document6 pagesTheory of Production 1Sky ceePas encore d'évaluation

- Allocation of ResourcesDocument14 pagesAllocation of ResourcesAzar Anjum RiazPas encore d'évaluation

- Macroeconomics: 1. MicroeconomicsDocument30 pagesMacroeconomics: 1. MicroeconomicsVictoria GalenkoPas encore d'évaluation

- Intro To Business - 20220817Document2 pagesIntro To Business - 20220817Joan DelatadoPas encore d'évaluation

- Basic Economic ConceptsDocument67 pagesBasic Economic ConceptsMuhammad TauseefPas encore d'évaluation

- Ss 1 Production EconomicsDocument23 pagesSs 1 Production Economicsgabrielfavour2010Pas encore d'évaluation

- Objectives of The SchemeDocument4 pagesObjectives of The Scheme1kashmirPas encore d'évaluation

- Unit 1 - Economic Activity: Text ADocument4 pagesUnit 1 - Economic Activity: Text AAyuniwulandariPas encore d'évaluation

- Section 1Document5 pagesSection 1samPas encore d'évaluation

- Emv 222 Lecture GuideDocument23 pagesEmv 222 Lecture Guidealica studioPas encore d'évaluation

- Understanding the Factors of ProductionDocument3 pagesUnderstanding the Factors of ProductionPsychoPak OfficialPas encore d'évaluation

- Individual Assignment (Is) - Khairul AmriDocument3 pagesIndividual Assignment (Is) - Khairul AmriKyrul AmryPas encore d'évaluation

- Module 3Document10 pagesModule 3trzie74Pas encore d'évaluation

- Today's Objectives: - Review Chapter One - QUIZ To Be Uploaded TomorrowDocument14 pagesToday's Objectives: - Review Chapter One - QUIZ To Be Uploaded Tomorrowwen jing yuPas encore d'évaluation

- Managerial Economics Module 1Document9 pagesManagerial Economics Module 1Caila Nicole ReyesPas encore d'évaluation

- FACTORSOFPRODUCTIONDocument1 pageFACTORSOFPRODUCTIONdimasPas encore d'évaluation

- Applied EconDocument49 pagesApplied EconJulie Ann SambranoPas encore d'évaluation

- 1 1 - 1 Basic Economic IdeasDocument4 pages1 1 - 1 Basic Economic IdeasTYDK MediaPas encore d'évaluation

- Understanding Economics Through Micro & Macro ConceptsDocument6 pagesUnderstanding Economics Through Micro & Macro ConceptsAngelica BerbalPas encore d'évaluation

- Tema 0Document6 pagesTema 0Ro ViEsPas encore d'évaluation

- Unit 2Document27 pagesUnit 2Cuti PandaPas encore d'évaluation

- Macroeconomics Analyzes The Decisions Made by Countries andDocument3 pagesMacroeconomics Analyzes The Decisions Made by Countries andKimberly BinoyaPas encore d'évaluation

- Alfalaval UVvsECDocument13 pagesAlfalaval UVvsECDeepak ShoriPas encore d'évaluation

- PDF 1Document45 pagesPDF 1Deepak ShoriPas encore d'évaluation

- SofDocument2 pagesSofDeepak ShoriPas encore d'évaluation

- ItfDocument3 pagesItfDeepak Shori100% (1)

- IMO News - Autumn Issue - 2017Document36 pagesIMO News - Autumn Issue - 2017Deepak ShoriPas encore d'évaluation

- Ethics in ShipbrokingDocument4 pagesEthics in ShipbrokingDeepak ShoriPas encore d'évaluation

- FocDocument7 pagesFocDeepak ShoriPas encore d'évaluation

- Safety Data Sheet: Product Name: MOBILGARD 540Document11 pagesSafety Data Sheet: Product Name: MOBILGARD 540Deepak ShoriPas encore d'évaluation

- Autocar Spare Parts Price SurveyDocument10 pagesAutocar Spare Parts Price SurveyDeepak ShoriPas encore d'évaluation

- ItfDocument3 pagesItfDeepak Shori100% (1)

- EthicsDocument8 pagesEthicsDeepak ShoriPas encore d'évaluation

- Variance AnalysisDocument1 pageVariance AnalysisDeepak ShoriPas encore d'évaluation

- Ship-owners' decisions to outsource vessel managementDocument24 pagesShip-owners' decisions to outsource vessel managementDeepak ShoriPas encore d'évaluation

- IccDocument3 pagesIccDeepak ShoriPas encore d'évaluation

- Law of TortsDocument41 pagesLaw of TortsDeepak ShoriPas encore d'évaluation

- Public and Private CompanyDocument22 pagesPublic and Private CompanyDeepak ShoriPas encore d'évaluation

- Special Circular: Revised Himalaya Clause For Bills of Lading and Other ContractsDocument3 pagesSpecial Circular: Revised Himalaya Clause For Bills of Lading and Other ContractsDeepak ShoriPas encore d'évaluation

- Riska of LOCDocument11 pagesRiska of LOCDeepak ShoriPas encore d'évaluation

- Public and Private CompanyDocument22 pagesPublic and Private CompanyDeepak ShoriPas encore d'évaluation

- Updated Glossary in Co TermsDocument13 pagesUpdated Glossary in Co TermsDeepak ShoriPas encore d'évaluation

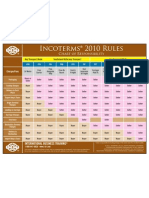

- Incoterms 2010 at A GlanceDocument1 pageIncoterms 2010 at A GlanceAftab UddinPas encore d'évaluation

- UC40+ User GuideDocument2 pagesUC40+ User GuideDeepak ShoriPas encore d'évaluation

- Ics Exams 2013 Questions SBDocument1 pageIcs Exams 2013 Questions SBDeepak ShoriPas encore d'évaluation

- Adler V Dickson The HimalayaDocument18 pagesAdler V Dickson The HimalayaDeepak ShoriPas encore d'évaluation

- Ics Exams 2013 Questions SLDocument1 pageIcs Exams 2013 Questions SLDeepak ShoriPas encore d'évaluation

- Ics Exams 2013 Questions SSPDocument2 pagesIcs Exams 2013 Questions SSPDeepak ShoriPas encore d'évaluation

- 01 IntroductiontoTransportationDocument23 pages01 IntroductiontoTransportationDeepak ShoriPas encore d'évaluation

- Shipping Finance Securitization Structure SPV IssuesDocument2 pagesShipping Finance Securitization Structure SPV IssuesDeepak Shori100% (1)

- Port Agency 2014Document3 pagesPort Agency 2014Deepak Shori100% (1)

- History, and Culture of DenmarkDocument14 pagesHistory, and Culture of DenmarkRina ApriliaPas encore d'évaluation

- Cristina Gallardo CV - English - WebDocument2 pagesCristina Gallardo CV - English - Webcgallardo88Pas encore d'évaluation

- PMT Machines LTD Inspection and Test Plan For Bogie Frame FabricationDocument6 pagesPMT Machines LTD Inspection and Test Plan For Bogie Frame FabricationAMIT SHAHPas encore d'évaluation

- Forces of Fantasy (1ed)Document127 pagesForces of Fantasy (1ed)Strogg100% (7)

- Bioethical / Legal Issues About Nursing (RA 9173)Document11 pagesBioethical / Legal Issues About Nursing (RA 9173)Richely MedezaPas encore d'évaluation

- CHRO 3.0 Lead Future HR Function India PDFDocument40 pagesCHRO 3.0 Lead Future HR Function India PDFpriteshpatel103100% (1)

- How To Get The Poor Off Our ConscienceDocument4 pagesHow To Get The Poor Off Our Conscience钟丽虹Pas encore d'évaluation

- FinTech BoguraDocument22 pagesFinTech BoguraMeraj TalukderPas encore d'évaluation

- Daddy's ChairDocument29 pagesDaddy's Chairambrosial_nectarPas encore d'évaluation

- Araneta v. Gatmaitan, 101 Phil. 328Document3 pagesAraneta v. Gatmaitan, 101 Phil. 328Bibi JumpolPas encore d'évaluation

- Vedic MythologyDocument4 pagesVedic MythologyDaniel MonteiroPas encore d'évaluation

- The Indian Navy - Inet (Officers)Document3 pagesThe Indian Navy - Inet (Officers)ANKIT KUMARPas encore d'évaluation

- PSEA Self Assessment Form - 2024 02 02 102327 - YjloDocument2 pagesPSEA Self Assessment Form - 2024 02 02 102327 - Yjlokenedy nuwaherezaPas encore d'évaluation

- Baccmass - ChordsDocument7 pagesBaccmass - ChordsYuan MasudaPas encore d'évaluation

- Seife Progress TrackerDocument4 pagesSeife Progress TrackerngilaPas encore d'évaluation

- Sunway Berhad (F) Part 2 (Page 97-189)Document93 pagesSunway Berhad (F) Part 2 (Page 97-189)qeylazatiey93_598514100% (1)

- Hamilton EssayDocument4 pagesHamilton Essayapi-463125709Pas encore d'évaluation

- Todd Pace Court DocketDocument12 pagesTodd Pace Court DocketKUTV2NewsPas encore d'évaluation

- Qustion 2020-Man QB MCQ - MAN-22509 - VI SEME 2019-20Document15 pagesQustion 2020-Man QB MCQ - MAN-22509 - VI SEME 2019-20Raees JamadarPas encore d'évaluation

- Drought in Somalia: A Migration Crisis: Mehdi Achour, Nina LacanDocument16 pagesDrought in Somalia: A Migration Crisis: Mehdi Achour, Nina LacanLiban SwedenPas encore d'évaluation

- Flexible Learning Part 1Document10 pagesFlexible Learning Part 1John Lex Sabines IgloriaPas encore d'évaluation

- RPPSN Arbour StatementDocument2 pagesRPPSN Arbour StatementJohnPhilpotPas encore d'évaluation

- Handout 2Document2 pagesHandout 2Manel AbdeljelilPas encore d'évaluation

- Reading Comprehension and Vocabulary PracticeDocument10 pagesReading Comprehension and Vocabulary Practice徐明羽Pas encore d'évaluation

- MKT201 Term PaperDocument8 pagesMKT201 Term PaperSumaiyaNoorPas encore d'évaluation

- Analyze Author's Bias and Identify Propaganda TechniquesDocument14 pagesAnalyze Author's Bias and Identify Propaganda TechniquesWinden SulioPas encore d'évaluation

- Group 1 - MM - Vanca Digital StrategyDocument10 pagesGroup 1 - MM - Vanca Digital StrategyAashna Duggal100% (1)

- Al Fara'aDocument56 pagesAl Fara'azoinasPas encore d'évaluation

- Ngulchu Thogme Zangpo - The Thirty-Seven Bodhisattva PracticesDocument184 pagesNgulchu Thogme Zangpo - The Thirty-Seven Bodhisattva PracticesMario Galle MPas encore d'évaluation

- Introduction To Contemporary World: Alan C. Denate Maed Social Science, LPTDocument19 pagesIntroduction To Contemporary World: Alan C. Denate Maed Social Science, LPTLorlie GolezPas encore d'évaluation