Vous aimerez peut-être aussi

- CPWD Accounts Question PapersDocument2 pagesCPWD Accounts Question Papersarulraj1971Pas encore d'évaluation

- CPCB DG Set Noise Emission NormsDocument6 pagesCPCB DG Set Noise Emission NormsRSPas encore d'évaluation

- Petrol and Carosin GSR 535 EDocument4 pagesPetrol and Carosin GSR 535 Earulraj1971Pas encore d'évaluation

- Concordance Table PDFDocument75 pagesConcordance Table PDFarulraj1971Pas encore d'évaluation

- Fire Finder XLS 1 PDFDocument2 pagesFire Finder XLS 1 PDFarulraj1971Pas encore d'évaluation

- Alphabet Practice PDFDocument8 pagesAlphabet Practice PDFarulraj1971Pas encore d'évaluation

- Finding The PerimeterDocument5 pagesFinding The Perimeterarulraj1971Pas encore d'évaluation

- Finding The PerimeterDocument5 pagesFinding The Perimeterarulraj1971Pas encore d'évaluation

- Chapter 10 CPWD ACCOUNTS CODEDocument46 pagesChapter 10 CPWD ACCOUNTS CODEarulraj1971Pas encore d'évaluation

- Chapter 22 CPWD ACCOUNTS CODEDocument26 pagesChapter 22 CPWD ACCOUNTS CODEarulraj1971Pas encore d'évaluation

- Chapter23 PDFDocument17 pagesChapter23 PDFarulraj1971Pas encore d'évaluation

- Chapter 21 CPWD ACCOUNTS CODEDocument1 pageChapter 21 CPWD ACCOUNTS CODEarulraj1971Pas encore d'évaluation

- Managing Cheque BooksDocument5 pagesManaging Cheque Booksarulraj1971Pas encore d'évaluation

- CPWD Accountants CodeDocument273 pagesCPWD Accountants CodeVishalagPas encore d'évaluation

- Chapter 17Document6 pagesChapter 17vijaygopal210Pas encore d'évaluation

- Chapter 20 CPWD ACCOUNTS CODEDocument2 pagesChapter 20 CPWD ACCOUNTS CODEarulraj1971Pas encore d'évaluation

- Chapter 13 CPWD ACCOUNTS CODEDocument6 pagesChapter 13 CPWD ACCOUNTS CODEarulraj1971Pas encore d'évaluation

- Chapter 6Document20 pagesChapter 6arulraj1971Pas encore d'évaluation

- Chapter 19 CPWD ACCOUNTS CODEDocument2 pagesChapter 19 CPWD ACCOUNTS CODEarulraj1971Pas encore d'évaluation

- Chapter 14 CPWD ACCOUNTS CODEDocument5 pagesChapter 14 CPWD ACCOUNTS CODEarulraj1971Pas encore d'évaluation

- Chapter 3Document8 pagesChapter 3arulraj1971Pas encore d'évaluation

- Chapter15 PDFDocument7 pagesChapter15 PDFarulraj1971Pas encore d'évaluation

- Chapter 9 CPWD ACCOUNTS CODEDocument9 pagesChapter 9 CPWD ACCOUNTS CODEarulraj1971Pas encore d'évaluation

- Chapter 18 CPWD ACCOUNTS CODEDocument5 pagesChapter 18 CPWD ACCOUNTS CODEarulraj1971Pas encore d'évaluation

- Chapter 16 CPWD ACCOUNTS CODEDocument5 pagesChapter 16 CPWD ACCOUNTS CODEarulraj1971Pas encore d'évaluation

- Chapter 12 CPWD ACCOUNTS CODEDocument2 pagesChapter 12 CPWD ACCOUNTS CODEarulraj1971Pas encore d'évaluation

- Chapter 2Document8 pagesChapter 2arulraj1971Pas encore d'évaluation

- Chapter 4Document6 pagesChapter 4arulraj1971Pas encore d'évaluation

- Chapter7 PDFDocument20 pagesChapter7 PDFarulraj1971Pas encore d'évaluation

- Chapter 11Document3 pagesChapter 11zingar85Pas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- McNETHS FOODS Egg Powder Business PlanDocument29 pagesMcNETHS FOODS Egg Powder Business PlanD J Ben UzeePas encore d'évaluation

- Differential Analysis: The Key To Decision MakingDocument26 pagesDifferential Analysis: The Key To Decision MakingEng Hinji RudgePas encore d'évaluation

- Chap 1 PDFDocument302 pagesChap 1 PDFRhayden Doguiles100% (1)

- GST Book by Rahul PDFDocument271 pagesGST Book by Rahul PDFharishPas encore d'évaluation

- Corporate Finance Assignment 3Document5 pagesCorporate Finance Assignment 3Hardeep KaurPas encore d'évaluation

- Tax Accounting: Tax On Profit of Juridical PersonsDocument42 pagesTax Accounting: Tax On Profit of Juridical PersonsBasma MohamedPas encore d'évaluation

- Complete Exhibit 3. Provide The Answers in A Table FormatDocument5 pagesComplete Exhibit 3. Provide The Answers in A Table FormatSajan Jose100% (2)

- Debt Securities MarketDocument5 pagesDebt Securities MarketXyza Faye RegaladoPas encore d'évaluation

- Ashok LeylandDocument89 pagesAshok Leylandsushanth198950% (4)

- Accounting For AttorneysDocument160 pagesAccounting For AttorneyschuenePas encore d'évaluation

- Financial Accounting IIIDocument684 pagesFinancial Accounting IIIkennedy75% (4)

- CPT Question Paper December 2015 With Answer CAknowledgeDocument26 pagesCPT Question Paper December 2015 With Answer CAknowledgerishabh jainPas encore d'évaluation

- Chapter 2 Nca Held For Sale and Discontinued OperationsDocument14 pagesChapter 2 Nca Held For Sale and Discontinued Operationslady gwaeyngPas encore d'évaluation

- Solved Twelve Years Ago Marilyn Purchased Two Lots in An UndevelopedDocument1 pageSolved Twelve Years Ago Marilyn Purchased Two Lots in An UndevelopedAnbu jaromiaPas encore d'évaluation

- Assign 5 Chapter 7 Cash Flow Analysis Answer Cabrera 2019-2020Document6 pagesAssign 5 Chapter 7 Cash Flow Analysis Answer Cabrera 2019-2020mhikeedelantar50% (2)

- Final Income TaxationDocument15 pagesFinal Income TaxationElizalen MacarilayPas encore d'évaluation

- Public Finance and Taxation Final12345Document134 pagesPublic Finance and Taxation Final12345ThomasGetye76% (29)

- HaiDocument8 pagesHaiPrajesh SrivastavaPas encore d'évaluation

- Business OutlineDocument14 pagesBusiness OutlineJao Austin BondocPas encore d'évaluation

- The Expenditure Cycle Part II: Payroll Processing and Fixed Asset ProceduresDocument30 pagesThe Expenditure Cycle Part II: Payroll Processing and Fixed Asset ProceduresabmyonisPas encore d'évaluation

- Final Practical NAVTTCDocument8 pagesFinal Practical NAVTTCParwaiz Ali JiskaniPas encore d'évaluation

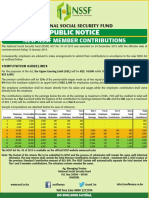

- Public Notice: New NSSF Member ContributionsDocument1 pagePublic Notice: New NSSF Member ContributionsDiana Dekatrinah KatrinePas encore d'évaluation

- Syngene Q3FY20 - RU - 23 Jan 2020Document9 pagesSyngene Q3FY20 - RU - 23 Jan 2020Doshi VaibhavPas encore d'évaluation

- LN04Brooks671956 02 LN04Document57 pagesLN04Brooks671956 02 LN04nightdazePas encore d'évaluation

- BIR Ruling 25-2002 June 25, 2002Document4 pagesBIR Ruling 25-2002 June 25, 2002Raiya Angela0% (1)

- Management Accounting/Series-4-2011 (Code3024)Document18 pagesManagement Accounting/Series-4-2011 (Code3024)Hein Linn Kyaw100% (2)

- Auditing RTP of IcaiDocument14 pagesAuditing RTP of IcaitpsbtpsbtpsbPas encore d'évaluation

- Code 2007 Accounting Level 2 2010 Series 4Document15 pagesCode 2007 Accounting Level 2 2010 Series 4apple_syih100% (1)

- Donor's Tax A) Basic Principles, Concept and DefinitionDocument4 pagesDonor's Tax A) Basic Principles, Concept and DefinitionAnonymous YNTVcDPas encore d'évaluation

- SSPOFADVDocument1 pageSSPOFADVKaren OHarePas encore d'évaluation