Vous aimerez peut-être aussi

- OMDocument11 pagesOMBishawnath RoyPas encore d'évaluation

- Sabrina SultanaDocument64 pagesSabrina SultanaMohib Ullah YousafzaiPas encore d'évaluation

- Critical Approaches To Strategic Management PDFDocument25 pagesCritical Approaches To Strategic Management PDFBishawnath RoyPas encore d'évaluation

- Balanced ScorecardDocument17 pagesBalanced ScorecardBishawnath Roy0% (1)

- Comparison Betwen VAT Act 1991 and VAT and SD Act 2012Document10 pagesComparison Betwen VAT Act 1991 and VAT and SD Act 2012Mohsena MunnaPas encore d'évaluation

- Reports Letters Email CVDocument53 pagesReports Letters Email CVBishawnath RoyPas encore d'évaluation

- 806f0f47-f773-4e09-8ce2-52082efbe311Document65 pages806f0f47-f773-4e09-8ce2-52082efbe311Bishawnath RoyPas encore d'évaluation

- MfiDocument10 pagesMfiBishawnath RoyPas encore d'évaluation

- Investing Money For Training and Development Gives Significant Returns To OrganizationDocument23 pagesInvesting Money For Training and Development Gives Significant Returns To OrganizationBishawnath RoyPas encore d'évaluation

- Bold Option in Multiple Choice Is The Correct Answer, Which Will Not Be Given in Actual QuestionDocument9 pagesBold Option in Multiple Choice Is The Correct Answer, Which Will Not Be Given in Actual QuestionBishawnath RoyPas encore d'évaluation

- BextexDocument14 pagesBextexBishawnath RoyPas encore d'évaluation

- Service Accounting SampleDocument38 pagesService Accounting SampleBishawnath RoyPas encore d'évaluation

- Xie - Yuanyuan and Hu - WeiDocument55 pagesXie - Yuanyuan and Hu - WeiVinoliaEdwinPas encore d'évaluation

- Excel Solutions To CasesDocument34 pagesExcel Solutions To CasesHoàng Thanh NguyễnPas encore d'évaluation

- Study Material For Basic English TestDocument23 pagesStudy Material For Basic English TestMinhaz Hossain OnikPas encore d'évaluation

- A Glimpse Into The Past of Selected BrandsDocument5 pagesA Glimpse Into The Past of Selected BrandsBishawnath RoyPas encore d'évaluation

- Balanced ScorecardDocument17 pagesBalanced ScorecardBishawnath Roy0% (1)

- KFC's Global Expansion and Relationship with Parent Company PepsiCoDocument14 pagesKFC's Global Expansion and Relationship with Parent Company PepsiCoEna Banda100% (1)

- Module4 Brand ResonanceDocument6 pagesModule4 Brand ResonanceBishawnath RoyPas encore d'évaluation

- Question 24251Document23 pagesQuestion 24251Bishawnath RoyPas encore d'évaluation

- Steve YoungDocument12 pagesSteve YoungMohit GoelPas encore d'évaluation

- 1 Defining Marketing For The 21 Century: Kotler KellerDocument26 pages1 Defining Marketing For The 21 Century: Kotler KellerBishawnath RoyPas encore d'évaluation

- Kentucky Fried Chicken PDFDocument21 pagesKentucky Fried Chicken PDFHohoho134Pas encore d'évaluation

- Module 1Document3 pagesModule 1Bishawnath RoyPas encore d'évaluation

- Kentucky Fried Chicken PDFDocument21 pagesKentucky Fried Chicken PDFHohoho134Pas encore d'évaluation

- Enterprise Rent A Car EditionDocument4 pagesEnterprise Rent A Car Editionjanuarius123Pas encore d'évaluation

- Module6 Choosing Brand Elements To Brand EquityDocument3 pagesModule6 Choosing Brand Elements To Brand EquityBishawnath RoyPas encore d'évaluation

- Enterprise Rent A CarDocument7 pagesEnterprise Rent A CarBishawnath RoyPas encore d'évaluation

- Songs of Innocence and of ExperienceDocument52 pagesSongs of Innocence and of ExperienceBishawnath RoyPas encore d'évaluation

- Guidance Notes For UK (External)Document3 pagesGuidance Notes For UK (External)ImoUstino ImoPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Convert Purchases to EMIs on LIC Credit CardDocument2 pagesConvert Purchases to EMIs on LIC Credit CardvijaykannamallaPas encore d'évaluation

- Definiton.: V. Interest Rate Risk (IRR) of VietinbankDocument2 pagesDefiniton.: V. Interest Rate Risk (IRR) of VietinbankQuynh Ngoc DangPas encore d'évaluation

- Sbi Esap BS Ca Oct20-15jan21Document10 pagesSbi Esap BS Ca Oct20-15jan21Minhans SrivastavaPas encore d'évaluation

- IFMR Capital: Securitizing Microloans For Non-Bank InvestorsDocument30 pagesIFMR Capital: Securitizing Microloans For Non-Bank Investorsakash srivastavaPas encore d'évaluation

- Banco Filipino v. Navarro (Escalation Clause De-Escalation Clause Is Also NECESSARY)Document3 pagesBanco Filipino v. Navarro (Escalation Clause De-Escalation Clause Is Also NECESSARY)kjhenyo218502Pas encore d'évaluation

- Resolution No 003 2020 LoanDocument4 pagesResolution No 003 2020 LoanDexter Bernardo Calanoga TignoPas encore d'évaluation

- Japan - Floro - Marcos - Sta. RomanaDocument3 pagesJapan - Floro - Marcos - Sta. RomanaMichael Maningat Capacia100% (1)

- Types of Loans: Annuity LoanDocument2 pagesTypes of Loans: Annuity LoanEvelyne BujoreanPas encore d'évaluation

- Intl LiquidityDocument3 pagesIntl LiquidityAshneet BhasinPas encore d'évaluation

- Sem 6 Monetary Economics BBA025 Prof AdityaDocument2 pagesSem 6 Monetary Economics BBA025 Prof AdityaHariom LohiaPas encore d'évaluation

- Volume 5 SFMDocument16 pagesVolume 5 SFMrajat sharmaPas encore d'évaluation

- Dayang Norita Binti Awang Bujang Lorong 2C Lorong 2C 7 Lorong 2C, JLN Tung Yee 96100, SARIKEI, SARDocument3 pagesDayang Norita Binti Awang Bujang Lorong 2C Lorong 2C 7 Lorong 2C, JLN Tung Yee 96100, SARIKEI, SARgoku sonPas encore d'évaluation

- NPA PROJECT For Surat Dist Co-Op BankDocument62 pagesNPA PROJECT For Surat Dist Co-Op BankVijay Gohil33% (3)

- The Carroltons Are Deliberating Whether To Purchase A House orDocument2 pagesThe Carroltons Are Deliberating Whether To Purchase A House ortrilocksp Singh0% (1)

- Irrevocable Special Power of AttorneyDocument2 pagesIrrevocable Special Power of AttorneyClara May PasilabanPas encore d'évaluation

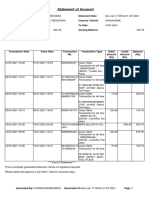

- StatementOfAccount - 1 1 21.15 1 PDFDocument1 pageStatementOfAccount - 1 1 21.15 1 PDFAmit SinghPas encore d'évaluation

- Monetary Policy Thesis TopicsDocument6 pagesMonetary Policy Thesis Topicsalisonreedphoenix100% (2)

- Growth of PayTM in IndiaDocument90 pagesGrowth of PayTM in IndiaGeetansh Bangard100% (3)

- Promotion Study Material - Clerk To JMG.s-1 - 2016Document403 pagesPromotion Study Material - Clerk To JMG.s-1 - 2016JitenPas encore d'évaluation

- STRBI Table No. 02 Earnings and Expenses of Scheduled Commercial BanksDocument466 pagesSTRBI Table No. 02 Earnings and Expenses of Scheduled Commercial BanksSai KishorePas encore d'évaluation

- All About NPA'sDocument6 pagesAll About NPA'sVishnu KumarPas encore d'évaluation

- HDFC Bank's Financial Performance During CovidDocument21 pagesHDFC Bank's Financial Performance During CovidSasi Samhitha KPas encore d'évaluation

- Question 2 (1 Point) : SavedDocument24 pagesQuestion 2 (1 Point) : SavedMs VampirePas encore d'évaluation

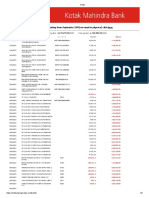

- Kotak Bank statement details for period 10/04/2021 - 14/04/2021Document2 pagesKotak Bank statement details for period 10/04/2021 - 14/04/2021Tushar GuptaPas encore d'évaluation

- Account2 BDocument20 pagesAccount2 BamitpriyashankarPas encore d'évaluation

- HDFC Third Party Transfer Activate FormDocument2 pagesHDFC Third Party Transfer Activate FormPankaj Batra100% (13)

- Chapter 10 Conduct of Monetary Policy (Chapter 10) MishkinDocument82 pagesChapter 10 Conduct of Monetary Policy (Chapter 10) MishkinethandanfordPas encore d'évaluation

- Intership ReportttttttDocument29 pagesIntership Reportttttttsehrish MalikPas encore d'évaluation

- The Money Masters - ReportDocument59 pagesThe Money Masters - ReportSamiyaIllias100% (2)

- Chapter 14 Audit of Cash and Bank BalancesDocument14 pagesChapter 14 Audit of Cash and Bank BalancesChristian LimPas encore d'évaluation