Vous aimerez peut-être aussi

- Acct1511 Final VersionDocument29 pagesAcct1511 Final VersioncarolinetsangPas encore d'évaluation

- Acct1511 Final VersionDocument27 pagesAcct1511 Final VersioncarolinetsangPas encore d'évaluation

- Final Exam f02Document13 pagesFinal Exam f02Omar Ahmed ElkhalilPas encore d'évaluation

- Financial Management: Thursday 9 June 2011Document9 pagesFinancial Management: Thursday 9 June 2011catcat1122Pas encore d'évaluation

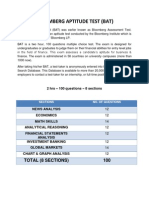

- Bloomberg Aptitude Test (BAT)Document10 pagesBloomberg Aptitude Test (BAT)Shivgan Joshi100% (1)

- Basic Financial Statements Analysis DoneDocument17 pagesBasic Financial Statements Analysis DoneAjmal SalamPas encore d'évaluation

- Assignment May2011 ADocument6 pagesAssignment May2011 AZyn Wann HoPas encore d'évaluation

- Question 1 (40marks - 48 Minutes)Document8 pagesQuestion 1 (40marks - 48 Minutes)dianimPas encore d'évaluation

- Lesson 1Document8 pagesLesson 1Amangeldi SalimzhanovPas encore d'évaluation

- IF1 - Practice ProblemsDocument198 pagesIF1 - Practice ProblemssaikrishnavnPas encore d'évaluation

- Level 1 - Financial StatementDocument11 pagesLevel 1 - Financial StatementVimmi BanuPas encore d'évaluation

- 2011 End of Session ExaminationDocument7 pages2011 End of Session Examinationleolau2015Pas encore d'évaluation

- Cat/fia (FFM)Document9 pagesCat/fia (FFM)theizzatirosli100% (1)

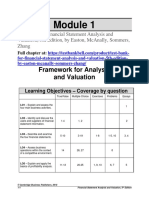

- Test Bank For Financial Statement Analysis and Valuation 2nd Edition EastonDocument29 pagesTest Bank For Financial Statement Analysis and Valuation 2nd Edition Eastonagnesgrainneo30Pas encore d'évaluation

- Using Bloomberg To Get The Data You NeedDocument36 pagesUsing Bloomberg To Get The Data You Needte_gantengPas encore d'évaluation

- Comm 217 ProjectDocument3 pagesComm 217 Projectthemichaelmccarthy12Pas encore d'évaluation

- CH 3 - The Statement of Financial Position and Financial DisclosuresDocument37 pagesCH 3 - The Statement of Financial Position and Financial DisclosuresZulqarnain KhokharPas encore d'évaluation

- Acct1511 Final VersionDocument33 pagesAcct1511 Final VersioncarolinetsangPas encore d'évaluation

- Comprehensive ExamDocument37 pagesComprehensive ExamAngeline DionicioPas encore d'évaluation

- Acp5efm13 J CombinedDocument36 pagesAcp5efm13 J CombinedHan HowPas encore d'évaluation

- Model Paper Financial AccountingDocument6 pagesModel Paper Financial AccountingzurwahmirzaPas encore d'évaluation

- Financial AccountingDocument66 pagesFinancial AccountingFaisal SaleemPas encore d'évaluation

- Test Bank For Financial Statement Analysis and Valuation 5th Edition by Easton Mcanally Sommers ZhangDocument30 pagesTest Bank For Financial Statement Analysis and Valuation 5th Edition by Easton Mcanally Sommers Zhangagnesgrainneo30100% (1)

- Test Bank For Financial Statement Analysis and Valuation 5th Edition by Easton Mcanally Sommers ZhangDocument30 pagesTest Bank For Financial Statement Analysis and Valuation 5th Edition by Easton Mcanally Sommers ZhangLucille Alexander100% (37)

- ACCT 201 Exam 1Document16 pagesACCT 201 Exam 1Steve ZaluchaPas encore d'évaluation

- The Home DepotDocument14 pagesThe Home DepotDaniel NastasePas encore d'évaluation

- Bloomberg Aptitude TestDocument35 pagesBloomberg Aptitude TestShivgan Joshi100% (1)

- Report Banking RiabkovDocument6 pagesReport Banking RiabkovKostia RiabkovPas encore d'évaluation

- Impairment 10tipsDocument13 pagesImpairment 10tipsTindo MoyoPas encore d'évaluation

- Financial Managemnet 3B LAO 2020 FinalDocument11 pagesFinancial Managemnet 3B LAO 2020 Finalsabelo.j.nkosi.5Pas encore d'évaluation

- Georgetown Case Competition: ConfidentialDocument17 pagesGeorgetown Case Competition: ConfidentialPatrick BensonPas encore d'évaluation

- ACCT504 Case Study 1Document15 pagesACCT504 Case Study 1sinbad97100% (1)

- WSJ Jpmfiling0510Document191 pagesWSJ Jpmfiling0510Reza Abusaidi100% (1)

- FR MJ23 Examiner's Report - FINALDocument24 pagesFR MJ23 Examiner's Report - FINALdeepshikhagupta514Pas encore d'évaluation

- Fin 621 Final Term Papers 99 25 Sure Solved 2Document78 pagesFin 621 Final Term Papers 99 25 Sure Solved 2Javaid IqbalPas encore d'évaluation

- Accounting 201 FALL 2000 Exam 2Document11 pagesAccounting 201 FALL 2000 Exam 2Corey ArmstrongPas encore d'évaluation

- Chapter 3Document17 pagesChapter 3Phan Anh HaoPas encore d'évaluation

- Capital Markets & Investments - BGK Chapter 1Document46 pagesCapital Markets & Investments - BGK Chapter 1张泷颢Pas encore d'évaluation

- Examiner's Report: F3/FFA Financial Accounting June 2012Document4 pagesExaminer's Report: F3/FFA Financial Accounting June 2012Ahmad Hafid HanifahPas encore d'évaluation

- M8 PracticeDocument22 pagesM8 PracticeleeminleePas encore d'évaluation

- Ba 623 Case AnalysisDocument8 pagesBa 623 Case AnalysisSarah Jane OrillosaPas encore d'évaluation

- F551 A01Document11 pagesF551 A01Osman AnwarPas encore d'évaluation

- Acct 504 Week 8 Final Exam All 4 Sets - DevryDocument17 pagesAcct 504 Week 8 Final Exam All 4 Sets - Devrycoursehomework0% (1)

- Acct1511 2013s2c2 Handout 2 PDFDocument19 pagesAcct1511 2013s2c2 Handout 2 PDFcelopurplePas encore d'évaluation

- Loan-Loss Provisions of Commercial Banks and Adequate Disclosure: A NoteDocument7 pagesLoan-Loss Provisions of Commercial Banks and Adequate Disclosure: A NoteabhinavatripathiPas encore d'évaluation

- Acct3708 Finals, Sem 2, 2010Document11 pagesAcct3708 Finals, Sem 2, 2010nessawhoPas encore d'évaluation

- Chapter 17Document48 pagesChapter 17Shiv NarayanPas encore d'évaluation

- Intermediate Accounting Kieso 13e Comp. TestDocument13 pagesIntermediate Accounting Kieso 13e Comp. TestRJKcPas encore d'évaluation

- Multiple Choice Questions: Section-IDocument6 pagesMultiple Choice Questions: Section-Isah108_pk796Pas encore d'évaluation

- Multiple Choice Questions: Section-IDocument6 pagesMultiple Choice Questions: Section-ItysonhishamPas encore d'évaluation

- Module 6 Ratio Analysis and InterpretationDocument9 pagesModule 6 Ratio Analysis and InterpretationHeart MacedaPas encore d'évaluation

- Accounting Ratio PDFDocument10 pagesAccounting Ratio PDFMuhammad KaleemPas encore d'évaluation

- f9 2014 Dec QDocument13 pagesf9 2014 Dec QreadtometooPas encore d'évaluation

- Handbook of Basel III Capital: Enhancing Bank Capital in PracticeD'EverandHandbook of Basel III Capital: Enhancing Bank Capital in PracticePas encore d'évaluation

- The Essentials of Finance and Accounting for Nonfinancial ManagersD'EverandThe Essentials of Finance and Accounting for Nonfinancial ManagersÉvaluation : 5 sur 5 étoiles5/5 (1)

- Consumer Lending Revenues World Summary: Market Values & Financials by CountryD'EverandConsumer Lending Revenues World Summary: Market Values & Financials by CountryPas encore d'évaluation

- Miscellaneous Nondepository Credit Intermediation Revenues World Summary: Market Values & Financials by CountryD'EverandMiscellaneous Nondepository Credit Intermediation Revenues World Summary: Market Values & Financials by CountryPas encore d'évaluation

- Cost of Doing Business Study, 2012 EditionD'EverandCost of Doing Business Study, 2012 EditionPas encore d'évaluation

- Secondary Market Financing Revenues World Summary: Market Values & Financials by CountryD'EverandSecondary Market Financing Revenues World Summary: Market Values & Financials by CountryPas encore d'évaluation

- Measuring Business Interruption Losses and Other Commercial Damages: An Economic ApproachD'EverandMeasuring Business Interruption Losses and Other Commercial Damages: An Economic ApproachPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.29Document1 pageWeek 9 Portfolio Performance Evaluation - Color.29jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.23Document1 pageWeek 9 Portfolio Performance Evaluation - Color.23jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.28Document1 pageWeek 9 Portfolio Performance Evaluation - Color.28jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.27Document1 pageWeek 9 Portfolio Performance Evaluation - Color.27jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.24Document1 pageWeek 9 Portfolio Performance Evaluation - Color.24jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.22Document1 pageWeek 9 Portfolio Performance Evaluation - Color.22jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.26Document1 pageWeek 9 Portfolio Performance Evaluation - Color.26jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.25Document1 pageWeek 9 Portfolio Performance Evaluation - Color.25jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.18Document1 pageWeek 9 Portfolio Performance Evaluation - Color.18jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.19Document1 pageWeek 9 Portfolio Performance Evaluation - Color.19jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.20Document1 pageWeek 9 Portfolio Performance Evaluation - Color.20jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.21Document1 pageWeek 9 Portfolio Performance Evaluation - Color.21jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.16Document1 pageWeek 9 Portfolio Performance Evaluation - Color.16jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.17Document1 pageWeek 9 Portfolio Performance Evaluation - Color.17jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.11Document1 pageWeek 9 Portfolio Performance Evaluation - Color.11jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.10Document1 pageWeek 9 Portfolio Performance Evaluation - Color.10jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.13Document1 pageWeek 9 Portfolio Performance Evaluation - Color.13jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.15Document1 pageWeek 9 Portfolio Performance Evaluation - Color.15jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.14Document1 pageWeek 9 Portfolio Performance Evaluation - Color.14jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.12Document1 pageWeek 9 Portfolio Performance Evaluation - Color.12jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.6Document1 pageWeek 9 Portfolio Performance Evaluation - Color.6jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.9Document1 pageWeek 9 Portfolio Performance Evaluation - Color.9jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.8Document1 pageWeek 9 Portfolio Performance Evaluation - Color.8jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.5Document1 pageWeek 9 Portfolio Performance Evaluation - Color.5jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.2Document1 pageWeek 9 Portfolio Performance Evaluation - Color.2jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.7Document1 pageWeek 9 Portfolio Performance Evaluation - Color.7jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.3Document1 pageWeek 9 Portfolio Performance Evaluation - Color.3jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.4Document1 pageWeek 9 Portfolio Performance Evaluation - Color.4jonPas encore d'évaluation

- Week 9 Portfolio Performance Evaluation - Color.1Document1 pageWeek 9 Portfolio Performance Evaluation - Color.1jonPas encore d'évaluation

- CAPMDocument30 pagesCAPMleolau2015Pas encore d'évaluation

- AKKU Annual Report 2016Document141 pagesAKKU Annual Report 2016Doli Dui TilfaPas encore d'évaluation

- Financial Ratio AnalysisDocument18 pagesFinancial Ratio Analysissarangpethe100% (4)

- Chapter 3 BecDocument11 pagesChapter 3 BecStephen ZhaoPas encore d'évaluation

- Maths Project: Planning A Home BudgetDocument10 pagesMaths Project: Planning A Home BudgetFaiz100% (8)

- Acct 04AHW Exercises Chapter1Document3 pagesAcct 04AHW Exercises Chapter1Chris Trevino100% (2)

- Hindustan Oil Exploration Company Limited: Transforming Through Talent and Technology 2016-2017Document34 pagesHindustan Oil Exploration Company Limited: Transforming Through Talent and Technology 2016-2017HarveyPas encore d'évaluation

- 2019 Study Plan For CPAsDocument30 pages2019 Study Plan For CPAsFreann Sharisse AustriaPas encore d'évaluation

- Costco Comprehensive AnalysisDocument11 pagesCostco Comprehensive AnalysisAlex GaoPas encore d'évaluation

- Q2-21: Natura &co Reports Strong +36% Growth, Continuing To Outperform The CFT Market, With Net Income Increasing To R$235 MillionDocument46 pagesQ2-21: Natura &co Reports Strong +36% Growth, Continuing To Outperform The CFT Market, With Net Income Increasing To R$235 MillionRenan Dantas SantosPas encore d'évaluation

- Euromonitor - Industry Capsules - Movie Theatres in India - ISIC 9212Document13 pagesEuromonitor - Industry Capsules - Movie Theatres in India - ISIC 9212shubhamwaghadhare100% (1)

- Q8Document4 pagesQ8Sundaramani Saran100% (1)

- Department of Financial Accounting Fac2601: Financial Accounting For CompaniesDocument63 pagesDepartment of Financial Accounting Fac2601: Financial Accounting For CompaniesPhebieon MukwenhaPas encore d'évaluation

- Power Notes: BudgetingDocument46 pagesPower Notes: BudgetingfrostyangelPas encore d'évaluation

- Accounting For NPOsDocument3 pagesAccounting For NPOsRaven BermalPas encore d'évaluation

- Project KhalidDocument68 pagesProject Khalidsnazim88100% (1)

- 12 - Incomplete Record - With - AnswerDocument13 pages12 - Incomplete Record - With - AnswerAbid faisal AhmedPas encore d'évaluation

- Financial AnalysisDocument12 pagesFinancial AnalysisTrisha Lane AtienzaPas encore d'évaluation

- MATH - REVIEW - SECOND - PHASE - 1 - .PDF Filename UTF-8''MATH - REVIEW - SECOND - PHASEDocument54 pagesMATH - REVIEW - SECOND - PHASE - 1 - .PDF Filename UTF-8''MATH - REVIEW - SECOND - PHASEAlaminPas encore d'évaluation

- CHAP05Document48 pagesCHAP05Trúc NenokonPas encore d'évaluation

- Customer Loyalty ProgrammesDocument3 pagesCustomer Loyalty ProgrammesStacy SmithPas encore d'évaluation

- Dominos+Pizza+Financial+Model+v1 TemplateDocument5 pagesDominos+Pizza+Financial+Model+v1 TemplateEmperor OverwatchPas encore d'évaluation

- Release: 2 Quarter of 2021Document29 pagesRelease: 2 Quarter of 2021Rafa BorgesPas encore d'évaluation

- Financial Statement AnalysisDocument31 pagesFinancial Statement AnalysisbilalahmedbhuttoPas encore d'évaluation

- Income Statement and Balance SheetDocument25 pagesIncome Statement and Balance SheetKhizer Waseem100% (1)

- Morebusiness Entertainment Business Plan TemplateDocument11 pagesMorebusiness Entertainment Business Plan TemplateToluwalope Sammie-Junior BanjoPas encore d'évaluation

- Rofitability Position of Sanakishan Kirsi Sahakari Santha, Kailali, NepalDocument32 pagesRofitability Position of Sanakishan Kirsi Sahakari Santha, Kailali, NepalKAMAL POKHRELPas encore d'évaluation

- Hwhwwjwjwjwjwjwiwiwiwkke Cpa Review School of The Philippines Manila Corporations Dela Cruz / de Vera / Lopez / LlamadoDocument9 pagesHwhwwjwjwjwjwjwiwiwiwkke Cpa Review School of The Philippines Manila Corporations Dela Cruz / de Vera / Lopez / LlamadoSophia PerezPas encore d'évaluation

- Makati City v. Metro Pacific Investments Corp. - Holding Company Not Subject To LBTDocument24 pagesMakati City v. Metro Pacific Investments Corp. - Holding Company Not Subject To LBTYuPas encore d'évaluation

- 2020 Dec. MIDTRM EXAM BSA 3A Accounting For Got. NPODocument6 pages2020 Dec. MIDTRM EXAM BSA 3A Accounting For Got. NPOVernn100% (1)

- Pi ChartsDocument24 pagesPi Chartsdivy0% (1)