Vous aimerez peut-être aussi

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Taxation CPALE by WMGDocument19 pagesTaxation CPALE by WMGJona Celle Castillo100% (1)

- 10 Task PerformanceDocument5 pages10 Task Performancejeffersam31Pas encore d'évaluation

- Taxation - Income TaxDocument158 pagesTaxation - Income Taxnaren197667% (6)

- Week 4 P4.21 Modified Question PDFDocument1 pageWeek 4 P4.21 Modified Question PDFalexandraPas encore d'évaluation

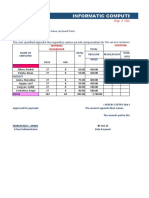

- Payroll: Informatic Computer Institute of Agusan Del SurDocument4 pagesPayroll: Informatic Computer Institute of Agusan Del SurJulius SalasPas encore d'évaluation

- FW 8 Ben 2Document1 pageFW 8 Ben 2DCOM SoftwaresPas encore d'évaluation

- Incorporation Certificate - Lightning NodeDocument1 pageIncorporation Certificate - Lightning NodeJustin LimPas encore d'évaluation

- Philippine Airlines, Inc. Vs The Secretary of Finance and Commissioner of Internal RevenueDocument1 pagePhilippine Airlines, Inc. Vs The Secretary of Finance and Commissioner of Internal RevenueAaliyah AndreaPas encore d'évaluation

- Income Tax Payment Challan: PSID #: 42079719Document1 pageIncome Tax Payment Challan: PSID #: 42079719gandapur khanPas encore d'évaluation

- Z Belay ZewudeDocument102 pagesZ Belay ZewudeamanualPas encore d'évaluation

- 1 CPA Review School of The Philippines Manila General Principles of Taxation Dela Cruz/De Vera/Lopez/LlamadoDocument20 pages1 CPA Review School of The Philippines Manila General Principles of Taxation Dela Cruz/De Vera/Lopez/LlamadoJolianne SalvadoOfcPas encore d'évaluation

- Contoh Soal Laporan Arus KasDocument2 pagesContoh Soal Laporan Arus KasRidwanPas encore d'évaluation

- Shree Motors Agencies Private Limited (Unit II) : Service/Repair EstimateDocument2 pagesShree Motors Agencies Private Limited (Unit II) : Service/Repair Estimateboobalan_shriPas encore d'évaluation

- MGMT3052 Taxation & Tax Management (UWI)Document6 pagesMGMT3052 Taxation & Tax Management (UWI)payel02000100% (1)

- Income Tax Numericals SolutionsDocument9 pagesIncome Tax Numericals SolutionsBrown BoiPas encore d'évaluation

- Mattress InvoiceDocument1 pageMattress InvoiceSMPas encore d'évaluation

- Internet JuneDocument1 pageInternet JuneUgesh ReddyPas encore d'évaluation

- Ghana Revenue Authority: Monthly Vat & Nhil ReturnDocument2 pagesGhana Revenue Authority: Monthly Vat & Nhil Returnokatakyie1990Pas encore d'évaluation

- JOHN H. OSMEÑA, Petitioner, vs. OSCAR ORBOS, in His Capacity AsDocument2 pagesJOHN H. OSMEÑA, Petitioner, vs. OSCAR ORBOS, in His Capacity AsMonikkaPas encore d'évaluation

- DaasdasddDocument2 pagesDaasdasddHarDik PatelPas encore d'évaluation

- Fort Bonifacio Development Vs CIR GR No 158885Document3 pagesFort Bonifacio Development Vs CIR GR No 158885Alfonso Dimla100% (1)

- Wickliffe Schools Levy HistoryDocument4 pagesWickliffe Schools Levy HistoryThe News-HeraldPas encore d'évaluation

- All About Annual Information Statement (AIS)Document79 pagesAll About Annual Information Statement (AIS)NEERAJ MAURYAPas encore d'évaluation

- Master NotesDocument270 pagesMaster NotesdavidcleePas encore d'évaluation

- Accounting Chapter 10Document4 pagesAccounting Chapter 1019033Pas encore d'évaluation

- Pascual vs. DragonDocument2 pagesPascual vs. DragonRussell John HipolitoPas encore d'évaluation

- Compare and Contrast Four Forms of Business OwnershipDocument2 pagesCompare and Contrast Four Forms of Business OwnershipAlma McCauleyPas encore d'évaluation

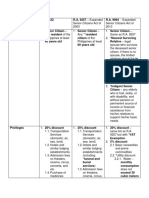

- Title R.A. 7432 R.A. 9257 R.A. 9994 - ExpandedDocument11 pagesTitle R.A. 7432 R.A. 9257 R.A. 9994 - ExpandedAngel Alejo AcobaPas encore d'évaluation

- Evaluation Tax Assessment and Collection Practice of Category "C" Tax Payers The Case of Nefas Silk Nifas Silk Lafto Sub City Woreda 01Document56 pagesEvaluation Tax Assessment and Collection Practice of Category "C" Tax Payers The Case of Nefas Silk Nifas Silk Lafto Sub City Woreda 01Nate WorkPas encore d'évaluation

- Gail & BradDocument2 pagesGail & BradAbid AliPas encore d'évaluation