Vous aimerez peut-être aussi

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The International Comparative Legal Guide To - Real Estate 2015Document13 pagesThe International Comparative Legal Guide To - Real Estate 2015Panos KolPas encore d'évaluation

- Questionnaire FOR LOANS AND ADVANCESDocument4 pagesQuestionnaire FOR LOANS AND ADVANCEStulasinad12371% (7)

- Risk Bearing Documents in International TradeDocument8 pagesRisk Bearing Documents in International TradeSukrut BoradePas encore d'évaluation

- Simple InterestDocument27 pagesSimple Interestleslie0% (1)

- Mpanzi Sacco Strategic PlanDocument39 pagesMpanzi Sacco Strategic Planna100% (2)

- HDFC FinalDocument19 pagesHDFC FinalLavina JainPas encore d'évaluation

- Assignment 1 - Individual Assignment Fin430Document7 pagesAssignment 1 - Individual Assignment Fin430NURMISHA AQMA SOFIA SELAMATPas encore d'évaluation

- Icici Subsidiaries Ar 2015 16Document492 pagesIcici Subsidiaries Ar 2015 16RAHIM KHANPas encore d'évaluation

- Income Tax Declaration FormDocument1 pageIncome Tax Declaration Formdiwakar1978Pas encore d'évaluation

- Principles of TakafulDocument3 pagesPrinciples of TakafulMuhamad NazriPas encore d'évaluation

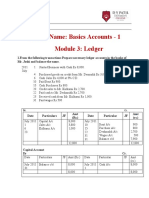

- Assignment Module 3 LedgerDocument3 pagesAssignment Module 3 LedgerPRINCE100% (1)

- Questionnaire Impact of E-Commerce On Purchase Behavior of Student in Higher Education: A Study of CSJMU KanpurDocument2 pagesQuestionnaire Impact of E-Commerce On Purchase Behavior of Student in Higher Education: A Study of CSJMU KanpurarpitPas encore d'évaluation

- Chapter6E2010 PDFDocument12 pagesChapter6E2010 PDFutcm77Pas encore d'évaluation

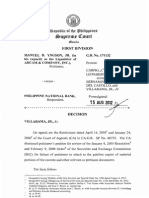

- PHILIPPINE EDUCATION CO., INC., Plaintiff-Appellant, vs. MAURICIO A. SORIANO, ET AL., Defendants-AppelleesDocument6 pagesPHILIPPINE EDUCATION CO., INC., Plaintiff-Appellant, vs. MAURICIO A. SORIANO, ET AL., Defendants-AppelleesKing BadongPas encore d'évaluation

- Principles of Banking Regulation: More InformationDocument19 pagesPrinciples of Banking Regulation: More InformationAnirudhAdityaPas encore d'évaluation

- Fintech Report 2019Document28 pagesFintech Report 2019Nadeem KhanPas encore d'évaluation

- Mortgages ExposedDocument130 pagesMortgages ExposedsatstarPas encore d'évaluation

- Building Business CreditDocument90 pagesBuilding Business Credithalcino100% (1)

- Service FeesDocument1 pageService FeesWayne ChuPas encore d'évaluation

- Yngson CaseDocument10 pagesYngson CaseKim EsmeñaPas encore d'évaluation

- Question Text: AnswerDocument5 pagesQuestion Text: AnswerIan Nicole SalvadorPas encore d'évaluation

- Measurement of Interest - SlidesDocument47 pagesMeasurement of Interest - SlidesSamir Arun BhucharPas encore d'évaluation

- Ra 7653Document17 pagesRa 7653Sherna Adil100% (2)

- SecuritisationDocument28 pagesSecuritisationPratik MehtaPas encore d'évaluation

- BSA ManualDocument60 pagesBSA ManualSFLDPas encore d'évaluation

- Loan Account Statement For LCDMUM0005095101Document3 pagesLoan Account Statement For LCDMUM0005095101Girish LunaviyaPas encore d'évaluation

- FASTag - Statement1032014763720200501124625793 - OW PDFDocument4 pagesFASTag - Statement1032014763720200501124625793 - OW PDFNarasimha SandakaPas encore d'évaluation

- Different Areas of Frauds in BanksDocument4 pagesDifferent Areas of Frauds in BanksKush SinghPas encore d'évaluation

- A Thesis On Correlation Between Customer Services and Its Satisfaction Level in HDFC BankDocument52 pagesA Thesis On Correlation Between Customer Services and Its Satisfaction Level in HDFC Bankbittu jain100% (1)

- 13-01-24 Complaint No 3 Against Bank HaPoalim, Filed With Bank of Israel, Alleging Organized Corporate CrimeDocument3 pages13-01-24 Complaint No 3 Against Bank HaPoalim, Filed With Bank of Israel, Alleging Organized Corporate CrimeHuman Rights Alert - NGO (RA)Pas encore d'évaluation