Vous aimerez peut-être aussi

- Travel Reimbursement Form: (Attach Photocopy of Tickets and Boarding Pass As Applicable)Document6 pagesTravel Reimbursement Form: (Attach Photocopy of Tickets and Boarding Pass As Applicable)Sambit MishraPas encore d'évaluation

- Data Science DomainsDocument1 pageData Science DomainsSambit MishraPas encore d'évaluation

- Indian Art HistoryDocument13 pagesIndian Art HistorySambit MishraPas encore d'évaluation

- Bring Out The Differences and Similarities Between Endogenous Growth Models and Exogenous Growth ModelsDocument4 pagesBring Out The Differences and Similarities Between Endogenous Growth Models and Exogenous Growth ModelssatgurupreetkaurPas encore d'évaluation

- 109Document8 pages109Sambit MishraPas encore d'évaluation

- BS Assignment 2Document4 pagesBS Assignment 2Sambit MishraPas encore d'évaluation

- A Local Officials Guide To Online Public Engagement 0Document28 pagesA Local Officials Guide To Online Public Engagement 0Sambit MishraPas encore d'évaluation

- Indian Craft TraditionDocument5 pagesIndian Craft TraditionSambit MishraPas encore d'évaluation

- Subsidies vs Cash Transfers: Pros and ConsDocument1 pageSubsidies vs Cash Transfers: Pros and ConsRajaDurai RamakrishnanPas encore d'évaluation

- Inclusive Growth 1Document24 pagesInclusive Growth 1sagar81285Pas encore d'évaluation

- Assignment DetailsDocument6 pagesAssignment DetailsSambit MishraPas encore d'évaluation

- Delivering Infrastructure Solutions through PPPsDocument67 pagesDelivering Infrastructure Solutions through PPPsSambit MishraPas encore d'évaluation

- Nuclear ProliferationDocument12 pagesNuclear ProliferationDevendrapratapdpPas encore d'évaluation

- Chapter 11 Exercise AnswersDocument16 pagesChapter 11 Exercise Answershimelwork100% (1)

- 1475 Exam Schedule-ET (Revised)Document2 pages1475 Exam Schedule-ET (Revised)Sambit MishraPas encore d'évaluation

- Fin Sight Oct2012Document3 pagesFin Sight Oct2012Sambit MishraPas encore d'évaluation

- India Wealth Report 2014Document46 pagesIndia Wealth Report 2014Thirumalai KrishnasamyPas encore d'évaluation

- 9705 - Handouts Sessions 12 FactoringDocument4 pages9705 - Handouts Sessions 12 FactoringSambit MishraPas encore d'évaluation

- CS406 Information Security Risk Assessme United States Government AccountabilityDocument50 pagesCS406 Information Security Risk Assessme United States Government AccountabilityMili ShahPas encore d'évaluation

- 4914 - Case Study - 1 - RPGDocument3 pages4914 - Case Study - 1 - RPGSambit Mishra100% (1)

- Sustainable Dev TranscriptDocument3 pagesSustainable Dev TranscriptSambit MishraPas encore d'évaluation

- Jean Louis PE Model Without SolutionDocument58 pagesJean Louis PE Model Without SolutionSambit MishraPas encore d'évaluation

- Analysis SportsWearDocument29 pagesAnalysis SportsWearSambit MishraPas encore d'évaluation

- Hedge FundDocument1 pageHedge FundSambit MishraPas encore d'évaluation

- DUPont and Technical AnalysisDocument2 pagesDUPont and Technical AnalysisSambit MishraPas encore d'évaluation

- ITS Cloud RoadmapDocument2 pagesITS Cloud RoadmapSambit MishraPas encore d'évaluation

- Mis Social Roi TB Cost of RXDocument9 pagesMis Social Roi TB Cost of RXSambit MishraPas encore d'évaluation

- Mis Social Roi TB Cost of RXDocument9 pagesMis Social Roi TB Cost of RXSambit MishraPas encore d'évaluation

- Human Activity Clustering with SmartphonesDocument18 pagesHuman Activity Clustering with Smartphonesniti860Pas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5782)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- ACCP 5000 Test 2 Review ClassDocument26 pagesACCP 5000 Test 2 Review ClassDang ThanhPas encore d'évaluation

- Using Vocabulary in Business and EconomicsDocument13 pagesUsing Vocabulary in Business and EconomicsKashani100% (1)

- Sample Demand LetterDocument2 pagesSample Demand LetterDamanMandaPas encore d'évaluation

- UFONE HRM ReportDocument44 pagesUFONE HRM ReportToûƧȝȝfIqßalMûghÅl100% (1)

- #22 Revaluation & Impairment (Notes For 6206)Document5 pages#22 Revaluation & Impairment (Notes For 6206)Claudine DuhapaPas encore d'évaluation

- Commercial Banks - Meaning and FunctionsDocument4 pagesCommercial Banks - Meaning and FunctionsCharu Saxena16Pas encore d'évaluation

- Templates of Credit Rebuilding LettersDocument27 pagesTemplates of Credit Rebuilding LettersBobby67% (3)

- Evidence of Life Evidence of Person Entitled To PaymentDocument5 pagesEvidence of Life Evidence of Person Entitled To Paymentjoe89% (9)

- Padgett Paper Products Case StudyDocument7 pagesPadgett Paper Products Case StudyDavey FranciscoPas encore d'évaluation

- Simple Interest Compounded Interest Population Growth Half LifeDocument32 pagesSimple Interest Compounded Interest Population Growth Half LifeCarmen GoguPas encore d'évaluation

- Rental Application FormDocument3 pagesRental Application FormNyasha SvondoPas encore d'évaluation

- Transfer of Property ActDocument8 pagesTransfer of Property ActAnkush JadaunPas encore d'évaluation

- Purple Line Extension Contract RevisedDocument20 pagesPurple Line Extension Contract RevisedMetro Los AngelesPas encore d'évaluation

- Hardin Living Within Limits CH 8Document25 pagesHardin Living Within Limits CH 8arif420_999Pas encore d'évaluation

- BLDocument4 pagesBLBBirdMozyPas encore d'évaluation

- Answer Key - First YearDocument10 pagesAnswer Key - First YearJohnAllenMarillaPas encore d'évaluation

- Comaprative Financial Statment Analysis of HBL & MCBDocument28 pagesComaprative Financial Statment Analysis of HBL & MCBIfzal Ahmad86% (7)

- Comparing Home Loans Across Top BanksDocument55 pagesComparing Home Loans Across Top BanksShikha Wadwa0% (1)

- Apply for MRI/SRI claimDocument2 pagesApply for MRI/SRI claimEliavena AmorPas encore d'évaluation

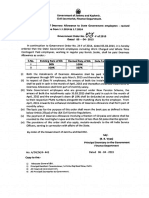

- J&K Govt Revises DA Rates for EmployeesDocument2 pagesJ&K Govt Revises DA Rates for EmployeesShowkat Ahmad LonePas encore d'évaluation

- Opening Case - Dilemma of Vishal JhulkaDocument2 pagesOpening Case - Dilemma of Vishal JhulkaSurbhi SabharwalPas encore d'évaluation

- Jamie McIntyre - What I Didn't Learn at School But Wish I HadDocument12 pagesJamie McIntyre - What I Didn't Learn at School But Wish I HadJamie McIntyre100% (3)

- Industrial Development Bank of IndiaDocument10 pagesIndustrial Development Bank of Indiabackupsanthosh21 dataPas encore d'évaluation

- Tata Motors Company ProfileDocument17 pagesTata Motors Company Profilesanjayy221Pas encore d'évaluation

- 07 - AUDIT OF NBFCsDocument17 pages07 - AUDIT OF NBFCsRavi RothiPas encore d'évaluation

- Selling With Emotional IntelligenceDocument274 pagesSelling With Emotional IntelligenceReyaz Mohemmad0% (1)

- 1MDB SagaDocument4 pages1MDB SagaJingyi SaysHelloPas encore d'évaluation

- City of Boise Idaho Checks 33Document32 pagesCity of Boise Idaho Checks 33Mark ReinhardtPas encore d'évaluation

- Received From (Client Name) Amount $: ReceiptDocument2 pagesReceived From (Client Name) Amount $: ReceiptAngellaPas encore d'évaluation

- 12-International Institutions and Role in International BusinessDocument13 pages12-International Institutions and Role in International Businessfrediz7971% (7)