Vous aimerez peut-être aussi

- Evaluation of Cba - Venera VladDocument11 pagesEvaluation of Cba - Venera VladcataromiPas encore d'évaluation

- The Perfect TimingDocument15 pagesThe Perfect TimingAlexandru VasilePas encore d'évaluation

- Foi 11 38 Procurement Process ReviewDocument41 pagesFoi 11 38 Procurement Process ReviewSaid AliPas encore d'évaluation

- Workshop3 1Document22 pagesWorkshop3 1lciacob4647Pas encore d'évaluation

- RegionalDocument28 pagesRegionalTheodore KoukoulisPas encore d'évaluation

- Training ManualDocument45 pagesTraining ManualbezawitwubshetPas encore d'évaluation

- Summary Benchmarking Bi 2002 2345Document15 pagesSummary Benchmarking Bi 2002 2345JessikarmPas encore d'évaluation

- About EU GrantsDocument29 pagesAbout EU GrantsEmilPas encore d'évaluation

- 2019 CPD BookletDocument64 pages2019 CPD Bookletapi-281232387Pas encore d'évaluation

- Joint Audit Programme For EEA GMP InspectoratesDocument11 pagesJoint Audit Programme For EEA GMP InspectoratesPiyush AroraPas encore d'évaluation

- Cost and Management Accounting - Course OutlineDocument9 pagesCost and Management Accounting - Course OutlineJajJay100% (1)

- Financial Statement AnalysisDocument58 pagesFinancial Statement AnalysisSabrina Reja MithilaPas encore d'évaluation

- Audit Engagement Strategy (Driving Audit Value, Vol. III): The Best Practice Strategy Guide for Maximising the Added Value of the Internal Audit EngagementsD'EverandAudit Engagement Strategy (Driving Audit Value, Vol. III): The Best Practice Strategy Guide for Maximising the Added Value of the Internal Audit EngagementsPas encore d'évaluation

- Benchmarking Business Incubators Main ReportDocument47 pagesBenchmarking Business Incubators Main ReportNaveen Kumar Poddar100% (1)

- Icwai Inter p10Document504 pagesIcwai Inter p10manreader100% (2)

- ACCT3014 Lecture01 s12013Document40 pagesACCT3014 Lecture01 s12013thomashong313Pas encore d'évaluation

- Module1 Managing GPP ImplementationDocument45 pagesModule1 Managing GPP ImplementationAria Imam AmbaraPas encore d'évaluation

- CA Inter Cost & Management Accounting Theory Book by CA Purushottam AggarwalDocument125 pagesCA Inter Cost & Management Accounting Theory Book by CA Purushottam Aggarwalabhinesh243Pas encore d'évaluation

- 4 Meth For C1BA PreparationDocument25 pages4 Meth For C1BA Preparationkopalko77Pas encore d'évaluation

- Modification PRAG 2012Document17 pagesModification PRAG 2012Marija ErgicPas encore d'évaluation

- Green Book Guidance Public Sector Business Cases 2015 UpdateDocument152 pagesGreen Book Guidance Public Sector Business Cases 2015 UpdateHilda IsfanoviPas encore d'évaluation

- Iso 17024 2012 PowerpointDocument38 pagesIso 17024 2012 Powerpointdaiweing67% (3)

- MBA Cost RecordsDocument8 pagesMBA Cost RecordsGurneet KaurPas encore d'évaluation

- Public Procurement DG Regional Policy Claude TournierDocument13 pagesPublic Procurement DG Regional Policy Claude TournierliviutfyPas encore d'évaluation

- Hans ZepicDocument13 pagesHans ZepicCamelia CamiPas encore d'évaluation

- Cost AuditDocument15 pagesCost AuditseesawupndownPas encore d'évaluation

- FRC Snapshot Introduction - August 2022 1Document13 pagesFRC Snapshot Introduction - August 2022 1sherif elashmawyPas encore d'évaluation

- Benefits Realisation Guide - Feb 2013Document20 pagesBenefits Realisation Guide - Feb 2013Dave CPas encore d'évaluation

- Audit Risk Alert: Employee Benefit Plans Industry Developments, 2018D'EverandAudit Risk Alert: Employee Benefit Plans Industry Developments, 2018Pas encore d'évaluation

- Guidelines On Pre AuditDocument65 pagesGuidelines On Pre AuditPeter Jhun Flores100% (1)

- Green Book Guidance On Public Sector Business Cases Using The Five Case Model 2013 UpdateDocument152 pagesGreen Book Guidance On Public Sector Business Cases Using The Five Case Model 2013 UpdateAjit SaiPas encore d'évaluation

- Excipact PresentationDocument25 pagesExcipact PresentationVaishali Kurdikar0% (1)

- ITTO - Memorizing Inputs Tools and OutputsDocument6 pagesITTO - Memorizing Inputs Tools and OutputslahyouhPas encore d'évaluation

- Cost 1Document21 pagesCost 1Victor VarghesePas encore d'évaluation

- Audit Risk Alert: Government Auditing Standards and Single Audit Developments: Strengthening Audit Integrity 2018/19D'EverandAudit Risk Alert: Government Auditing Standards and Single Audit Developments: Strengthening Audit Integrity 2018/19Pas encore d'évaluation

- ACCA Advanced Corporate Reporting 2005Document763 pagesACCA Advanced Corporate Reporting 2005Platonic100% (2)

- The Federal Budget 2014 2015 Impacts Risks Tools and Changes With Commission of Audit and Henry ReviewDocument10 pagesThe Federal Budget 2014 2015 Impacts Risks Tools and Changes With Commission of Audit and Henry ReviewfwrgroupPas encore d'évaluation

- Financial Management Series Number 8: Performance Measurement & Performance Based Budgeting (PBB)Document95 pagesFinancial Management Series Number 8: Performance Measurement & Performance Based Budgeting (PBB)laddooparmarPas encore d'évaluation

- CD 07 A Internal ControlDocument8 pagesCD 07 A Internal ControlAlexandru VasilePas encore d'évaluation

- Workshop: Cost and Pricing Analysis: Analyzing The NumbersDocument8 pagesWorkshop: Cost and Pricing Analysis: Analyzing The NumbersJowjie TVPas encore d'évaluation

- 1137 Dohoda o Certifikaci Rev 4 enDocument8 pages1137 Dohoda o Certifikaci Rev 4 enAriel AlcantaraPas encore d'évaluation

- ACCT3014 Lecture14 s12013Document35 pagesACCT3014 Lecture14 s12013thomashong313Pas encore d'évaluation

- IATF Auditor Guide First Ed April 2009 Final PDFDocument32 pagesIATF Auditor Guide First Ed April 2009 Final PDFkarthikkanda100% (7)

- FM8PBBDocument95 pagesFM8PBBsamuel hailuPas encore d'évaluation

- Guidance Notes For Ceng Candidates 67285Document75 pagesGuidance Notes For Ceng Candidates 67285johnbullasPas encore d'évaluation

- Guidance On Joint Action Plans: European CommissionDocument14 pagesGuidance On Joint Action Plans: European CommissionMarcello D'AmicoPas encore d'évaluation

- TAXNZ Module Outlinev04Document5 pagesTAXNZ Module Outlinev04spatel1972Pas encore d'évaluation

- Cost Accounting TheoryDocument77 pagesCost Accounting TheoryLakshmi811Pas encore d'évaluation

- Audits and Controls in Horizon 2020Document10 pagesAudits and Controls in Horizon 2020Angel LagrañaPas encore d'évaluation

- Vacancy Notice It Operations & Infrastructure Manager (F/M) REF.: ESMA/2014/VAC24/AD7Document7 pagesVacancy Notice It Operations & Infrastructure Manager (F/M) REF.: ESMA/2014/VAC24/AD7Prashant PrajapatiPas encore d'évaluation

- Fin218 CSG CompilationDocument508 pagesFin218 CSG CompilationMartin GilarPas encore d'évaluation

- Ifrs For Smes Fact Sheet: ContentDocument6 pagesIfrs For Smes Fact Sheet: ContentMary Jane O ApelladoPas encore d'évaluation

- Tax Management and Practice in IndiaDocument1 272 pagesTax Management and Practice in IndiaCalmguy Chaitu100% (1)

- 06 Regulation of The Public Accounting PracticeDocument6 pages06 Regulation of The Public Accounting PracticeJane DizonPas encore d'évaluation

- IocDocument2 pagesIocamits609Pas encore d'évaluation

- PFM Reform in Nepal: Towards Better Financial GovernanceDocument74 pagesPFM Reform in Nepal: Towards Better Financial GovernanceInternational Consortium on Governmental Financial ManagementPas encore d'évaluation

- Research On Comprehensive IncomeDocument22 pagesResearch On Comprehensive IncomeAya SafwatPas encore d'évaluation

- Dipifrs AccaDocument11 pagesDipifrs AccaDeepak Thakkar100% (1)

- 2015 BPP P7 Passcards PDFDocument161 pages2015 BPP P7 Passcards PDFZain Mohiuddin100% (1)

- A Parents Guide To Mini TennispdfDocument20 pagesA Parents Guide To Mini TennispdfDragan VuckovicPas encore d'évaluation

- 2 MW Product BrochurepdfDocument16 pages2 MW Product BrochurepdfDragan VuckovicPas encore d'évaluation

- TS KoncarDocument4 pagesTS KoncarDragan VuckovicPas encore d'évaluation

- Factsheet Industrial ParticipationDocument4 pagesFactsheet Industrial ParticipationDragan VuckovicPas encore d'évaluation

- How To Obtain A PIC NumberDocument2 pagesHow To Obtain A PIC NumberDragan Vuckovic100% (1)

- 16 AbbreviationsDocument4 pages16 AbbreviationsDragan VuckovicPas encore d'évaluation

- Preparation of Manuscript For A CIE Meeting Proceedings: 1.2 Photo-Offset PrintingDocument2 pagesPreparation of Manuscript For A CIE Meeting Proceedings: 1.2 Photo-Offset PrintingDragan VuckovicPas encore d'évaluation

- Progress Monitoring and Ex-Post Evaluation: Performance Record That Will Be Kept For Each BeneficiaryDocument2 pagesProgress Monitoring and Ex-Post Evaluation: Performance Record That Will Be Kept For Each BeneficiaryDragan VuckovicPas encore d'évaluation

- Architectural LTG Fundamentals Update 12april2010Document1 pageArchitectural LTG Fundamentals Update 12april2010Dragan VuckovicPas encore d'évaluation

- Annex D I-Legal Entity Sheet-Private CompaniesDocument1 pageAnnex D I-Legal Entity Sheet-Private CompaniesDragan VuckovicPas encore d'évaluation

- Grant Facility 2005: Pre-Notice of Call For ProposalsDocument1 pageGrant Facility 2005: Pre-Notice of Call For ProposalsDragan VuckovicPas encore d'évaluation

- Philips Pole GuideDocument36 pagesPhilips Pole GuideDragan VuckovicPas encore d'évaluation

- Secure Clean and Efficient Energy Draft Work ProgrammeDocument138 pagesSecure Clean and Efficient Energy Draft Work ProgrammeDragan VuckovicPas encore d'évaluation

- CoreLine LED Brochure 2013Document20 pagesCoreLine LED Brochure 2013Dragan VuckovicPas encore d'évaluation

- AT&T COMMUNICATIONS SERVICES PHILIPPINES, INC. v. COMMISSION ON INTERNAL REVENUEDocument2 pagesAT&T COMMUNICATIONS SERVICES PHILIPPINES, INC. v. COMMISSION ON INTERNAL REVENUESSPas encore d'évaluation

- CS2306668Document1 pageCS2306668MusaPas encore d'évaluation

- PPM FunctionalitiesDocument58 pagesPPM FunctionalitiesBenbase Salim AbdelkhaderPas encore d'évaluation

- Mapping A Customers EDI Field in and Out of SAPDocument7 pagesMapping A Customers EDI Field in and Out of SAPSOUMEN DASPas encore d'évaluation

- Information TechnologyDocument43 pagesInformation TechnologyAlexis TradioPas encore d'évaluation

- TPST 5050854611 1Document3 pagesTPST 5050854611 1ianrossbPas encore d'évaluation

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Gadde Niharika ChowdaryPas encore d'évaluation

- Tax Invoice: Shop No. SH-4, Ground Floor, Springfield Avenue, Tolcai Zari, Margao, Salcete - GoaDocument1 pageTax Invoice: Shop No. SH-4, Ground Floor, Springfield Avenue, Tolcai Zari, Margao, Salcete - GoaSakshi ComputersPas encore d'évaluation

- Ais - Chapter 15 Rea ModelDocument138 pagesAis - Chapter 15 Rea Modelariel0429100% (2)

- Online Appointment SystemDocument5 pagesOnline Appointment SystemJefferson De Vera100% (1)

- Bank Release OrderDocument2 pagesBank Release Ordercallvk50% (2)

- FabHotels PI V3oqu 2324 01437 Invoice CEBXJDDocument1 pageFabHotels PI V3oqu 2324 01437 Invoice CEBXJDPamily Adhikary0% (1)

- Dispute ManagementDocument33 pagesDispute ManagementKarina Nunes100% (2)

- Time of Supply of GoodsDocument5 pagesTime of Supply of GoodsSuman AnandPas encore d'évaluation

- Cookbook Payment Scheme eDocument58 pagesCookbook Payment Scheme ebhaskar_tripath67% (3)

- LC DocumentDocument5 pagesLC DocumentmaykPas encore d'évaluation

- LE Shipment Cost ConfigurationDocument44 pagesLE Shipment Cost ConfigurationAziz100% (10)

- Afs Event: Value Proposition & Proposed SolutionDocument47 pagesAfs Event: Value Proposition & Proposed SolutionSuryanarayana TataPas encore d'évaluation

- Freelancer Startup GuideDocument15 pagesFreelancer Startup GuideveravsyrPas encore d'évaluation

- 07002379Document2 pages07002379api-3701571Pas encore d'évaluation

- Shopify - Sa FormDocument6 pagesShopify - Sa FormSujathaKsPas encore d'évaluation

- Ril PVC Price DT.01.02.2019Document13 pagesRil PVC Price DT.01.02.2019Akshat JainPas encore d'évaluation

- FakeDocument1 pageFakeAbdulMananPas encore d'évaluation

- Igcrd 2022Document13 pagesIgcrd 2022Abhijyo SinghPas encore d'évaluation

- 1311692Document1 page1311692Alexander VasquezPas encore d'évaluation

- SAP R/3 Consultant Cin - TaxinjDocument25 pagesSAP R/3 Consultant Cin - TaxinjphanikumaraPas encore d'évaluation

- G.Naga Chandra Sekhar Mobile: 07760460489: Project # 1: SAP R/3 SupportDocument4 pagesG.Naga Chandra Sekhar Mobile: 07760460489: Project # 1: SAP R/3 SupportYashwant KumarPas encore d'évaluation

- UAE VAT Dual Currency Invoice Template 1Document4 pagesUAE VAT Dual Currency Invoice Template 1Vijay Kumar Reddy ChallaPas encore d'évaluation

- Computerized Accounting Unit - 5Document36 pagesComputerized Accounting Unit - 5thamizt100% (2)

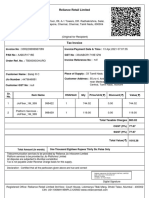

- Reliance Retail Limited: Total Amount (In Words) One Thousand Eighteen Rupees Thirty Six Paisa OnlyDocument3 pagesReliance Retail Limited: Total Amount (In Words) One Thousand Eighteen Rupees Thirty Six Paisa OnlyBalaPas encore d'évaluation