Vous aimerez peut-être aussi

- Wedding Emcee ScriptDocument6 pagesWedding Emcee ScriptTristan Michael RyanPas encore d'évaluation

- Wedding ItineraryDocument3 pagesWedding ItineraryTristan Michael RyanPas encore d'évaluation

- Readiness Potential Is The Key To Free WillDocument7 pagesReadiness Potential Is The Key To Free WillTristan Michael RyanPas encore d'évaluation

- How To Set Up The LightsDocument2 pagesHow To Set Up The LightsTristan Michael RyanPas encore d'évaluation

- End of Year Self-ReflectionDocument2 pagesEnd of Year Self-ReflectionTristan Michael RyanPas encore d'évaluation

- St. Augustine EssayDocument5 pagesSt. Augustine EssayTristan Michael RyanPas encore d'évaluation

- A Short Summary of Calvin's Institutes - by Dr. C. Matthew McMahon - A Puritan's Mind PDFDocument3 pagesA Short Summary of Calvin's Institutes - by Dr. C. Matthew McMahon - A Puritan's Mind PDFTristan Michael RyanPas encore d'évaluation

- Public Finance and Public Policy - Gruber Chapter 2Document2 pagesPublic Finance and Public Policy - Gruber Chapter 2Tristan Michael RyanPas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- ReSA B42 TAX First PB Exam - Questions, Answers - SolutionsDocument18 pagesReSA B42 TAX First PB Exam - Questions, Answers - SolutionsPearl Mae De VeasPas encore d'évaluation

- VP NG9XKB5Z InvoicesDocument2 pagesVP NG9XKB5Z InvoicesKhushin LakharaPas encore d'évaluation

- Deacc506 23241 2Document2 pagesDeacc506 23241 2Sants ShadyPas encore d'évaluation

- Oct PayslipDocument3 pagesOct PayslipRajanala Vignesh NaiduPas encore d'évaluation

- CFI Advanced Excel Formulas & Functions - BlankDocument6 pagesCFI Advanced Excel Formulas & Functions - BlankNew Era Games80% (5)

- Itr-1 Sahaj Individual Income Tax Return: Acknowledgement Number: 856116270220718 Assessment Year: 2018-19Document5 pagesItr-1 Sahaj Individual Income Tax Return: Acknowledgement Number: 856116270220718 Assessment Year: 2018-19sky2flyboy@gmail.comPas encore d'évaluation

- PwcSalesInvoiceReport DesignJCDocument2 pagesPwcSalesInvoiceReport DesignJCCHOTIPas encore d'évaluation

- Final AnalyticsDocument10 pagesFinal AnalyticsAries BautistaPas encore d'évaluation

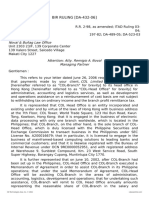

- 2006 BIR - Ruling - DA 432 06 - 20210505 13 1t6tcx6Document3 pages2006 BIR - Ruling - DA 432 06 - 20210505 13 1t6tcx6Boss NikPas encore d'évaluation

- Table A: Product ComparisonDocument4 pagesTable A: Product ComparisonSeemaPas encore d'évaluation

- FabHotels BTGKV 2324 00287 Invoice ZRPFLQDocument2 pagesFabHotels BTGKV 2324 00287 Invoice ZRPFLQMohanGuptaPas encore d'évaluation

- New Jersey Tax Guide: Buying or Selling A Home in New JerseyDocument9 pagesNew Jersey Tax Guide: Buying or Selling A Home in New Jerseynour abdallaPas encore d'évaluation

- Employees Payroll 5Document28 pagesEmployees Payroll 5ArthurLeonard MalijanPas encore d'évaluation

- Salary Slip MainDocument1 pageSalary Slip MainVineetBaliyan100% (1)

- Adobe Scan 01042021 - CompressedDocument6 pagesAdobe Scan 01042021 - CompressedKartik ShuklaPas encore d'évaluation

- HDFC Life YoungStar Super Premium (SPL) IllustrationDocument0 pageHDFC Life YoungStar Super Premium (SPL) IllustrationAnkur MittalPas encore d'évaluation

- Tax SecretsDocument16 pagesTax SecretsVenkat SairamPas encore d'évaluation

- How Much Is The Distributable Income of The GPP?Document2 pagesHow Much Is The Distributable Income of The GPP?Katrina Dela CruzPas encore d'évaluation

- Withholding Compensation - 1601Cv2018 FormDocument1 pageWithholding Compensation - 1601Cv2018 FormReynaldo PogzPas encore d'évaluation

- Chapter11Document33 pagesChapter11Zai AriyPas encore d'évaluation

- Sor - WRD Gob - 01 - 10 - 12Document383 pagesSor - WRD Gob - 01 - 10 - 12Abhishek sPas encore d'évaluation

- Canons of Taxation: Income Tax LawsDocument13 pagesCanons of Taxation: Income Tax LawsHaris MughalPas encore d'évaluation

- Math 11 ABM Business Math Q2 Week 3Document18 pagesMath 11 ABM Business Math Q2 Week 3Flordilyn DichonPas encore d'évaluation

- Lease Agreement Between COC and CODDocument5 pagesLease Agreement Between COC and CODAntonieto BPas encore d'évaluation

- Tax Invoice: Product Description Qty Gross A Mount Discount Taxable V Alue Igst TotalDocument2 pagesTax Invoice: Product Description Qty Gross A Mount Discount Taxable V Alue Igst TotalRaju Kumar SoniPas encore d'évaluation

- Investment Declaration For Income Tax Calculation For The Financial Year 2023-24Document2 pagesInvestment Declaration For Income Tax Calculation For The Financial Year 2023-24Bheemineni ChandrikaPas encore d'évaluation

- Pioma Plastics Company Cash Flow Statement For The Year Ended July 31 Amount in Rs. Amount in Rs. Cash Flow From Operating ActivitiesDocument4 pagesPioma Plastics Company Cash Flow Statement For The Year Ended July 31 Amount in Rs. Amount in Rs. Cash Flow From Operating ActivitiesPrajwal PaiPas encore d'évaluation

- TEST PAPER-1 House PropertyDocument2 pagesTEST PAPER-1 House PropertyBharatbhusan RoutPas encore d'évaluation

- Donor S Tax. CPA REVIEWER. TABAG PDFDocument19 pagesDonor S Tax. CPA REVIEWER. TABAG PDFHansPas encore d'évaluation

- BillDocument3 pagesBillnahlaPas encore d'évaluation