Vous aimerez peut-être aussi

- Cost Accounting Normal Job Costing: Presented By: Umut Korkuter & Sina BakhshalianDocument35 pagesCost Accounting Normal Job Costing: Presented By: Umut Korkuter & Sina BakhshalianBurakhan YanıkPas encore d'évaluation

- S2 CMA c03 Job CostingDocument13 pagesS2 CMA c03 Job Costingdiasjoy67Pas encore d'évaluation

- Cost12ism 04Document42 pagesCost12ism 04d.pagkatoytoyPas encore d'évaluation

- Cost Accounting 15th Edition Horngren Solutions Manual 1Document36 pagesCost Accounting 15th Edition Horngren Solutions Manual 1maryreynoldsxdbtqcfaje100% (22)

- ABC and Cost Management ToolsDocument132 pagesABC and Cost Management ToolsAmanda BarkerPas encore d'évaluation

- Cost Accounting - 2021 - Part 2 - LVL L3Document89 pagesCost Accounting - 2021 - Part 2 - LVL L3Poupeau AnthonyPas encore d'évaluation

- Job Batch Costing GuideDocument21 pagesJob Batch Costing GuidesamiPas encore d'évaluation

- ACC 2242 Chapter 5 In-Class QuestionsDocument7 pagesACC 2242 Chapter 5 In-Class QuestionsSalman I SadibPas encore d'évaluation

- ManaktugasDocument7 pagesManaktugasNimas KartikaPas encore d'évaluation

- Answers Homework # 15 Cost MGMT 4Document7 pagesAnswers Homework # 15 Cost MGMT 4Raman APas encore d'évaluation

- ACCT 3125 Chapter 5 SolutionsDocument7 pagesACCT 3125 Chapter 5 SolutionskayPas encore d'évaluation

- Cornerstones of Managerial Accounting Canadian 2nd Edition Mowen Solutions Manual 1Document36 pagesCornerstones of Managerial Accounting Canadian 2nd Edition Mowen Solutions Manual 1dawnlarsentsgiwnqczm100% (25)

- Cornerstones of Managerial Accounting Canadian 2Nd Edition Mowen Solutions Manual Full Chapter PDFDocument36 pagesCornerstones of Managerial Accounting Canadian 2Nd Edition Mowen Solutions Manual Full Chapter PDFrenee.crawford887100% (7)

- Process Costing: Questions For Writing and DiscussionDocument49 pagesProcess Costing: Questions For Writing and DiscussionKhoirul MubinPas encore d'évaluation

- Cornerstones of Managerial Accounting Canadian 2nd Edition Mowen Solutions Manual 1Document54 pagesCornerstones of Managerial Accounting Canadian 2nd Edition Mowen Solutions Manual 1kenneth100% (40)

- Lecture 9 ABC, CVP PDFDocument58 pagesLecture 9 ABC, CVP PDFShweta SridharPas encore d'évaluation

- Solution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 4Document34 pagesSolution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 4jasperkennedy092% (37)

- Management AccountingDocument33 pagesManagement AccountingjazzmahbubPas encore d'évaluation

- CH 4Document72 pagesCH 4Chang Chan ChongPas encore d'évaluation

- ABC Hansen & Mowen ch4 P ('t':'3', 'I':'669594619') D '' Var B Location Settimeout (Function ( If (Typeof Window - Iframe 'Undefined') ( B.href B.href ) ), 15000)Document22 pagesABC Hansen & Mowen ch4 P ('t':'3', 'I':'669594619') D '' Var B Location Settimeout (Function ( If (Typeof Window - Iframe 'Undefined') ( B.href B.href ) ), 15000)Aziza AmranPas encore d'évaluation

- Asiment SolutionDocument4 pagesAsiment Solutionmansoor1307100% (1)

- Chapter 3 Job Order CostingDocument33 pagesChapter 3 Job Order CostingFatimaIjazPas encore d'évaluation

- Job Costing at Law Firm and University PressDocument22 pagesJob Costing at Law Firm and University PressAlmirPas encore d'évaluation

- Absorption of OverheadDocument22 pagesAbsorption of OverheadSamuel DwumfourPas encore d'évaluation

- 230 Chapter 3 - Overhead BulldogDocument28 pages230 Chapter 3 - Overhead BulldogSarath Mohan K SPas encore d'évaluation

- Strategic Cost Accounting: MBA-First YearDocument99 pagesStrategic Cost Accounting: MBA-First YearNada YoussefPas encore d'évaluation

- Process Costing Weighted Average Method for Picture Frame Assembly DepartmentDocument3 pagesProcess Costing Weighted Average Method for Picture Frame Assembly DepartmentRudy Setiawan KamadjajaPas encore d'évaluation

- Activity Based CostingDocument20 pagesActivity Based CostingArpit SahaiPas encore d'évaluation

- Systems Design: Job-Order CostingDocument46 pagesSystems Design: Job-Order CostingRafay Salman MazharPas encore d'évaluation

- Activity Based CostingDocument52 pagesActivity Based CostingraviktatiPas encore d'évaluation

- SMC W4 Cost R2Document12 pagesSMC W4 Cost R2Ronnie EnriquezPas encore d'évaluation

- Activity Based CostingDocument40 pagesActivity Based CostingHaseeb JavedPas encore d'évaluation

- ACCG200 Lectures 2-11 HandoutDocument108 pagesACCG200 Lectures 2-11 HandoutNikita Singh DhamiPas encore d'évaluation

- Standard Costing and Basic VariancesDocument9 pagesStandard Costing and Basic Variancesbrian bolloPas encore d'évaluation

- SCM Sol 05 14Document14 pagesSCM Sol 05 14bloomshing0% (1)

- Cost-Chapter 4 NewDocument18 pagesCost-Chapter 4 NewYonas AyelePas encore d'évaluation

- Ch.2 - Job CostingDocument26 pagesCh.2 - Job Costingahmedgalalabdalbaath2003Pas encore d'évaluation

- Analyze Cost Allocation Methods and Overhead VariancesDocument73 pagesAnalyze Cost Allocation Methods and Overhead VariancesPiyal Hossain100% (1)

- CMA Part 1 Sec CDocument131 pagesCMA Part 1 Sec CMusthaqMohammedMadathilPas encore d'évaluation

- ACCT505 Week 2 Quiz 1 Job Order and Process Costing SystemsDocument8 pagesACCT505 Week 2 Quiz 1 Job Order and Process Costing SystemsNatasha DeclanPas encore d'évaluation

- COST ALLOCATION and ACTIVITY-BASED COSTINGDocument5 pagesCOST ALLOCATION and ACTIVITY-BASED COSTINGBeverly Claire Lescano-MacagalingPas encore d'évaluation

- Study Unit 3: COST Allocation Techniques Overhead Normal CostingDocument29 pagesStudy Unit 3: COST Allocation Techniques Overhead Normal CostingPauline Keith Paz ManuelPas encore d'évaluation

- Group 6 PPT CaseDocument33 pagesGroup 6 PPT CaseRavNeet KaUr100% (1)

- Chapter 2 Activity Based Costing: 1. ObjectivesDocument13 pagesChapter 2 Activity Based Costing: 1. ObjectivesNilda CorpuzPas encore d'évaluation

- Accounting For Factory OverheadDocument27 pagesAccounting For Factory Overheadspectrum_480% (1)

- F5 RM March 2016 AnswersDocument15 pagesF5 RM March 2016 AnswersPrincezPinkyPas encore d'évaluation

- UEU Akuntansi Biaya Pertemuan 8910Document84 pagesUEU Akuntansi Biaya Pertemuan 8910hardyputra46Pas encore d'évaluation

- Longman F21 (Key)Document18 pagesLongman F21 (Key)Yan Pak KiuPas encore d'évaluation

- MAHM6e Ch04.Ab - AzDocument49 pagesMAHM6e Ch04.Ab - Azlita2703Pas encore d'évaluation

- COST & MANAGERIAL ACCOUNTINGDocument20 pagesCOST & MANAGERIAL ACCOUNTINGAthar KhanPas encore d'évaluation

- Cost Terminology and Cost FlowsDocument60 pagesCost Terminology and Cost FlowsInney SildalatifaPas encore d'évaluation

- Product CostingDocument16 pagesProduct CostingAyush100% (1)

- PROCESS COSTING METHODS AND CALCULATIONSDocument76 pagesPROCESS COSTING METHODS AND CALCULATIONSAnggrainiPas encore d'évaluation

- Cost Accounting A Managerial Emphasis Canadian 7th Edition Horngren Solutions Manual 1Document36 pagesCost Accounting A Managerial Emphasis Canadian 7th Edition Horngren Solutions Manual 1maryreynoldsxdbtqcfaje100% (22)

- Lecture 6 - ABC Costing RevisedDocument22 pagesLecture 6 - ABC Costing RevisedMJ jPas encore d'évaluation

- Cost Management: A Case for Business Process Re-engineeringD'EverandCost Management: A Case for Business Process Re-engineeringPas encore d'évaluation

- A to Z Cost Accounting Dictionary: A Practical Approach - Theory to CalculationD'EverandA to Z Cost Accounting Dictionary: A Practical Approach - Theory to CalculationPas encore d'évaluation

- 1-4 Deductions FlowchartDocument2 pages1-4 Deductions Flowchartoddsey0713Pas encore d'évaluation

- 3 5 PartnershipsDocument1 page3 5 Partnershipsoddsey0713Pas encore d'évaluation

- 1-8 GST - GST Payable or ITC AvalDocument2 pages1-8 GST - GST Payable or ITC Avaloddsey0713Pas encore d'évaluation

- 1-5 Trading StockDocument1 page1-5 Trading Stockoddsey0713Pas encore d'évaluation

- Does FBT Apply?: Div 13 ExclusionsDocument1 pageDoes FBT Apply?: Div 13 Exclusionsoddsey0713Pas encore d'évaluation

- 4-3 Part IVA General AntiAvoidanceDocument1 page4-3 Part IVA General AntiAvoidanceoddsey0713Pas encore d'évaluation

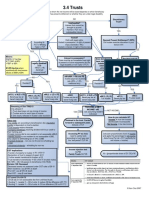

- 3-4 TrustsDocument1 page3-4 Trustsoddsey0713Pas encore d'évaluation

- 1-3 Assessable IncomeDocument2 pages1-3 Assessable Incomeoddsey0713Pas encore d'évaluation

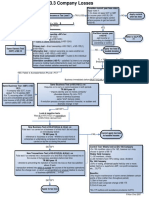

- 3-3 Company LossesDocument1 page3-3 Company Lossesoddsey0713Pas encore d'évaluation

- 2-4,5 Capital WorksDocument1 page2-4,5 Capital Worksoddsey0713Pas encore d'évaluation

- 2-3 Capital AllowancesDocument1 page2-3 Capital Allowancesoddsey0713Pas encore d'évaluation

- Restrictions on franking creditsDocument1 pageRestrictions on franking creditsoddsey0713Pas encore d'évaluation

- T7 Chapter 6 Solutions To The Essential ActivitiesDocument26 pagesT7 Chapter 6 Solutions To The Essential Activitiesoddsey0713Pas encore d'évaluation

- Executing-The-Creative Design Elements and Layout Styles With ADS As ExamplesDocument47 pagesExecuting-The-Creative Design Elements and Layout Styles With ADS As Examplesoddsey0713Pas encore d'évaluation

- Creating Effective Ads PPT 4 MGMTDocument22 pagesCreating Effective Ads PPT 4 MGMToddsey0713Pas encore d'évaluation

- T5 Chapters 4 and 8 Solutions To The Essential ActivitiesDocument18 pagesT5 Chapters 4 and 8 Solutions To The Essential Activitiesoddsey0713Pas encore d'évaluation

- 3-3 Div 7A Deemed Divs - VLDocument1 page3-3 Div 7A Deemed Divs - VLoddsey0713Pas encore d'évaluation

- Case Summaries 1 193Document54 pagesCase Summaries 1 193oddsey0713100% (1)

- T8 Chapters 9 and 7 Solutions To The Essential ActivitiesDocument12 pagesT8 Chapters 9 and 7 Solutions To The Essential Activitiesoddsey0713Pas encore d'évaluation

- 2006 Planning EvalDocument33 pages2006 Planning EvalSanjay SahooPas encore d'évaluation

- MOD 03 Appendix ABC Case Classic Pen (2023)Document22 pagesMOD 03 Appendix ABC Case Classic Pen (2023)georgiana.ioannouPas encore d'évaluation

- Adobe Scan 14 May 2022Document5 pagesAdobe Scan 14 May 2022Mary CharlesPas encore d'évaluation

- Self Practice Cost AccountingDocument17 pagesSelf Practice Cost AccountingLara Alyssa GarboPas encore d'évaluation

- Process Costing Chapter PDFDocument50 pagesProcess Costing Chapter PDFTasfiPas encore d'évaluation

- Detailed Unit Price Analysis for Clearing & Grubbing WorksDocument220 pagesDetailed Unit Price Analysis for Clearing & Grubbing WorksDennis Sagao100% (11)

- Project Semester Report: Business Development & Detailed Design of Bogie Repair Shed, New Bongaigaon, AssamDocument121 pagesProject Semester Report: Business Development & Detailed Design of Bogie Repair Shed, New Bongaigaon, AssamJaneesh Pal SinghPas encore d'évaluation

- Cost Accounting Questions and Their AnswersDocument5 pagesCost Accounting Questions and Their Answerszulqarnainhaider450_Pas encore d'évaluation

- Recruitment Rules for West Bengal Audit ServiceDocument11 pagesRecruitment Rules for West Bengal Audit ServiceCMA GuysPas encore d'évaluation

- Job Order and Process CostingDocument13 pagesJob Order and Process CostingAnuar LoboPas encore d'évaluation

- Tapal 2Document32 pagesTapal 2Javed Dawoodani0% (1)

- Tutorial Collection 3Document1 pageTutorial Collection 3Arti SinghPas encore d'évaluation

- Wa0001 PDFDocument298 pagesWa0001 PDFZohair HumayunPas encore d'évaluation

- Mock Exam MG T Acct 2022Document2 pagesMock Exam MG T Acct 2022Bình AnPas encore d'évaluation

- Audit of Asingan Corporation Financial StatementsDocument4 pagesAudit of Asingan Corporation Financial StatementsKizzea Bianca GadotPas encore d'évaluation

- Tutorial 4 - Costing For OverheadDocument5 pagesTutorial 4 - Costing For OverheadMuhammad Alif100% (1)

- Job order costing cycle explainedDocument20 pagesJob order costing cycle explainedAlysa JanePas encore d'évaluation

- Cost Accounting Systems A. Traditional Cost Accounting TheoriesDocument47 pagesCost Accounting Systems A. Traditional Cost Accounting TheoriesalabwalaPas encore d'évaluation

- Chapter 5 - Solutions To Cost Accounting Book (Raiborn and Kinney, 2 Phil Edition)Document22 pagesChapter 5 - Solutions To Cost Accounting Book (Raiborn and Kinney, 2 Phil Edition)Mark Johnrei GandiaPas encore d'évaluation

- 4 Learning CurvesDocument8 pages4 Learning Curvessabinaeghan1Pas encore d'évaluation

- Form 3 Adjudicator's Determination: ClaimantDocument7 pagesForm 3 Adjudicator's Determination: ClaimantSuresh GovindarajPas encore d'évaluation

- Accounting Graded AssignmentsDocument19 pagesAccounting Graded AssignmentsAnnela EasyPas encore d'évaluation

- 102.01 Introduction To Cost Accounting - by MD - Monowar Hossain, FCMA, CPA, FCS, ACADocument12 pages102.01 Introduction To Cost Accounting - by MD - Monowar Hossain, FCMA, CPA, FCS, ACAMridul KarmakarPas encore d'évaluation

- Bachelor of Accounting ACC731 Cost & Management Accounting 1Document39 pagesBachelor of Accounting ACC731 Cost & Management Accounting 1Gideon SancyPas encore d'évaluation

- Performance Evaluation Using Variances From Standard CostsDocument41 pagesPerformance Evaluation Using Variances From Standard Costswarsima100% (1)

- Senior Auditor Cost-Accounting-McqsDocument101 pagesSenior Auditor Cost-Accounting-McqsMuhammad HamidPas encore d'évaluation

- Alaska Dor - Oil & Gas Annual Cost History Report V 1.20110812Document3 pagesAlaska Dor - Oil & Gas Annual Cost History Report V 1.20110812Amit KumarPas encore d'évaluation

- Private Prisons in The United States: Executive SummaryDocument6 pagesPrivate Prisons in The United States: Executive SummaryLee GaylordPas encore d'évaluation

- Process Accounts: Normal/Abnormal Loss/Gain: Problems and SolutionsDocument16 pagesProcess Accounts: Normal/Abnormal Loss/Gain: Problems and Solutionspuneet jainPas encore d'évaluation

- AA025 PYQ 2015 - 2014 (ANS) by SectionDocument4 pagesAA025 PYQ 2015 - 2014 (ANS) by Sectionnurauniatiqah49Pas encore d'évaluation

- Intermediate Accounting I - Ppe AnswersDocument3 pagesIntermediate Accounting I - Ppe AnswersJoovs Joovho50% (2)