Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- 1-4 Deductions FlowchartDocument2 pages1-4 Deductions Flowchartoddsey0713Pas encore d'évaluation

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- 1-8 GST - GST Payable or ITC AvalDocument2 pages1-8 GST - GST Payable or ITC Avaloddsey0713Pas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- 3 5 PartnershipsDocument1 page3 5 Partnershipsoddsey0713Pas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (894)

- 2-3 Capital AllowancesDocument1 page2-3 Capital Allowancesoddsey0713Pas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

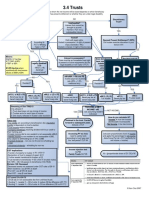

- 3-4 TrustsDocument1 page3-4 Trustsoddsey0713Pas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- 4-3 Part IVA General AntiAvoidanceDocument1 page4-3 Part IVA General AntiAvoidanceoddsey0713Pas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Does FBT Apply?: Div 13 ExclusionsDocument1 pageDoes FBT Apply?: Div 13 Exclusionsoddsey0713Pas encore d'évaluation

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

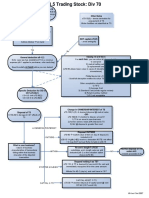

- 1-5 Trading StockDocument1 page1-5 Trading Stockoddsey0713Pas encore d'évaluation

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

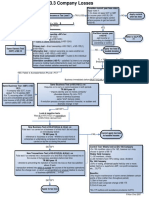

- 3-3 Company LossesDocument1 page3-3 Company Lossesoddsey0713Pas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- 1-3 Assessable IncomeDocument2 pages1-3 Assessable Incomeoddsey0713Pas encore d'évaluation

- 2-4,5 Capital WorksDocument1 page2-4,5 Capital Worksoddsey0713Pas encore d'évaluation

- Restrictions on franking creditsDocument1 pageRestrictions on franking creditsoddsey0713Pas encore d'évaluation

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Executing-The-Creative Design Elements and Layout Styles With ADS As ExamplesDocument47 pagesExecuting-The-Creative Design Elements and Layout Styles With ADS As Examplesoddsey0713Pas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- 3-3 Div 7A Deemed Divs - VLDocument1 page3-3 Div 7A Deemed Divs - VLoddsey0713Pas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Case Summaries 1 193Document54 pagesCase Summaries 1 193oddsey0713100% (1)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Creating Effective Ads PPT 4 MGMTDocument22 pagesCreating Effective Ads PPT 4 MGMToddsey0713Pas encore d'évaluation

- T7 Chapter 6 Solutions To The Essential ActivitiesDocument26 pagesT7 Chapter 6 Solutions To The Essential Activitiesoddsey0713Pas encore d'évaluation

- T6 Chapter 5 Solutions To The Essential ActivitiesDocument12 pagesT6 Chapter 5 Solutions To The Essential Activitiesoddsey0713Pas encore d'évaluation

- T8 Chapters 9 and 7 Solutions To The Essential ActivitiesDocument12 pagesT8 Chapters 9 and 7 Solutions To The Essential Activitiesoddsey0713Pas encore d'évaluation

- 2006 Planning EvalDocument33 pages2006 Planning EvalSanjay SahooPas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Agricultural Debt Waiver and Debt Relief SchemeDocument11 pagesAgricultural Debt Waiver and Debt Relief SchemehiteshvavaiyaPas encore d'évaluation

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- Project EvaluationDocument4 pagesProject EvaluationUkesh ShresthaPas encore d'évaluation

- 1.4 Planning and Structuring The Cost Audit 1.4.1 Need For Planning An AuditDocument5 pages1.4 Planning and Structuring The Cost Audit 1.4.1 Need For Planning An AuditAnu Yashpal KapoorPas encore d'évaluation

- 2013 Visayas Power Supply and Demand Situation: Republic of The Philippines Department of EnergyDocument10 pages2013 Visayas Power Supply and Demand Situation: Republic of The Philippines Department of EnergyJannet MalezaPas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Environmental Assessment Template Group MembersDocument4 pagesEnvironmental Assessment Template Group MembersPaula NguyenPas encore d'évaluation

- The Investment Function in Banking and Financial-Services ManagementDocument18 pagesThe Investment Function in Banking and Financial-Services ManagementHaris FadžanPas encore d'évaluation

- Topic 4 - Adjusting Accounts and Preparing Financial StatementsDocument18 pagesTopic 4 - Adjusting Accounts and Preparing Financial Statementsapi-388504348100% (1)

- CompleteDocument2 pagesCompleteappledeja7829Pas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- PepsiCo Shopping ListDocument1 pagePepsiCo Shopping ListPriyesh V RameshPas encore d'évaluation

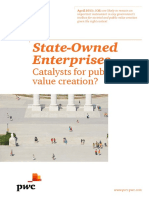

- PWC (2015) - 48 - State-Owned Enterprises - Catalysts For Public Value Creation (PEs SOEs) PDFDocument48 pagesPWC (2015) - 48 - State-Owned Enterprises - Catalysts For Public Value Creation (PEs SOEs) PDFAna Bandeira100% (1)

- Main Theories of FDIDocument22 pagesMain Theories of FDIThu TrangPas encore d'évaluation

- Afghan Rose Project - Some More DetailsDocument4 pagesAfghan Rose Project - Some More DetailsShrinkhala JainPas encore d'évaluation

- Chapter 4 Transportation and Assignment ModelsDocument88 pagesChapter 4 Transportation and Assignment ModelsSyaz Amri100% (1)

- Case of HyfluxDocument6 pagesCase of HyfluxMai NganPas encore d'évaluation

- Cluster Profile of Pickle of ShikarpurDocument7 pagesCluster Profile of Pickle of ShikarpurZohaib Ali MemonPas encore d'évaluation

- Irfz 24 NDocument9 pagesIrfz 24 Njmbernal7487886Pas encore d'évaluation

- Hygienic Chappathi Business Loan ReportDocument13 pagesHygienic Chappathi Business Loan ReportJose PiusPas encore d'évaluation

- Idea Bridge - 100 Success Plan For Crisis Recovery & New CeoDocument6 pagesIdea Bridge - 100 Success Plan For Crisis Recovery & New CeoJairo H Pinzón CastroPas encore d'évaluation

- Supply Chain-Case Study of DellDocument3 pagesSupply Chain-Case Study of DellSafijo Alphons100% (1)

- How To Attack The Leader - FinalDocument14 pagesHow To Attack The Leader - Finalbalakk06Pas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- To Lease or Not To Lease?: Hotel ContractsDocument10 pagesTo Lease or Not To Lease?: Hotel ContractsDaryl ChengPas encore d'évaluation

- Class XII - Economics Government Budget and The EconomyDocument5 pagesClass XII - Economics Government Budget and The EconomyAayush GargPas encore d'évaluation

- Hygeia International: I. Title of The CaseDocument7 pagesHygeia International: I. Title of The CaseDan GabonPas encore d'évaluation

- Ch. 13 Leverage and Capital Structure AnswersDocument23 pagesCh. 13 Leverage and Capital Structure Answersbetl89% (27)

- DATABASEDocument8 pagesDATABASERusheet PadaliaPas encore d'évaluation

- Louis Vuitton in IndiaDocument16 pagesLouis Vuitton in IndiaFez Research LaboratoryPas encore d'évaluation

- Presentation On Attrition Rate of DeloitteDocument13 pagesPresentation On Attrition Rate of DeloitteRohit GuptaPas encore d'évaluation

- Cash Forecasting For ClassDocument24 pagesCash Forecasting For ClassShaikh Saifullah KhalidPas encore d'évaluation

- Financing Methods For Import of Capital Goods in IndiaDocument13 pagesFinancing Methods For Import of Capital Goods in IndiaAneesha KasimPas encore d'évaluation

- Water and Diamond ParadoxDocument19 pagesWater and Diamond ParadoxDevraj100% (1)

- $100M Leads: How to Get Strangers to Want to Buy Your StuffD'Everand$100M Leads: How to Get Strangers to Want to Buy Your StuffÉvaluation : 5 sur 5 étoiles5/5 (12)

- $100M Offers: How to Make Offers So Good People Feel Stupid Saying NoD'Everand$100M Offers: How to Make Offers So Good People Feel Stupid Saying NoÉvaluation : 5 sur 5 étoiles5/5 (20)

- Surrounded by Idiots: The Four Types of Human Behavior and How to Effectively Communicate with Each in Business (and in Life) (The Surrounded by Idiots Series) by Thomas Erikson: Key Takeaways, Summary & AnalysisD'EverandSurrounded by Idiots: The Four Types of Human Behavior and How to Effectively Communicate with Each in Business (and in Life) (The Surrounded by Idiots Series) by Thomas Erikson: Key Takeaways, Summary & AnalysisÉvaluation : 4.5 sur 5 étoiles4.5/5 (2)