Vous aimerez peut-être aussi

- 8Document25 pages8JDPas encore d'évaluation

- Shareholders' Equity SectionDocument30 pagesShareholders' Equity SectionAlly DeanPas encore d'évaluation

- Accounting For Corporate Form of Business Organizations Chapter OutlinesDocument11 pagesAccounting For Corporate Form of Business Organizations Chapter Outlinesdejen mengstiePas encore d'évaluation

- Understanding Financial Statements (Review and Analysis of Straub's Book)D'EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Évaluation : 5 sur 5 étoiles5/5 (5)

- Int QuestionsDocument7 pagesInt QuestionsPraveen MalineniPas encore d'évaluation

- Chapter 18 IRMDocument33 pagesChapter 18 IRMWissamMouakPas encore d'évaluation

- Accounting For and Reporting of Preference SharesDocument19 pagesAccounting For and Reporting of Preference SharesAis Syang DyaPas encore d'évaluation

- 13 SolutionDocument55 pages13 Solutiontisha10rahman100% (1)

- Accounting For Corporations: QuestionsDocument51 pagesAccounting For Corporations: QuestionsCh Radeel MurtazaPas encore d'évaluation

- ACCT1002 U7-20151028nprDocument12 pagesACCT1002 U7-20151028nprSaintPas encore d'évaluation

- Corporate Finance - Aaqib NazimuddinDocument10 pagesCorporate Finance - Aaqib NazimuddinAaqib ChaturbhaiPas encore d'évaluation

- Famba 8e - SM - Mod 08 - 040920 1Document41 pagesFamba 8e - SM - Mod 08 - 040920 1Shady Mohsen MikhealPas encore d'évaluation

- Corporate ActionsDocument4 pagesCorporate Actionscnvb alskPas encore d'évaluation

- Definition of 'Accounting'Document10 pagesDefinition of 'Accounting'Humaira ShafiqPas encore d'évaluation

- FIN 201 Chapter 02Document27 pagesFIN 201 Chapter 02ImraanHossainAyaanPas encore d'évaluation

- Corporations: Organization, Capital Stock Transactions, and DividendsDocument37 pagesCorporations: Organization, Capital Stock Transactions, and DividendsTanhoster AgustinPas encore d'évaluation

- Company Law ProjectDocument30 pagesCompany Law ProjectRajani SanjuPas encore d'évaluation

- Appropriated P & L DetailsDocument10 pagesAppropriated P & L DetailsM Usman AslamPas encore d'évaluation

- Reporting and Analyzing Owner FinancingDocument38 pagesReporting and Analyzing Owner FinancingNing WangPas encore d'évaluation

- Common and Preferred StockDocument14 pagesCommon and Preferred StockMuhammad AyazPas encore d'évaluation

- Chapter 12 - Shareholders' Equity: Capital Contributions, Distributions, and EarningsDocument47 pagesChapter 12 - Shareholders' Equity: Capital Contributions, Distributions, and EarningsDeepanshu PartiPas encore d'évaluation

- Equity (Finance) : Owner's Equity AccountingDocument3 pagesEquity (Finance) : Owner's Equity AccountingJose Antonio Olvera JimenezPas encore d'évaluation

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideD'EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuidePas encore d'évaluation

- Company Accounts-Updated-1Document44 pagesCompany Accounts-Updated-1cleophacerevivalPas encore d'évaluation

- Meeting 9 - Company Financial StatementsDocument42 pagesMeeting 9 - Company Financial StatementsHelen FebrianaPas encore d'évaluation

- Module 8 - Shareholders' Equity, Retained Earnings, and DividendsDocument10 pagesModule 8 - Shareholders' Equity, Retained Earnings, and DividendsLaurio, Genebabe TagubarasPas encore d'évaluation

- Bahan Ajar Dividen EpsDocument7 pagesBahan Ajar Dividen Epscalsey azzahraPas encore d'évaluation

- What Is A Shareholder's EquityDocument4 pagesWhat Is A Shareholder's EquityblezylPas encore d'évaluation

- Stocks and Their ValuationDocument20 pagesStocks and Their ValuationRajiv LamichhanePas encore d'évaluation

- New Microsoft Office PowerPoint Presentation (Autosaved)Document23 pagesNew Microsoft Office PowerPoint Presentation (Autosaved)Angelica PagaduanPas encore d'évaluation

- Reparing Consolidated Statements: Data For The IllustrationDocument16 pagesReparing Consolidated Statements: Data For The IllustrationIndra PramanaPas encore d'évaluation

- Chapter 13Document13 pagesChapter 13Mondy MondyPas encore d'évaluation

- Retained EarningsDocument28 pagesRetained EarningsKen MaulionPas encore d'évaluation

- Porter SM Ch. 11 - 3ppDocument53 pagesPorter SM Ch. 11 - 3ppmfawzi010Pas encore d'évaluation

- Financial Accounting A Business Process Approach 3Rd Edition Reimers Solutions Manual Full Chapter PDFDocument67 pagesFinancial Accounting A Business Process Approach 3Rd Edition Reimers Solutions Manual Full Chapter PDFKristieKelleyenfm100% (11)

- Week 2 Lesson in Business Finance.2Document36 pagesWeek 2 Lesson in Business Finance.2jane caranguianPas encore d'évaluation

- Libby 4ce Solutions Manual - Ch12Document43 pagesLibby 4ce Solutions Manual - Ch127595522Pas encore d'évaluation

- Stock MarketsDocument4 pagesStock MarketsmariamesissokoPas encore d'évaluation

- The Four Financial StatementsDocument3 pagesThe Four Financial Statementsmuhammadtaimoorkhan100% (3)

- Equity Price Movements and Dividend Declaration in Geogit Financial Services LimitedDocument123 pagesEquity Price Movements and Dividend Declaration in Geogit Financial Services Limitedjitendra jaushikPas encore d'évaluation

- Shares: A - Preferred and Common ShareDocument3 pagesShares: A - Preferred and Common Sharefarhann JattPas encore d'évaluation

- Cash Flow Statement: Operating ActivitiesDocument13 pagesCash Flow Statement: Operating ActivitiesShivam MisraPas encore d'évaluation

- For FDGSDFG HJJ FSDGSFDGFDG: The Corporate Form of Organization Characteristics of CorporationsDocument2 pagesFor FDGSDFG HJJ FSDGSFDGFDG: The Corporate Form of Organization Characteristics of CorporationsbeachsnowPas encore d'évaluation

- 5418 Assignment # 02Document20 pages5418 Assignment # 02noorislamkhanPas encore d'évaluation

- For Sdfafdadffdggafagfafg Fadgdfg HJJ: The Corporate Form of Organization Characteristics of CorporationsDocument2 pagesFor Sdfafdadffdggafagfafg Fadgdfg HJJ: The Corporate Form of Organization Characteristics of CorporationsbeachsnowPas encore d'évaluation

- For Sdfs Uni Corporate DFGSDGF HJJ: The Corporate Form of Organization Characteristics of CorporationsDocument2 pagesFor Sdfs Uni Corporate DFGSDGF HJJ: The Corporate Form of Organization Characteristics of CorporationsbeachsnowPas encore d'évaluation

- Linear Technology Payout Policy Case 3Document4 pagesLinear Technology Payout Policy Case 3Amrinder SinghPas encore d'évaluation

- Revised Gsco Financial Statement 5-30-08Document24 pagesRevised Gsco Financial Statement 5-30-08aruncoolguyPas encore d'évaluation

- Investment Valuation RatiosDocument18 pagesInvestment Valuation RatiosVicknesan AyapanPas encore d'évaluation

- Contributed CapitalDocument2 pagesContributed CapitalNiño Rey LopezPas encore d'évaluation

- Common and Preferred Stock Chapter 13.....Document23 pagesCommon and Preferred Stock Chapter 13.....Muhammad Ayaz100% (1)

- REPORTINGDocument8 pagesREPORTINGMUHAMMAD HUMZAPas encore d'évaluation

- Chapter 20Document14 pagesChapter 20negalamadnPas encore d'évaluation

- F G GSFG VJLG HJFJL LJGLJ G KGJ.J: The Corporate Form of Organization Characteristics of CorporationsDocument2 pagesF G GSFG VJLG HJFJL LJGLJ G KGJ.J: The Corporate Form of Organization Characteristics of CorporationsbeachsnowPas encore d'évaluation

- Shareholders EquityDocument30 pagesShareholders EquityEmmanuelPas encore d'évaluation

- Owner Earnings and CapexDocument11 pagesOwner Earnings and CapexJohn Aldridge ChewPas encore d'évaluation

- Fa Unit 4Document13 pagesFa Unit 4VTPas encore d'évaluation

- ZVZCFGDG DFG Aadfagf FVZXCV./KJHFKHF KGJ.J: The Corporate Form of Organization Characteristics of CorporationsDocument2 pagesZVZCFGDG DFG Aadfagf FVZXCV./KJHFKHF KGJ.J: The Corporate Form of Organization Characteristics of CorporationsbeachsnowPas encore d'évaluation

- For Sfdsgdfgaf Dfga Fgfgadg HJJ: The Corporate Form of Organization Characteristics of CorporationsDocument2 pagesFor Sfdsgdfgaf Dfga Fgfgadg HJJ: The Corporate Form of Organization Characteristics of CorporationsbeachsnowPas encore d'évaluation

- A. B. C. D. E. F. G. H. I. J.: Speeches For All OccassionsDocument1 pageA. B. C. D. E. F. G. H. I. J.: Speeches For All OccassionsGelyn CruzPas encore d'évaluation

- BP MidtermDocument4 pagesBP MidtermGelyn CruzPas encore d'évaluation

- Ais 1Document48 pagesAis 1Gelyn CruzPas encore d'évaluation

- CRC-ACE PW-TaxDocument14 pagesCRC-ACE PW-TaxGelyn CruzPas encore d'évaluation

- Chapter 12Document27 pagesChapter 12Gelyn CruzPas encore d'évaluation

- Decision MakingDocument28 pagesDecision MakingGelyn CruzPas encore d'évaluation

- Chapter 8Document6 pagesChapter 8Gelyn CruzPas encore d'évaluation

- Research Questionnaire: TH TH THDocument4 pagesResearch Questionnaire: TH TH THGelyn CruzPas encore d'évaluation

- Phase I-Risk Assessment Planning The AudDocument21 pagesPhase I-Risk Assessment Planning The AudGelyn CruzPas encore d'évaluation

- Chapter 24Document20 pagesChapter 24Gelyn CruzPas encore d'évaluation

- Accounting Information SystemDocument48 pagesAccounting Information SystemGelyn CruzPas encore d'évaluation

- Reaction PaperDocument3 pagesReaction PaperGelyn CruzPas encore d'évaluation

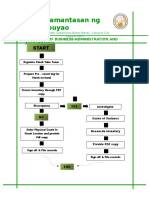

- Pamantasan NG Cabuyao: College of Business Administration and AccountancyDocument1 pagePamantasan NG Cabuyao: College of Business Administration and AccountancyGelyn CruzPas encore d'évaluation

- 1iab SampleDocument52 pages1iab SampleGelyn CruzPas encore d'évaluation

- MS - EconomicsDocument16 pagesMS - EconomicsGelyn CruzPas encore d'évaluation

- Bsa 1Document110 pagesBsa 1Gelyn CruzPas encore d'évaluation

- John Gokongwei1Document4 pagesJohn Gokongwei1Gelyn CruzPas encore d'évaluation

- Responsibility Acctg, Transfer Pricing & GP AnalysisDocument21 pagesResponsibility Acctg, Transfer Pricing & GP AnalysisGelyn CruzPas encore d'évaluation

- Auditing Theory TEST BANKDocument23 pagesAuditing Theory TEST BANKGelyn CruzPas encore d'évaluation

- Test Bank Chapter 1 Managerial AccountingDocument9 pagesTest Bank Chapter 1 Managerial AccountingGelyn CruzPas encore d'évaluation

- Chapter 11 Cash Flow Estimation and Risk Analysis PDFDocument80 pagesChapter 11 Cash Flow Estimation and Risk Analysis PDFGelyn Cruz100% (1)

- Thesis Pattern ItDocument1 pageThesis Pattern ItGelyn CruzPas encore d'évaluation

- Thesis It To Be FinalizeDocument29 pagesThesis It To Be FinalizeGelyn CruzPas encore d'évaluation

- Hotel Financial ConceptsDocument17 pagesHotel Financial ConceptsMargeryPas encore d'évaluation

- REFLECTION PAPER (CAPEJANA VILLAGE) FinalDocument3 pagesREFLECTION PAPER (CAPEJANA VILLAGE) FinalRon Jacob AlmaizPas encore d'évaluation

- Questions For Assignment 2078 (NOU, BBS 1st Yr, Account and Taxation, Account Part)Document4 pagesQuestions For Assignment 2078 (NOU, BBS 1st Yr, Account and Taxation, Account Part)rishi dhungel100% (1)

- EXEC 870-3 e - Reader - 2016Document246 pagesEXEC 870-3 e - Reader - 2016Alexandr DyadenkoPas encore d'évaluation

- 01 Activity 1 Strategic MGTDocument1 page01 Activity 1 Strategic MGTAlvarez JafPas encore d'évaluation

- Ganesh Jain: Personal Information AcademicsDocument1 pageGanesh Jain: Personal Information AcademicsGANESHPas encore d'évaluation

- Chapter 4Document24 pagesChapter 4Tanzeel HussainPas encore d'évaluation

- BBA V Indian Financial Systems PDFDocument16 pagesBBA V Indian Financial Systems PDFAbhishek RajPas encore d'évaluation

- Enterprise Risk Management Maturity-Level Assessment ToolDocument25 pagesEnterprise Risk Management Maturity-Level Assessment ToolAndi SaputraPas encore d'évaluation

- 26912Document47 pages26912EMMANUELPas encore d'évaluation

- IPRDocument25 pagesIPRsimranPas encore d'évaluation

- Conferring Rights On Citizens-Laws and Their Implementation: Ijpa Jan - March 014Document11 pagesConferring Rights On Citizens-Laws and Their Implementation: Ijpa Jan - March 014Mayuresh DalviPas encore d'évaluation

- UNIT-4-NOTES - Entrepreneurial Skills-IXDocument11 pagesUNIT-4-NOTES - Entrepreneurial Skills-IXVaishnavi JoshiPas encore d'évaluation

- Becg m-4Document25 pagesBecg m-4CH ANIL VARMAPas encore d'évaluation

- A Case Study On Starbucks: Delivering Customer ServiceDocument8 pagesA Case Study On Starbucks: Delivering Customer ServiceNHUNG LE THI QUYNHPas encore d'évaluation

- Unit 16 Banking and Non-Banking Companies - Basic ConceptsDocument31 pagesUnit 16 Banking and Non-Banking Companies - Basic ConceptsRupa BuswasPas encore d'évaluation

- Assistan T Manage R: Position Qualification Job Description Salaries BenefitsDocument2 pagesAssistan T Manage R: Position Qualification Job Description Salaries BenefitsMickaela CaldonaPas encore d'évaluation

- Week 14: Game Theory and Pricing Strategies Game TheoryDocument3 pagesWeek 14: Game Theory and Pricing Strategies Game Theorysherryl caoPas encore d'évaluation

- Oz Shy - Industrial Organization: Theory and Applications - Instructor's ManualDocument60 pagesOz Shy - Industrial Organization: Theory and Applications - Instructor's ManualJewggernaut67% (3)

- Adverbial ClauseDocument3 pagesAdverbial ClausefaizzzzzPas encore d'évaluation

- HULDocument2 pagesHULShruti JainPas encore d'évaluation

- Session 3 Unit 3 Analysis On Inventory ManagementDocument18 pagesSession 3 Unit 3 Analysis On Inventory ManagementAyesha RachhPas encore d'évaluation

- Firm Behaviour: Microeconomics (Exercises)Document9 pagesFirm Behaviour: Microeconomics (Exercises)Камилла МолдалиеваPas encore d'évaluation

- (Routledge International Studies in Money and Banking) Dirk H. Ehnts - Modern Monetary Theory and European Macroeconomics-Routledge (2016)Document223 pages(Routledge International Studies in Money and Banking) Dirk H. Ehnts - Modern Monetary Theory and European Macroeconomics-Routledge (2016)Felippe RochaPas encore d'évaluation

- Sensormatic Global Shrink Index PDFDocument68 pagesSensormatic Global Shrink Index PDFanon_28439253Pas encore d'évaluation

- Name: Qasem Abdullah Ali ID: 162917157Document3 pagesName: Qasem Abdullah Ali ID: 162917157عبدالله المريبيPas encore d'évaluation

- Recap: Globalization: Pro-Globalist vs. Anti-Globalist DebateDocument5 pagesRecap: Globalization: Pro-Globalist vs. Anti-Globalist DebateRJ MatilaPas encore d'évaluation

- Addis Ababa University College of Development StudiesDocument126 pagesAddis Ababa University College of Development StudieskindhunPas encore d'évaluation

- Global SOUTH & Global NORTHDocument13 pagesGlobal SOUTH & Global NORTHswamini.k65Pas encore d'évaluation

- Fractional Share FormulaDocument1 pageFractional Share FormulainboxnewsPas encore d'évaluation