Vous aimerez peut-être aussi

- Unit 5 Woking CapitalDocument10 pagesUnit 5 Woking CapitalRich ManPas encore d'évaluation

- Corporate FinanceDocument31 pagesCorporate FinanceAbhi RainaPas encore d'évaluation

- Module IV: Working Capital ManagementDocument19 pagesModule IV: Working Capital Managementanusmayavbs1Pas encore d'évaluation

- Working CapitalDocument60 pagesWorking CapitaljubinPas encore d'évaluation

- Working Capital ManagementDocument8 pagesWorking Capital ManagementSenthilSelvaPas encore d'évaluation

- Working Capital ManagementDocument56 pagesWorking Capital ManagementmanuPas encore d'évaluation

- Working CapDocument19 pagesWorking CapJuhi SharmaPas encore d'évaluation

- Working Capital of Vim Dye ChemDocument15 pagesWorking Capital of Vim Dye ChemJIGAR SHAHPas encore d'évaluation

- Working Capital ManagementDocument52 pagesWorking Capital Managementforevers2218Pas encore d'évaluation

- Management of Working Capital: Ajeet Kumar ThakurDocument125 pagesManagement of Working Capital: Ajeet Kumar ThakurDilip Kumar YadavPas encore d'évaluation

- WMDocument31 pagesWMNiña Rhocel YangcoPas encore d'évaluation

- Principles of Working Capital Management-1Document29 pagesPrinciples of Working Capital Management-1margetPas encore d'évaluation

- Working CapitalDocument7 pagesWorking CapitalSreenath SreePas encore d'évaluation

- Submitted By: Prince Sharma M.B.A-II ROLL NO.-22 Submitted To: - Prof. Geetika GroverDocument8 pagesSubmitted By: Prince Sharma M.B.A-II ROLL NO.-22 Submitted To: - Prof. Geetika GroverShubhamPas encore d'évaluation

- Sources of Working Capital Finance EssayDocument11 pagesSources of Working Capital Finance EssayMehak JainPas encore d'évaluation

- Working Capital ManagementDocument6 pagesWorking Capital Managementarchana_anuragiPas encore d'évaluation

- MBA ProjectDocument15 pagesMBA ProjectkrishnithyanPas encore d'évaluation

- Working CapitalDocument9 pagesWorking CapitalSahil PasrijaPas encore d'évaluation

- Working Capital ManagementDocument44 pagesWorking Capital ManagementPhaniraj Lenkalapally100% (1)

- What Is Working Capital Management (WCM)Document26 pagesWhat Is Working Capital Management (WCM)Sudip BaruaPas encore d'évaluation

- Principles of Working Capital ManagementDocument45 pagesPrinciples of Working Capital ManagementSohini ChakrabortyPas encore d'évaluation

- Working Capital ManagementDocument62 pagesWorking Capital ManagementSuresh Dhanapal100% (1)

- BF CH 5Document12 pagesBF CH 5IzHar YousafzaiPas encore d'évaluation

- Working Capital Management in Vardhman-Final ProjectDocument84 pagesWorking Capital Management in Vardhman-Final ProjectRaj Kumar100% (3)

- Wc-Aditya BirlaDocument81 pagesWc-Aditya BirlaDominic Roshan DDRPas encore d'évaluation

- Working Capital: by Dr. M S KhanDocument13 pagesWorking Capital: by Dr. M S KhanMohd. Shadab khanPas encore d'évaluation

- Financial MGMT Notes - Unit VDocument10 pagesFinancial MGMT Notes - Unit Vhimanshujoshi7789Pas encore d'évaluation

- Management Accounting - II: Presented by Dr. Arvind Rayalwar Assistant Professor Department of Commerce, SSM BeedDocument30 pagesManagement Accounting - II: Presented by Dr. Arvind Rayalwar Assistant Professor Department of Commerce, SSM BeedArvind RayalwarPas encore d'évaluation

- Working Capital ManagementDocument79 pagesWorking Capital ManagementAbhilash GopalPas encore d'évaluation

- PageDocument24 pagesPagearpithaacchu76Pas encore d'évaluation

- Working Capital RequirementDocument26 pagesWorking Capital RequirementAdityaPas encore d'évaluation

- Working CapitalDocument15 pagesWorking CapitalAdeem AshrafiPas encore d'évaluation

- Understanding Working CapitalDocument11 pagesUnderstanding Working CapitalRohit BajpaiPas encore d'évaluation

- Ambuja Cements Was Set Up in 1986Document13 pagesAmbuja Cements Was Set Up in 1986himaswethaPas encore d'évaluation

- Working Capital ManagementDocument32 pagesWorking Capital ManagementVineeta BhatiPas encore d'évaluation

- Role of Banks in Working Capital ManagementDocument59 pagesRole of Banks in Working Capital Managementashwin thakurPas encore d'évaluation

- Harish YadacccccDocument60 pagesHarish YadacccccjubinPas encore d'évaluation

- Body PartDocument66 pagesBody PartSourabh SabatPas encore d'évaluation

- Acc 301 Corporate Finance - Lectures Two - ThreeDocument17 pagesAcc 301 Corporate Finance - Lectures Two - ThreeFolarin EmmanuelPas encore d'évaluation

- Chapter 1Document121 pagesChapter 1Santosh GuptaPas encore d'évaluation

- New Research 2017Document19 pagesNew Research 2017SAKSHI GUPTAPas encore d'évaluation

- Working CapitalDocument49 pagesWorking CapitalRicha SharmaPas encore d'évaluation

- Yashoda Again Edit Content File.........................Document64 pagesYashoda Again Edit Content File.........................aasthashukla902Pas encore d'évaluation

- Professional Practices Lecture 7Document21 pagesProfessional Practices Lecture 7Talha ChaudharyPas encore d'évaluation

- New Microsoft Office Word DocumentDocument5 pagesNew Microsoft Office Word Documentrajput12345Pas encore d'évaluation

- Chapter 1.1 Working Capital Management 1.1 .1conceptDocument55 pagesChapter 1.1 Working Capital Management 1.1 .1conceptMAYUGAMPas encore d'évaluation

- Summer Training Report: On "Training of Employees" ATDocument56 pagesSummer Training Report: On "Training of Employees" ATGauravPas encore d'évaluation

- Working Capital On Telecommunication IndustryDocument54 pagesWorking Capital On Telecommunication IndustrySAGARPas encore d'évaluation

- Working Capital ManagementDocument44 pagesWorking Capital ManagementIvani KatalPas encore d'évaluation

- Final ProjectDocument20 pagesFinal ProjectBalkaran SinghPas encore d'évaluation

- Working Capital Management: DefinitionDocument50 pagesWorking Capital Management: DefinitionĶąřťhï ĞõűđPas encore d'évaluation

- Working Capital FinanceDocument17 pagesWorking Capital FinanceAnitha GirigoudruPas encore d'évaluation

- What Is Working Capital ManagementDocument17 pagesWhat Is Working Capital ManagementKhushboo NagpalPas encore d'évaluation

- Working Capital Management in Icici PrudentialDocument83 pagesWorking Capital Management in Icici PrudentialVipul TandonPas encore d'évaluation

- Understanding Financial Statements (Review and Analysis of Straub's Book)D'EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Évaluation : 5 sur 5 étoiles5/5 (5)

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingD'EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingPas encore d'évaluation

- Furniture Furnishing PDFDocument63 pagesFurniture Furnishing PDFSushil Kumar JangirPas encore d'évaluation

- Employee RelocationDocument10 pagesEmployee RelocationVin BankaPas encore d'évaluation

- NCFDocument159 pagesNCFsachindatt9Pas encore d'évaluation

- United Nations Literacy Decade: International Strategic Framework For ActionDocument51 pagesUnited Nations Literacy Decade: International Strategic Framework For ActionVin BankaPas encore d'évaluation

- ATM Premises RequirementDocument3 pagesATM Premises RequirementVin BankaPas encore d'évaluation

- Health and Safety Management Systems - ArchiveDocument250 pagesHealth and Safety Management Systems - ArchiveMohamad ZackuanPas encore d'évaluation

- Health and Safety Management Systems - ArchiveDocument250 pagesHealth and Safety Management Systems - ArchiveMohamad ZackuanPas encore d'évaluation

- Marketing Management - Market SegmentationDocument26 pagesMarketing Management - Market SegmentationAmit TatedPas encore d'évaluation

- Iso 9000 Case StudyDocument10 pagesIso 9000 Case StudyVin BankaPas encore d'évaluation

- E Shield Sales BrochureDocument8 pagesE Shield Sales BrochuresgrsthPas encore d'évaluation

- Indian Textile IndustryDocument17 pagesIndian Textile IndustryVin BankaPas encore d'évaluation

- ISO 9000 Implementation at The Me-An Shoe CompanyDocument4 pagesISO 9000 Implementation at The Me-An Shoe CompanyVin BankaPas encore d'évaluation

- Financial Management in Psu'sDocument14 pagesFinancial Management in Psu'sAkshaya Mali100% (1)

- Economic Scams in IndiaDocument46 pagesEconomic Scams in IndiaVin BankaPas encore d'évaluation

- Swot Analysis of The Indian Textile IndustryDocument30 pagesSwot Analysis of The Indian Textile IndustryDeepali Choudhary57% (14)

- Vision Strategy Action Plan For Indian Textile SectorDocument24 pagesVision Strategy Action Plan For Indian Textile SectorVin BankaPas encore d'évaluation

- EVA Widgets - Com-01-08-2019Document7 pagesEVA Widgets - Com-01-08-2019proPas encore d'évaluation

- Governmental and Nonprofit Accounting 10th Edition Smith Test BankDocument13 pagesGovernmental and Nonprofit Accounting 10th Edition Smith Test BankHeatherHayescwboz100% (19)

- Financial Accounting The Impact On Decision Makers 10th Edition Porter Solutions ManualDocument41 pagesFinancial Accounting The Impact On Decision Makers 10th Edition Porter Solutions Manualhildabacvvz100% (27)

- Copy of 62551kunci Jawaban PT Kharisma Digital910 PDFDocument32 pagesCopy of 62551kunci Jawaban PT Kharisma Digital910 PDFNirdila KrismawatiPas encore d'évaluation

- Chapter 7 Asset Investment Decisions and Capital RationingDocument31 pagesChapter 7 Asset Investment Decisions and Capital RationingdperepolkinPas encore d'évaluation

- Section B Answer Question 1 and Not More Than One Further Question From This Section. Question 1Document3 pagesSection B Answer Question 1 and Not More Than One Further Question From This Section. Question 1Kəmalə AslanzadəPas encore d'évaluation

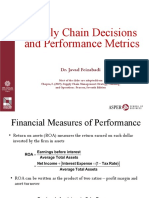

- 3-Supply Chain Decisions and Performance Metrics (A)Document21 pages3-Supply Chain Decisions and Performance Metrics (A)eeman kPas encore d'évaluation

- Profit/Loss & Cash Flow ProjectionsDocument9 pagesProfit/Loss & Cash Flow ProjectionsKervin DavantesPas encore d'évaluation

- Future of PE and VCDocument14 pagesFuture of PE and VCReaderPas encore d'évaluation

- CA Final G2 SFM Paper 2 SolutionDocument13 pagesCA Final G2 SFM Paper 2 SolutionDEVANSHPas encore d'évaluation

- Stock Market Edges Patterns PDFDocument53 pagesStock Market Edges Patterns PDFbopparaju kranthiPas encore d'évaluation

- Remedies in Bankruptcy SummaryDocument5 pagesRemedies in Bankruptcy SummaryKhairun Nisaazwani100% (4)

- Expected Credit LossDocument6 pagesExpected Credit Losstunlinoo.067433Pas encore d'évaluation

- SOIC Allocation Sheet Lyst3011Document4 pagesSOIC Allocation Sheet Lyst3011Manish GargPas encore d'évaluation

- Yoseva Yuliana DH Ruju - Chapter 20Document2 pagesYoseva Yuliana DH Ruju - Chapter 20Septy RujuPas encore d'évaluation

- DWDWDocument178 pagesDWDWJericho Pedragosa100% (1)

- Economic Value Added: EVA Is An Estimate of A Firm's Economic Profit - BeingDocument7 pagesEconomic Value Added: EVA Is An Estimate of A Firm's Economic Profit - BeingSunil Kumar SahooPas encore d'évaluation

- This Study Resource Was: MBA 641 Managerial Accounting Class Exercises Chapter 6: Variable Costing and Segment ReportingDocument6 pagesThis Study Resource Was: MBA 641 Managerial Accounting Class Exercises Chapter 6: Variable Costing and Segment ReportingJun-Mari VisayaPas encore d'évaluation

- Financial Performance MeasuresDocument15 pagesFinancial Performance MeasuresNigel A.L. Brooks67% (3)

- Stock Analysis Excel Revised March 2017Document26 pagesStock Analysis Excel Revised March 2017Sangram Panda100% (1)

- SASF Mock Exam Answers December 2004 - Level I Page 4 of 30Document2 pagesSASF Mock Exam Answers December 2004 - Level I Page 4 of 30SmileOYPas encore d'évaluation

- Inventory ValuationDocument32 pagesInventory ValuationSHENUPas encore d'évaluation

- Question-Ias 2 - Ias 16 and Ias 40 - Admin-2019-2020-1Document6 pagesQuestion-Ias 2 - Ias 16 and Ias 40 - Admin-2019-2020-1Letsah BrightPas encore d'évaluation

- TGS - Mentorship 2.0Document11 pagesTGS - Mentorship 2.0Aakash KumarPas encore d'évaluation

- JFW464 Analisis Penyata Kewangan Sidang Webex 5 Bab 10 Analisis KreditDocument39 pagesJFW464 Analisis Penyata Kewangan Sidang Webex 5 Bab 10 Analisis KreditM-Hilme M-HassanPas encore d'évaluation

- ACCT550 Homework Week 1Document6 pagesACCT550 Homework Week 1Natasha DeclanPas encore d'évaluation

- 1001 Practice QuestionsDocument95 pages1001 Practice QuestionsMohamad El-JadayelPas encore d'évaluation

- Debt Restructure - SIM - 0Document14 pagesDebt Restructure - SIM - 0lilienesieraPas encore d'évaluation

- 04 REO HO-MAS FS Analysis Consultation HODocument3 pages04 REO HO-MAS FS Analysis Consultation HOCeline RiveraPas encore d'évaluation

- Corporate Finance Midterm Exam 201810 With CorrectionsDocument7 pagesCorporate Finance Midterm Exam 201810 With CorrectionsMohd OzairPas encore d'évaluation