Vous aimerez peut-être aussi

- Banking India: Accepting Deposits for the Purpose of LendingD'EverandBanking India: Accepting Deposits for the Purpose of LendingPas encore d'évaluation

- Major Bank Fraud Cases: A Critical ReviewD'EverandMajor Bank Fraud Cases: A Critical ReviewÉvaluation : 4.5 sur 5 étoiles4.5/5 (6)

- BanksDocument120 pagesBankskoshycjPas encore d'évaluation

- History of Banking in India: 1) Pre-Nationalization EraDocument7 pagesHistory of Banking in India: 1) Pre-Nationalization EraKoshyPas encore d'évaluation

- Scenario of Foreign Banks in IndiaDocument62 pagesScenario of Foreign Banks in IndiaYesha Khona100% (1)

- TH THDocument34 pagesTH THpmmppmPas encore d'évaluation

- Project Report On Personal Loan CompressDocument62 pagesProject Report On Personal Loan CompressSudhakar GuntukaPas encore d'évaluation

- Non Performing AssetsDocument89 pagesNon Performing AssetsNazma MalikPas encore d'évaluation

- Comparative Study Between Two BanksDocument26 pagesComparative Study Between Two BanksAnupam SinghPas encore d'évaluation

- Fundamental Analysis of Banking Sector in IndiaDocument17 pagesFundamental Analysis of Banking Sector in IndiaGauri BiyaniPas encore d'évaluation

- Sbi and Hdfc"COMPARATIVE STUDY OF CUSTOMER'S SATISFACTION TOWARDS HDFC BANK AND STATE BANK OF INDIADocument68 pagesSbi and Hdfc"COMPARATIVE STUDY OF CUSTOMER'S SATISFACTION TOWARDS HDFC BANK AND STATE BANK OF INDIArupesh singh84% (31)

- Chapter-1 Introduction 1.1 Introduction About The SectorDocument60 pagesChapter-1 Introduction 1.1 Introduction About The SectorGaurav Goyal100% (2)

- Project - Loans and AdvancesDocument60 pagesProject - Loans and AdvancesRajendra Gawate75% (12)

- Chapter - Iii An Introduction To Banking and Banking ServicesDocument28 pagesChapter - Iii An Introduction To Banking and Banking ServicesVijay KumarPas encore d'évaluation

- 12 - Chapter 2 PDFDocument32 pages12 - Chapter 2 PDFManali ShahPas encore d'évaluation

- Project On Job SatisfcationDocument84 pagesProject On Job Satisfcationnamitaahuja2006Pas encore d'évaluation

- And Long Term" Which Is Accomplished During The Training Bank of Baroda, SME LOANDocument246 pagesAnd Long Term" Which Is Accomplished During The Training Bank of Baroda, SME LOANkanchanmbmPas encore d'évaluation

- Rural DevelopmentsDocument88 pagesRural DevelopmentsVyom K ShahPas encore d'évaluation

- A Study On Credit Appraisal Process On Lotak Mahindra Bank (Draft)Document54 pagesA Study On Credit Appraisal Process On Lotak Mahindra Bank (Draft)Rhea SrivastavaPas encore d'évaluation

- A Research Report On SbiDocument45 pagesA Research Report On SbiSonu LovesforuPas encore d'évaluation

- A Study On Customer Relationship Management at Bandhan Bank LimitedDocument55 pagesA Study On Customer Relationship Management at Bandhan Bank LimitedRIDDHIPas encore d'évaluation

- The Oxford Dictionary Defines The Bank AsDocument51 pagesThe Oxford Dictionary Defines The Bank AsMeenu RaniPas encore d'évaluation

- Universal BankingDocument50 pagesUniversal BankingBennett CheenathPas encore d'évaluation

- Chapter 1Document37 pagesChapter 1Kalyan Reddy AnuguPas encore d'évaluation

- Project On SBI BankDocument48 pagesProject On SBI BankArvind Mahandhwal80% (5)

- Sbi and HDFC Comparative Study of Customer S Satisfaction TowardsDocument67 pagesSbi and HDFC Comparative Study of Customer S Satisfaction TowardsMõørthï Shãrmâ75% (4)

- Financial Inclusion FinalDocument54 pagesFinancial Inclusion FinalSOHAM DESAIPas encore d'évaluation

- Banking System and Structure in India Evolution of Indian BanksDocument61 pagesBanking System and Structure in India Evolution of Indian BanksTrilok IndiPas encore d'évaluation

- A Study On Type of Bank FinancingDocument18 pagesA Study On Type of Bank FinancingAjeet YadavPas encore d'évaluation

- Project: G I B SDocument26 pagesProject: G I B Srohit utekarPas encore d'évaluation

- Term Paper: Topic: Study On Private and Public Sector BankDocument23 pagesTerm Paper: Topic: Study On Private and Public Sector BankniharikatyagiPas encore d'évaluation

- Banking Sector in India - A ReviewDocument8 pagesBanking Sector in India - A ReviewHarshvardhan SurekaPas encore d'évaluation

- Banking Sector in India - A ReviewDocument8 pagesBanking Sector in India - A ReviewSandeep Singh BhandariPas encore d'évaluation

- Banking Sector in India - A ReviewDocument8 pagesBanking Sector in India - A ReviewSandeep Singh BhandariPas encore d'évaluation

- Growth in Indian Banking SectorDocument59 pagesGrowth in Indian Banking SectorKishan KudiaPas encore d'évaluation

- I. Evolution of Banking in IndiaDocument19 pagesI. Evolution of Banking in IndiajyotsnandPas encore d'évaluation

- A Study On Customer Relationship Management at Bandhan Bank LimitedDocument55 pagesA Study On Customer Relationship Management at Bandhan Bank LimitedNitinAgnihotriPas encore d'évaluation

- Chapter: 1 Introduction: Services Provided by Banking OrganizationsDocument56 pagesChapter: 1 Introduction: Services Provided by Banking OrganizationsAmol RakshePas encore d'évaluation

- Untitled 1Document14 pagesUntitled 1Tushar BhatiPas encore d'évaluation

- Project Report On Role of Banks in Indian EconomyDocument29 pagesProject Report On Role of Banks in Indian EconomyNeeraj UpadhyayPas encore d'évaluation

- Bank of Maharashtra Home LoanDocument95 pagesBank of Maharashtra Home Loansayyadsajidali100% (5)

- ICICI Project ReportDocument53 pagesICICI Project ReportPawan MeenaPas encore d'évaluation

- Bank of Baroda HomeloanDocument63 pagesBank of Baroda HomeloansantoshPas encore d'évaluation

- Indian Banking & The Road AheadDocument33 pagesIndian Banking & The Road AheadViral ShahPas encore d'évaluation

- Job Satisfaction at SBI Project Report Mba HRDocument78 pagesJob Satisfaction at SBI Project Report Mba HRBabasab Patil (Karrisatte)0% (1)

- 3935cstudy Material On Banking Law 1Document9 pages3935cstudy Material On Banking Law 1NancygirdherPas encore d'évaluation

- ParveezDocument55 pagesParveezRameem PaPas encore d'évaluation

- Nationalisation of Banks in IndiaDocument5 pagesNationalisation of Banks in IndiaPravish Lionel DcostaPas encore d'évaluation

- "Credit Risk Management in State Bank of India": Title of The ProjectDocument43 pages"Credit Risk Management in State Bank of India": Title of The Projectswarali deshmukhPas encore d'évaluation

- Organizational Structure, Development of Banks in IndiaDocument54 pagesOrganizational Structure, Development of Banks in Indiaanand_lamani100% (1)

- Karnataka Bank ProjectDocument72 pagesKarnataka Bank ProjectBalaji70% (10)

- Discuss The Role of Banking System in Economic Growth and Development of IndiaDocument5 pagesDiscuss The Role of Banking System in Economic Growth and Development of IndiaNaruChoudharyPas encore d'évaluation

- Introduction ToDocument44 pagesIntroduction ToYash SoniPas encore d'évaluation

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)D'EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Pas encore d'évaluation

- The role of banks in the regional economic development of Uzbekistan: lessons from the German experienceD'EverandThe role of banks in the regional economic development of Uzbekistan: lessons from the German experiencePas encore d'évaluation

- Regional Rural Banks of India: Evolution, Performance and ManagementD'EverandRegional Rural Banks of India: Evolution, Performance and ManagementPas encore d'évaluation

- Islamic Banking And Finance for Beginners!D'EverandIslamic Banking And Finance for Beginners!Évaluation : 2 sur 5 étoiles2/5 (1)

- Marketing of Consumer Financial Products: Insights From Service MarketingD'EverandMarketing of Consumer Financial Products: Insights From Service MarketingPas encore d'évaluation

- Dissertation Project On HDFC BankDocument43 pagesDissertation Project On HDFC BankMAHENDRA SHIVAJI DHENAK100% (6)

- Service CharacteristicsDocument8 pagesService CharacteristicsMAHENDRA SHIVAJI DHENAK79% (14)

- 6.the Servuction ModelDocument3 pages6.the Servuction ModelMAHENDRA SHIVAJI DHENAK93% (40)

- The Services Marketing TriangleDocument3 pagesThe Services Marketing TriangleMAHENDRA SHIVAJI DHENAK100% (2)

- Presentation On IOCL - PPT On SUMMER INTERNSHIP PROJECTDocument15 pagesPresentation On IOCL - PPT On SUMMER INTERNSHIP PROJECTMAHENDRA SHIVAJI DHENAK33% (3)

- What Are Different Types of Strategic Missions at SBU Level How Do These Missions Affect Strategic Planning Process and Budgeting at SBU LevelDocument3 pagesWhat Are Different Types of Strategic Missions at SBU Level How Do These Missions Affect Strategic Planning Process and Budgeting at SBU LevelMAHENDRA SHIVAJI DHENAKPas encore d'évaluation

- The Marketing Mix (The 4 P'S of Marketing) : American Marketing Association E. Jerome MccarthyDocument10 pagesThe Marketing Mix (The 4 P'S of Marketing) : American Marketing Association E. Jerome MccarthypreetgodanPas encore d'évaluation

- Consumer Buying ProcessDocument6 pagesConsumer Buying ProcessMAHENDRA SHIVAJI DHENAKPas encore d'évaluation

- The Extended Marketing MixDocument6 pagesThe Extended Marketing MixMAHENDRA SHIVAJI DHENAK50% (2)

- The Service SystemDocument1 pageThe Service SystemMAHENDRA SHIVAJI DHENAKPas encore d'évaluation

- Theories of EntrepreneurshipDocument4 pagesTheories of EntrepreneurshipMAHENDRA SHIVAJI DHENAKPas encore d'évaluation

- Presentation On MCSDocument20 pagesPresentation On MCSMAHENDRA SHIVAJI DHENAKPas encore d'évaluation

- Q.5. A) Describe The Inherent Difficulties Creation of Profit Centers May Cause and Advantages PossibleDocument2 pagesQ.5. A) Describe The Inherent Difficulties Creation of Profit Centers May Cause and Advantages PossibleMAHENDRA SHIVAJI DHENAKPas encore d'évaluation

- Profit CenterDocument3 pagesProfit CenterMAHENDRA SHIVAJI DHENAKPas encore d'évaluation

- Generated by Unregistered Batch DOC & DOCX Converter 2010.2.406.1388, Please Register! Management Control SystemDocument23 pagesGenerated by Unregistered Batch DOC & DOCX Converter 2010.2.406.1388, Please Register! Management Control SystemMAHENDRA SHIVAJI DHENAKPas encore d'évaluation

- 2003 Management-Control-SystemDocument11 pages2003 Management-Control-SystemMAHENDRA SHIVAJI DHENAKPas encore d'évaluation

- Management Control in Matrix StructuresDocument2 pagesManagement Control in Matrix StructuresMAHENDRA SHIVAJI DHENAK100% (1)

- Assignment 6 Envt. MGTDocument3 pagesAssignment 6 Envt. MGTMAHENDRA SHIVAJI DHENAKPas encore d'évaluation

- Importance of Entrepreneurship in Developed EconomyDocument8 pagesImportance of Entrepreneurship in Developed EconomyMAHENDRA SHIVAJI DHENAK50% (2)

- Factors Affecting Entrepreneurial GrowthDocument6 pagesFactors Affecting Entrepreneurial GrowthMAHENDRA SHIVAJI DHENAK91% (45)

- Stages of Evolution of EntrepreneurshipDocument2 pagesStages of Evolution of EntrepreneurshipMAHENDRA SHIVAJI DHENAK69% (35)

- The Entrepreneurial ProcessDocument2 pagesThe Entrepreneurial ProcessMAHENDRA SHIVAJI DHENAK50% (2)

- Functions of An EntrepreneurDocument2 pagesFunctions of An EntrepreneurMAHENDRA SHIVAJI DHENAK96% (24)

- Skills Required For Being An EntrepreneurDocument4 pagesSkills Required For Being An EntrepreneurMAHENDRA SHIVAJI DHENAKPas encore d'évaluation

- Meaning, Def .,feature of EntreprenurDocument5 pagesMeaning, Def .,feature of EntreprenurMAHENDRA SHIVAJI DHENAKPas encore d'évaluation

- Types of EntrepreneursDocument3 pagesTypes of EntrepreneursMAHENDRA SHIVAJI DHENAK50% (2)

- Online StatementDocument6 pagesOnline StatementЮлия П100% (2)

- Wk1 Wk2 Wk3 Wk4 Wk5 Wk6 Wk7 Wk8 Wk9 Wk10 Wk11 Wk12Document12 pagesWk1 Wk2 Wk3 Wk4 Wk5 Wk6 Wk7 Wk8 Wk9 Wk10 Wk11 Wk12waxkale igadhehPas encore d'évaluation

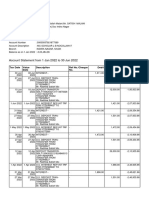

- Account Statement UnlockedDocument12 pagesAccount Statement UnlockedDeepePas encore d'évaluation

- Intra-EEA Fallback POS Interchange FeesDocument4 pagesIntra-EEA Fallback POS Interchange FeesStefano Micautolalaner GrgićPas encore d'évaluation

- Alamat Dollar BitcoinDocument4 pagesAlamat Dollar BitcoinBuru DollarPas encore d'évaluation

- Saved Message Center Message 13Document2 pagesSaved Message Center Message 13Clinton AndersonPas encore d'évaluation

- PDFDocument1 pagePDFKumar SamyappanPas encore d'évaluation

- XXXXXXX 1029Document18 pagesXXXXXXX 1029Jamaluddin GauriPas encore d'évaluation

- WU Transfer Bug PayPal Transfer ATM Clone Plastic Cards Bank Transfer Logs BTC Transfer Cashapp TransferWise ATM Clone Plastic CardsDocument5 pagesWU Transfer Bug PayPal Transfer ATM Clone Plastic Cards Bank Transfer Logs BTC Transfer Cashapp TransferWise ATM Clone Plastic CardsAlbert G100% (8)

- Recent SbiDocument13 pagesRecent SbiSunkara ThanmayeesaisowmyaPas encore d'évaluation

- Form For No DuesDocument2 pagesForm For No DuesPrakarsh SaxenaPas encore d'évaluation

- SBI Education Loan StatementDocument2 pagesSBI Education Loan StatementVivek ChandakPas encore d'évaluation

- How To Pay BPDB Bill Through GPAY APP ?Document4 pagesHow To Pay BPDB Bill Through GPAY APP ?SUNNY AHMED RIYADPas encore d'évaluation

- Learn About Refunds On Google Play - Google Play HelpDocument9 pagesLearn About Refunds On Google Play - Google Play HelpLemma Tolessa DadiPas encore d'évaluation

- White Label AtmDocument5 pagesWhite Label AtmAliza SayedPas encore d'évaluation

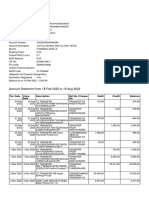

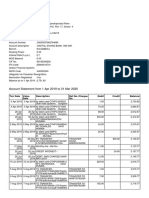

- Account Statement From 1 Apr 2019 To 31 Mar 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument7 pagesAccount Statement From 1 Apr 2019 To 31 Mar 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceawddPas encore d'évaluation

- Payment MethodsDocument3 pagesPayment MethodsAbdo A. El-wafiPas encore d'évaluation

- TransactionSummary 920020060866153 051023033316Document3 pagesTransactionSummary 920020060866153 051023033316gaurav sondhiPas encore d'évaluation

- E-Cash Report CSE SeminarDocument35 pagesE-Cash Report CSE Seminarz1230% (1)

- IATA EasyPay Launch in Serbia For AgentsDocument5 pagesIATA EasyPay Launch in Serbia For AgentsSoko123Pas encore d'évaluation

- Online Banking (Or Internet Banking) Allows Customers To Conduct Financial Transactions OnDocument4 pagesOnline Banking (Or Internet Banking) Allows Customers To Conduct Financial Transactions OnJamshed AlamPas encore d'évaluation

- ITM Skills Academy Digital Payment ModesDocument14 pagesITM Skills Academy Digital Payment Modeschiranjivi bulusuPas encore d'évaluation

- Plastic MoneyDocument15 pagesPlastic MoneyRahulPas encore d'évaluation

- Chapter-5: Findings Summary, Suggestions AND ConclusionDocument7 pagesChapter-5: Findings Summary, Suggestions AND ConclusionPavan Kumar SuralaPas encore d'évaluation

- PNB Dispute Form PDFDocument2 pagesPNB Dispute Form PDFKitol Pepito50% (2)

- Croma Bank Offers - Save More With Exciting Bank Offers - Croma PDFDocument10 pagesCroma Bank Offers - Save More With Exciting Bank Offers - Croma PDFYogesh kuarPas encore d'évaluation

- Certified Vendor ListDocument498 pagesCertified Vendor ListSuhail0% (1)

- 0 0 0 0 94791 SGST (0006)Document2 pages0 0 0 0 94791 SGST (0006)dhavalPas encore d'évaluation

- C YCMd VD6 Ogs Kal 3 HDocument12 pagesC YCMd VD6 Ogs Kal 3 HVishal BawanePas encore d'évaluation

- DBBL StatementDocument1 pageDBBL StatementKazi Foyez Ahmed75% (16)