Vous aimerez peut-être aussi

- Goods and Services Tax (GST) Filing Made Easy: Free Software Literacy SeriesD'EverandGoods and Services Tax (GST) Filing Made Easy: Free Software Literacy SeriesPas encore d'évaluation

- Law Incometaxindia Gov in Dittaxmann Incometaxrules PDF Itr62form16Document3 pagesLaw Incometaxindia Gov in Dittaxmann Incometaxrules PDF Itr62form16api-247505461Pas encore d'évaluation

- Itr 62 Form 16Document4 pagesItr 62 Form 16Hardik ShahPas encore d'évaluation

- 1040 Exam Prep: Module I: The Form 1040 FormulaD'Everand1040 Exam Prep: Module I: The Form 1040 FormulaÉvaluation : 1 sur 5 étoiles1/5 (3)

- Form16fy10 11Document3 pagesForm16fy10 11atishroyPas encore d'évaluation

- Form No. 16: Finotax 1 of 3Document3 pagesForm No. 16: Finotax 1 of 3dugdugdugdugiPas encore d'évaluation

- Form 16 For The AY 2017-18Document4 pagesForm 16 For The AY 2017-18Suman HalderPas encore d'évaluation

- (See Rule 31 (1) (A) ) : Form No. 16Document4 pages(See Rule 31 (1) (A) ) : Form No. 16Ejaj HassanPas encore d'évaluation

- 1040 Exam Prep Module V: Adjustments to Income or DeductionsD'Everand1040 Exam Prep Module V: Adjustments to Income or DeductionsPas encore d'évaluation

- Form 16Document3 pagesForm 16Bijay TiwariPas encore d'évaluation

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionD'EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionPas encore d'évaluation

- (See Rule 31 (1) (A) ) : Form No. 16Document8 pages(See Rule 31 (1) (A) ) : Form No. 16Amol LokhandePas encore d'évaluation

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionD'EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionPas encore d'évaluation

- Form No 16Document4 pagesForm No 16Md ZhidPas encore d'évaluation

- Form No.16: Part ADocument3 pagesForm No.16: Part AYogesh DhekalePas encore d'évaluation

- Form 16, Tax Deduction at Source... Income Tax of IndiaDocument2 pagesForm 16, Tax Deduction at Source... Income Tax of IndiaDrAnilkesar GohilPas encore d'évaluation

- Form 16 FormatDocument2 pagesForm 16 FormatParthVanjaraPas encore d'évaluation

- Bar Review Companion: Taxation: Anvil Law Books Series, #4D'EverandBar Review Companion: Taxation: Anvil Law Books Series, #4Pas encore d'évaluation

- New Form 16 AY 11 12Document4 pagesNew Form 16 AY 11 12Sushma Kaza DuggarajuPas encore d'évaluation

- Cit (TDS) : Emp CodeDocument3 pagesCit (TDS) : Emp CodeMahaveer DhelariyaPas encore d'évaluation

- Gopal G. Trivedi - (108-108) - (2011 - 2012) - Form24Document2 pagesGopal G. Trivedi - (108-108) - (2011 - 2012) - Form24Gopal TrivediPas encore d'évaluation

- Form 16Document6 pagesForm 16Pulkit Gupta100% (1)

- Anspg5953f 2018-19Document3 pagesAnspg5953f 2018-19virajv1Pas encore d'évaluation

- Umesh C-Form16 - 2020-21Document10 pagesUmesh C-Form16 - 2020-21Umesh CPas encore d'évaluation

- Samsung India Electronics Pvt. LTD.: Signature Not VerifiedDocument7 pagesSamsung India Electronics Pvt. LTD.: Signature Not VerifiedGajendra Singh RaghavPas encore d'évaluation

- Form No 16 in Excel With FormuleDocument3 pagesForm No 16 in Excel With FormuleSayal Ji33% (6)

- Form No. 16 (See Rule 31 (1) (A) ) : Certificate Under Section 203 of The Income-Tax Act, 1961 For Tax Deducted at SourceDocument4 pagesForm No. 16 (See Rule 31 (1) (A) ) : Certificate Under Section 203 of The Income-Tax Act, 1961 For Tax Deducted at SourceJeevabinding xeroxPas encore d'évaluation

- (See Rule 37D) : Cit (TDS) Address City Pin Code . .Document2 pages(See Rule 37D) : Cit (TDS) Address City Pin Code . .Akshay RuikarPas encore d'évaluation

- Form27d Applicable From 01.04Document2 pagesForm27d Applicable From 01.04sudhrengePas encore d'évaluation

- Tax Applicable (Tick One) 2 8 1Document7 pagesTax Applicable (Tick One) 2 8 1Gaurav BajajPas encore d'évaluation

- Form No 16Document5 pagesForm No 16Rabiul KhanPas encore d'évaluation

- Form 16Document6 pagesForm 16Ravi DesaiPas encore d'évaluation

- Form 16Document3 pagesForm 16api-247505461Pas encore d'évaluation

- Certificate Under Section 203 of The Income-Tax Act, 1961 For Tax Deducted at Source On SalaryDocument3 pagesCertificate Under Section 203 of The Income-Tax Act, 1961 For Tax Deducted at Source On SalarySvsSridharPas encore d'évaluation

- Form 16 Word FormatDocument4 pagesForm 16 Word FormatVenkee SaiPas encore d'évaluation

- Kaushik Sarkar Form 16 DynProDocument5 pagesKaushik Sarkar Form 16 DynProKaushik SarkarPas encore d'évaluation

- Form 16Document2 pagesForm 16jwadje1Pas encore d'évaluation

- Form 16Document2 pagesForm 16Hari Krishnan ElangovanPas encore d'évaluation

- Form No. 16: Details of Salary Paid and Any Other Income and Tax DeductedDocument2 pagesForm No. 16: Details of Salary Paid and Any Other Income and Tax DeductedSundaresan ChockalingamPas encore d'évaluation

- Form 16 2020 21Document6 pagesForm 16 2020 21Manoj MahimkarPas encore d'évaluation

- Summary of Tax Deducted at Source: TotalDocument2 pagesSummary of Tax Deducted at Source: Totaladithya604Pas encore d'évaluation

- Form 16Document4 pagesForm 16Aruna Kadge JhaPas encore d'évaluation

- Form 16Document2 pagesForm 16Mithun KumarPas encore d'évaluation

- Form 16Document4 pagesForm 16neel721507Pas encore d'évaluation

- Form ITR-1Document3 pagesForm ITR-1Rajeev PuthuparambilPas encore d'évaluation

- Nidhi Form 16 UpdateDocument3 pagesNidhi Form 16 UpdateAbhinav NigamPas encore d'évaluation

- Shashank Kantheti Hyd 12 13Document5 pagesShashank Kantheti Hyd 12 13kshashankPas encore d'évaluation

- Form2FandInstructions 06062006Document11 pagesForm2FandInstructions 06062006Mnaoj PatelPas encore d'évaluation

- Form 16Document3 pagesForm 16tid_scribdPas encore d'évaluation

- A SimDocument4 pagesA Simsana_rautPas encore d'évaluation

- ITR62 Form 15 CADocument5 pagesITR62 Form 15 CAMohit47Pas encore d'évaluation

- 103497Document5 pages103497Ashok PuttaparthyPas encore d'évaluation

- Case Study - 7HR001Document9 pagesCase Study - 7HR001Jehan Jacob FernandoPas encore d'évaluation

- Customer Service Center Manager in Chicago IL Resume Mark HardyDocument2 pagesCustomer Service Center Manager in Chicago IL Resume Mark HardyMarkHardy2Pas encore d'évaluation

- Lecture Non Teaching StaffDocument2 pagesLecture Non Teaching StaffJoyce Ann RamirezPas encore d'évaluation

- Safety Health Manager in North America Resume Gerald DeschaineDocument3 pagesSafety Health Manager in North America Resume Gerald DeschaineGeraldDeschainePas encore d'évaluation

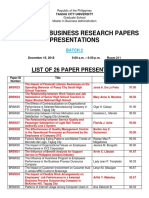

- List of Paper Presenters Tcu Mba 2018 - Batch 2Document2 pagesList of Paper Presenters Tcu Mba 2018 - Batch 2api-194241825100% (1)

- Oolite Inds and Central States Pension Fund 6-23-87Document46 pagesOolite Inds and Central States Pension Fund 6-23-87E Frank CorneliusPas encore d'évaluation

- Harmonic MeanDocument14 pagesHarmonic MeanPolice stationPas encore d'évaluation

- A Project Report On ATTRITION MANAGEMENT PDFDocument120 pagesA Project Report On ATTRITION MANAGEMENT PDFFebson Lee MathewPas encore d'évaluation

- SLB Land Rig BRDocument9 pagesSLB Land Rig BRIkhwan100% (1)

- Wage ConceptsDocument4 pagesWage ConceptsSankalp Jain100% (1)

- Effect of Performance Incentives On Employee Efficiency in Reliance Mart - BangaloreDocument128 pagesEffect of Performance Incentives On Employee Efficiency in Reliance Mart - BangaloreRaja kamal ChPas encore d'évaluation

- Space Planning ReportDocument11 pagesSpace Planning Reportanon283Pas encore d'évaluation

- As A Manager of XYZ OrganizationDocument1 pageAs A Manager of XYZ Organizationshariq ahmedPas encore d'évaluation

- CH14 7edDocument34 pagesCH14 7edgafulugenciaPas encore d'évaluation

- Hostile Work EnvironmentDocument6 pagesHostile Work EnvironmentKarugendo0% (1)

- DO 73-05 TB PreventionDocument5 pagesDO 73-05 TB PreventionMark Rusiana100% (1)

- (G.R. No. 158637 April 12, 2006) Maricalum Mining Corporation, Petitioner, vs. Antonio Decorion, RespondentDocument3 pages(G.R. No. 158637 April 12, 2006) Maricalum Mining Corporation, Petitioner, vs. Antonio Decorion, RespondentMonica May RamosPas encore d'évaluation

- Coordination and SupervisionDocument42 pagesCoordination and Supervisionpriya chauhanPas encore d'évaluation

- Q & A LaborDocument5 pagesQ & A Labormamp05100% (1)

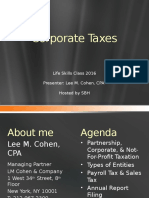

- Corporate Taxes - Life Skills 2016 1Document16 pagesCorporate Taxes - Life Skills 2016 1api-337655281Pas encore d'évaluation

- ME180 Preliminary Report Pagbilao Power StationDocument15 pagesME180 Preliminary Report Pagbilao Power StationMark Christian LiwagPas encore d'évaluation

- Act Relating To Holidays (Norway)Document14 pagesAct Relating To Holidays (Norway)AnaLuManolePas encore d'évaluation

- 1940 Census Extraction FormsDocument6 pages1940 Census Extraction FormsEutychus2ndPas encore d'évaluation

- St. Mary'S University School of Graduate StudiesDocument68 pagesSt. Mary'S University School of Graduate StudiesAnonymous SmT3KnPas encore d'évaluation

- 2014 Pharmaceutical Salary SurveyDocument64 pages2014 Pharmaceutical Salary SurveyClinical Professionals Ltd100% (1)

- Integration Between SAP HR Sub ModulesDocument3 pagesIntegration Between SAP HR Sub ModulesAditya DeshpandePas encore d'évaluation

- Issues Between Organizations and Individuals (TYWIN)Document15 pagesIssues Between Organizations and Individuals (TYWIN)张智100% (1)

- Workman Compensation Act: Presented By: Laxmi Sagar Rout Soumya Tripathy Mary Sumita BaraDocument31 pagesWorkman Compensation Act: Presented By: Laxmi Sagar Rout Soumya Tripathy Mary Sumita BaraLaxmi Sagar RoutPas encore d'évaluation

- CS Form No. 1 Appointment Transmittal and Action FormDocument4 pagesCS Form No. 1 Appointment Transmittal and Action FormDeejay Rubio OpelacPas encore d'évaluation

- Job EvaluationDocument28 pagesJob Evaluationld_ganeshPas encore d'évaluation