Vous aimerez peut-être aussi

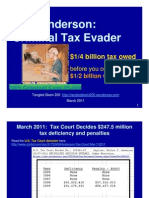

- Walt Anderson - Criminal Tax Evader March 2011Document15 pagesWalt Anderson - Criminal Tax Evader March 2011tangledskein200Pas encore d'évaluation

- Cambria Doc Opp To Detention 4 LaceyDocument19 pagesCambria Doc Opp To Detention 4 LaceyStephen LemonsPas encore d'évaluation

- Sylvia Atkinson Federal IndictmentDocument10 pagesSylvia Atkinson Federal IndictmentEl Paso Times100% (1)

- Sandra BullockDocument12 pagesSandra BullockEriq GardnerPas encore d'évaluation

- Boxx AnswerDocument32 pagesBoxx AnswerKenan FarrellPas encore d'évaluation

- Referencing Ruelas PieceDocument21 pagesReferencing Ruelas PieceStephen LemonsPas encore d'évaluation

- Stewart V Apple ComplaintDocument5 pagesStewart V Apple ComplaintEric GoldmanPas encore d'évaluation

- Tamara Favazza v. Joe Francis and Girls Gone WildDocument28 pagesTamara Favazza v. Joe Francis and Girls Gone WildChad Garrison0% (1)

- DWB Fintext-1 1Document372 pagesDWB Fintext-1 1taibiscutePas encore d'évaluation

- Frost Gang ReportDocument10 pagesFrost Gang ReportLee PedersonPas encore d'évaluation

- Who Was Howard Bowles Talking To On 26 Feb 2015 Australian Time, Mastercardantitrust-HearingtranscriptDocument62 pagesWho Was Howard Bowles Talking To On 26 Feb 2015 Australian Time, Mastercardantitrust-HearingtranscriptSenateBriberyInquiryPas encore d'évaluation

- Aud Marie Wendy MC Lean 6Mc A108095-05Document3 pagesAud Marie Wendy MC Lean 6Mc A108095-05Kym LatoyPas encore d'évaluation

- 20221203-Mr G. H. Schorel-Hlavka O.W.B. To R Kershaw Chief Commissioner of AFP-Suppl 93 - Part 5 - Electors-Candidates-Covid Scam, EtcDocument34 pages20221203-Mr G. H. Schorel-Hlavka O.W.B. To R Kershaw Chief Commissioner of AFP-Suppl 93 - Part 5 - Electors-Candidates-Covid Scam, EtcGerrit Hendrik Schorel-HlavkaPas encore d'évaluation

- The Sink: Crime, Terror and Dirty Money in the Offshore WorldD'EverandThe Sink: Crime, Terror and Dirty Money in the Offshore WorldPas encore d'évaluation

- The Blue And Silver Shark: A Biker's Story (Book 5 of the Series)D'EverandThe Blue And Silver Shark: A Biker's Story (Book 5 of the Series)Pas encore d'évaluation

- Berlin Dossier On ChandlersDocument192 pagesBerlin Dossier On ChandlersJim Hoft100% (1)

- The Dirty Deeds of Silicon Valley Volume TwoDocument382 pagesThe Dirty Deeds of Silicon Valley Volume TwoSCRIBD444100% (2)

- Doc. 36 - First Amended ComplaintDocument222 pagesDoc. 36 - First Amended ComplaintR. Lance FloresPas encore d'évaluation

- 20230916-Schorel-Hlavka O.W.B. To Buloke Shire Council & OrsDocument33 pages20230916-Schorel-Hlavka O.W.B. To Buloke Shire Council & OrsGerrit Hendrik Schorel-HlavkaPas encore d'évaluation

- The Greatest Texas Bank Job: Felonious Balonias - ToxiczombiedevelopmentsDocument4 pagesThe Greatest Texas Bank Job: Felonious Balonias - ToxiczombiedevelopmentsBaqi-Khaliq BeyPas encore d'évaluation

- 20211121-Mr G. H. Schorel-Hlavka O.W.B. To R Kershaw Chief Commissioner of The Australian Federal Police-Suppl - 33 VICTIM or AGGRESSORDocument54 pages20211121-Mr G. H. Schorel-Hlavka O.W.B. To R Kershaw Chief Commissioner of The Australian Federal Police-Suppl - 33 VICTIM or AGGRESSORGerrit Hendrik Schorel-HlavkaPas encore d'évaluation

- TRIAL by DECLARATION: SEATBELT CITATION's ARE UNCONSTITUTIONAL B/C They Are A MEDICAL DEVICE & NO RELIGIOUS EXEMPTION IS ALLOWEDDocument24 pagesTRIAL by DECLARATION: SEATBELT CITATION's ARE UNCONSTITUTIONAL B/C They Are A MEDICAL DEVICE & NO RELIGIOUS EXEMPTION IS ALLOWEDVan Der KokPas encore d'évaluation

- Imputación Contra M. LustgartenDocument30 pagesImputación Contra M. LustgartenArmandoInfoPas encore d'évaluation

- The Jere Beasley Report Nov. 2004Document52 pagesThe Jere Beasley Report Nov. 2004Beasley AllenPas encore d'évaluation

- 1stAmd'Cmplnt RICO - Complaint - ECFDocument222 pages1stAmd'Cmplnt RICO - Complaint - ECFR. Lance FloresPas encore d'évaluation

- 20230912-Mr G. H. Schorel-Hlavka O.W.B. To Banyule City Council Mayor CR Castaldo and Ors-TRESPASS, Etc-Supplement 1Document35 pages20230912-Mr G. H. Schorel-Hlavka O.W.B. To Banyule City Council Mayor CR Castaldo and Ors-TRESPASS, Etc-Supplement 1Gerrit Hendrik Schorel-HlavkaPas encore d'évaluation

- Con Men: Fascinating Profiles of Swindlers and Rogues from the Files of the Most Successful Broadcast in Television HistoryD'EverandCon Men: Fascinating Profiles of Swindlers and Rogues from the Files of the Most Successful Broadcast in Television HistoryÉvaluation : 2.5 sur 5 étoiles2.5/5 (4)

- Usa Inc. Bankrupt - No More Irs! Where's Potus - The Marshall ReportDocument10 pagesUsa Inc. Bankrupt - No More Irs! Where's Potus - The Marshall ReportJohn SutphinPas encore d'évaluation

- Rogue Corporations: Inside Australia’s biggest business scandalsD'EverandRogue Corporations: Inside Australia’s biggest business scandalsPas encore d'évaluation

- Maverick Ministries To The Legal Services Board Victoria AustraliaDocument11 pagesMaverick Ministries To The Legal Services Board Victoria AustraliaSenateBriberyInquiryPas encore d'évaluation

- The Dirty Deeds of Silicon ValleyDocument227 pagesThe Dirty Deeds of Silicon ValleySCRIBD444100% (1)

- Senate Hearing, 114TH Congress - Protecting Taxpayers From Schemes and Scams During The 2015 Tax Filing SeasonDocument56 pagesSenate Hearing, 114TH Congress - Protecting Taxpayers From Schemes and Scams During The 2015 Tax Filing SeasonScribd Government DocsPas encore d'évaluation

- Joel Stallworth, Tamiya Dickerson, Et Al., Nike Retail Services, Inc.Document45 pagesJoel Stallworth, Tamiya Dickerson, Et Al., Nike Retail Services, Inc.The Fashion LawPas encore d'évaluation

- T4 B12 Winer - National Money FDR - Entire Contents - 9-26-01 Jonathan M Winer Senate Banking Testimony - 1st PG Scanned For Reference 028Document1 pageT4 B12 Winer - National Money FDR - Entire Contents - 9-26-01 Jonathan M Winer Senate Banking Testimony - 1st PG Scanned For Reference 0289/11 Document ArchivePas encore d'évaluation

- Writing Sample - Appellate Brief LRW2Document15 pagesWriting Sample - Appellate Brief LRW2Ramin RajaiiPas encore d'évaluation

- Networks Authorized User List (NAUL) : November 2021Document24 pagesNetworks Authorized User List (NAUL) : November 2021Harish HashPas encore d'évaluation

- 252 - U.S. Treasury Forclosing On The Federal Reserve BankDocument2 pages252 - U.S. Treasury Forclosing On The Federal Reserve BankDavid E Robinson100% (6)

- 01 Alegaciones 1993 ChandlerDocument24 pages01 Alegaciones 1993 ChandlerJose Miguel ReyPas encore d'évaluation

- Citizens ArrestDocument1 pageCitizens Arresttrinadadwarlock666Pas encore d'évaluation

- I Am Seeing My Work in The News and I Know We Are Getting Our THERAPY CAMPS REAL SOON - You Cannot Make This Up!Document250 pagesI Am Seeing My Work in The News and I Know We Are Getting Our THERAPY CAMPS REAL SOON - You Cannot Make This Up!Sue BozgozPas encore d'évaluation

- RULWA Claim Against Munsters Corn MazeDocument3 pagesRULWA Claim Against Munsters Corn MazeShauna Pryer-WhitePas encore d'évaluation

- Matters of Life and Data: The Remarkable Journey of a Big Data Visionary Whose Work Impacted Millions (Including You)D'EverandMatters of Life and Data: The Remarkable Journey of a Big Data Visionary Whose Work Impacted Millions (Including You)Pas encore d'évaluation

- Searching For My Identity (Vol 2): The Chronological Evolution Of An Outlaw Biker On The Road To Redemption: Searching For My IdentityD'EverandSearching For My Identity (Vol 2): The Chronological Evolution Of An Outlaw Biker On The Road To Redemption: Searching For My IdentityPas encore d'évaluation

- Case 1:20-cv-02342-LKG Document 1 Filed 08/13/20 Page 1 of 36Document36 pagesCase 1:20-cv-02342-LKG Document 1 Filed 08/13/20 Page 1 of 36Ethan BrownPas encore d'évaluation

- Amended Complaint in SEPTA vs. Orrstown Bank in U.S. District Court, Pa. Middle DistrictDocument190 pagesAmended Complaint in SEPTA vs. Orrstown Bank in U.S. District Court, Pa. Middle DistrictFranklin OpinionPas encore d'évaluation

- 1 Robert As A Jag Officer LJ Former DCDocument624 pages1 Robert As A Jag Officer LJ Former DCadaadvocatesuebozgozPas encore d'évaluation

- We Control The World's Wealth Twitter1.2.19Document19 pagesWe Control The World's Wealth Twitter1.2.19karen hudesPas encore d'évaluation

- Epstein ImagesDocument29 pagesEpstein ImagesJames LynchPas encore d'évaluation

- August 23,2012 EditionDocument12 pagesAugust 23,2012 EditionThe Emerald Star NewsPas encore d'évaluation

- Federal Lawsuit Finally Gives Steve Aubrey and Brian Vodicka A Voice.Document229 pagesFederal Lawsuit Finally Gives Steve Aubrey and Brian Vodicka A Voice.Steve AubreyPas encore d'évaluation

- In The Name of God Most Gracious Most MercifulDocument124 pagesIn The Name of God Most Gracious Most MercifulSUPREME TRIBUNAL OF THE JURISPas encore d'évaluation

- In The Name of God Most Gracious Most MercifulDocument124 pagesIn The Name of God Most Gracious Most MercifulSUPREME TRIBUNAL OF THE JURISPas encore d'évaluation

- 201306REM Report PrivacyDocument24 pages201306REM Report PrivacyAlistairPas encore d'évaluation

- Josh Johnson Complaint For Copyright Infringement and Providing False Copyright Management InformationDocument10 pagesJosh Johnson Complaint For Copyright Infringement and Providing False Copyright Management InformationSchneider Rothman IP Law GroupPas encore d'évaluation

- Walt Anderson Tax Evader On CNBC 9 PM April 14 2011Document20 pagesWalt Anderson Tax Evader On CNBC 9 PM April 14 2011tangledskein200Pas encore d'évaluation

- In Anderson Case, Uneasy Role For Firms - Legal Times 2005Document4 pagesIn Anderson Case, Uneasy Role For Firms - Legal Times 2005tangledskein200Pas encore d'évaluation

- Anderson Tax Court Mar 7 2011Document2 pagesAnderson Tax Court Mar 7 2011tangledskein200Pas encore d'évaluation

- Bankruptcy Docket 05-00775 DOCKET 35 Pages 2010Document34 pagesBankruptcy Docket 05-00775 DOCKET 35 Pages 2010tangledskein200Pas encore d'évaluation

- US Internal Revenue Service: Metest040505Document19 pagesUS Internal Revenue Service: Metest040505IRSPas encore d'évaluation

- WHERE Is This "Smaller World" Trust Entity Described in SEC Filings ? - QuestionDocument1 pageWHERE Is This "Smaller World" Trust Entity Described in SEC Filings ? - Questiontangledskein200Pas encore d'évaluation

- IRC 4942-g Qualifying Distributions - 1988 Cured Delay in Benefit To Charity TRA69 IssueDocument22 pagesIRC 4942-g Qualifying Distributions - 1988 Cured Delay in Benefit To Charity TRA69 Issuetangledskein200Pas encore d'évaluation

- WHERE Is This "Smaller World" Trust Entity Described in SEC Filings ? - QuestionDocument1 pageWHERE Is This "Smaller World" Trust Entity Described in SEC Filings ? - Questiontangledskein200Pas encore d'évaluation

- Tax Court 20364-07 May 12 2010 OrderDocument2 pagesTax Court 20364-07 May 12 2010 Ordertangledskein200Pas encore d'évaluation

- About Alternative Dispute ResolutionDocument9 pagesAbout Alternative Dispute ResolutionLykah HonraPas encore d'évaluation

- 21-04-12 Samsung Reply BriefDocument45 pages21-04-12 Samsung Reply BriefFlorian MuellerPas encore d'évaluation

- Thos. D. Aitken For Appellant. Modesto Reyes and Eliseo Ymzon For AppelleesDocument42 pagesThos. D. Aitken For Appellant. Modesto Reyes and Eliseo Ymzon For AppelleesEm AlayzaPas encore d'évaluation

- CPC CaseDocument4 pagesCPC CaseNidhi RaiPas encore d'évaluation

- Adr AssignmentDocument16 pagesAdr AssignmentInaz IdPas encore d'évaluation

- Guidelines Implementing Rules of Dangerous Drugs ActDocument10 pagesGuidelines Implementing Rules of Dangerous Drugs ActKerwin LeonidaPas encore d'évaluation

- Rule 111 - JM Dominguez v. Liclican (DIGEST)Document1 pageRule 111 - JM Dominguez v. Liclican (DIGEST)Antonio Salvador0% (1)

- People Vs MedrosoDocument4 pagesPeople Vs MedrosoJun JunPas encore d'évaluation

- Alonte Vs PeopleDocument54 pagesAlonte Vs PeopleCes YlayaPas encore d'évaluation

- Case Digest Legal Prof - Last Cases Starting From Tanada V CADocument18 pagesCase Digest Legal Prof - Last Cases Starting From Tanada V CAIamtheLaughingmanPas encore d'évaluation

- Alonzo v. Padua, G.R. No. 72873. May 28, 1987Document3 pagesAlonzo v. Padua, G.R. No. 72873. May 28, 1987Rodolfo TobiasPas encore d'évaluation

- Petitioner Respondents: Nicanor Somodio, Court of Appeals, Ebenecer Purisima and Felomino AycoDocument6 pagesPetitioner Respondents: Nicanor Somodio, Court of Appeals, Ebenecer Purisima and Felomino AycoSamuel ValladoresPas encore d'évaluation

- IBP ruling on lawyer drafting release orderDocument62 pagesIBP ruling on lawyer drafting release orderMelissaRoseMolinaPas encore d'évaluation

- Avelino v. Cuenco (G.R. No. L-2821)Document2 pagesAvelino v. Cuenco (G.R. No. L-2821)Roward67% (3)

- G.R. No. L-1276 April 30, 1948Document3 pagesG.R. No. L-1276 April 30, 1948Tovy BordadoPas encore d'évaluation

- 2 Gachon vs. de VeraDocument3 pages2 Gachon vs. de VeraMutyaAlmodienteCocjinPas encore d'évaluation

- MCQ - CPC ReseachDocument50 pagesMCQ - CPC ReseachSushil BaranwalPas encore d'évaluation

- This Product Is Licensed To Hard Soni, Advocate,, AhmedabadDocument6 pagesThis Product Is Licensed To Hard Soni, Advocate,, AhmedabadHard SoniPas encore d'évaluation

- Teng v. PahagacDocument13 pagesTeng v. PahagacJoe RealPas encore d'évaluation

- Occupational Health and Safety Act Free QuizDocument2 pagesOccupational Health and Safety Act Free QuizQuiz Ontario100% (2)

- Cases ObliconDocument52 pagesCases ObliconDon SumiogPas encore d'évaluation

- Correct Your Status The American States AssemblyDocument13 pagesCorrect Your Status The American States Assemblymballbuster208Pas encore d'évaluation

- Law of SuccessionDocument9 pagesLaw of Successiondivyasoni2511100% (1)

- UPDATED 07a TOM Remedial Law Bar Reviewer IDocument598 pagesUPDATED 07a TOM Remedial Law Bar Reviewer IJose Rolly GonzagaPas encore d'évaluation

- Representation of Government Officials by Private CounselDocument7 pagesRepresentation of Government Officials by Private CounselBon HartPas encore d'évaluation

- COMELEC Resolution No. 9922 and Extended Warranty Contract NullifiedDocument4 pagesCOMELEC Resolution No. 9922 and Extended Warranty Contract NullifiedEliePas encore d'évaluation

- PCGG Agreements Lack Legal BasisDocument30 pagesPCGG Agreements Lack Legal BasisviviviolettePas encore d'évaluation

- SC Dismisses Petition Challenging Issuance of Letters Testamentary to Marcos RespondentsDocument9 pagesSC Dismisses Petition Challenging Issuance of Letters Testamentary to Marcos RespondentsNikkiAndradePas encore d'évaluation

- Vera v. Avelino, G.R. No. L-543, 31 August 1946Document162 pagesVera v. Avelino, G.R. No. L-543, 31 August 1946Kate Del PradoPas encore d'évaluation

- January 2014 Philippine Supreme Court Rulings on Political and Commercial LawDocument84 pagesJanuary 2014 Philippine Supreme Court Rulings on Political and Commercial LawBernadette PaladPas encore d'évaluation