Vous aimerez peut-être aussi

- Module 13 - Intangible AssetsDocument13 pagesModule 13 - Intangible AssetsJehPoyPas encore d'évaluation

- MODULE 4 Relevant CostingDocument9 pagesMODULE 4 Relevant Costingsharielles /Pas encore d'évaluation

- AFAR - Revenue Recognition, JointDocument3 pagesAFAR - Revenue Recognition, JointJoanna Rose DeciarPas encore d'évaluation

- Compre Audit Cieloflawless Q PDFDocument3 pagesCompre Audit Cieloflawless Q PDFCarina Mae Valdez ValenciaPas encore d'évaluation

- Quiz - Intangible Assets With QuestionsDocument3 pagesQuiz - Intangible Assets With Questionsjanus lopezPas encore d'évaluation

- 1911 Investments Investment in Associate and Bond InvestmentDocument13 pages1911 Investments Investment in Associate and Bond InvestmentCykee Hanna Quizo LumongsodPas encore d'évaluation

- Business CombinationDocument3 pagesBusiness CombinationJia CruzPas encore d'évaluation

- Pre Week NewDocument30 pagesPre Week NewAnonymous wDganZPas encore d'évaluation

- Jamolod - Unit 1 - General Features of Financial StatementDocument8 pagesJamolod - Unit 1 - General Features of Financial StatementJatha JamolodPas encore d'évaluation

- Franchise AccountingDocument2 pagesFranchise AccountingChristopher NogotPas encore d'évaluation

- Audit of IntangiblesDocument2 pagesAudit of IntangiblesJaycee FabriagPas encore d'évaluation

- Benjo Lopez CoDocument2 pagesBenjo Lopez Conovy0% (1)

- Colegio de La Purisima Concepcion: School of The Archdiocese of Capiz Roxas CityDocument5 pagesColegio de La Purisima Concepcion: School of The Archdiocese of Capiz Roxas CityJhomel Domingo GalvezPas encore d'évaluation

- Theories: Far Eastern University - Manila Quiz No. 1Document6 pagesTheories: Far Eastern University - Manila Quiz No. 1Kenneth Christian WilburPas encore d'évaluation

- ADV2 Chapter12 QADocument4 pagesADV2 Chapter12 QAMa Alyssa DelmiguezPas encore d'évaluation

- Module 1 Home Office and Branch Accounting General ProceduresDocument4 pagesModule 1 Home Office and Branch Accounting General ProceduresDaenielle EspinozaPas encore d'évaluation

- AFAR BOOKLET 2 AutoRecovered AutoRecoveredDocument222 pagesAFAR BOOKLET 2 AutoRecovered AutoRecoveredEmey CalbayPas encore d'évaluation

- Module 4 Business Combination Date of AcquisitionDocument28 pagesModule 4 Business Combination Date of AcquisitionJulliena BakersPas encore d'évaluation

- DLSA AP Intangibles For DistributionDocument7 pagesDLSA AP Intangibles For DistributionJan Renee EpinoPas encore d'évaluation

- CH 7 AnswersDocument5 pagesCH 7 Answersthenikkitr0% (1)

- Derivatives Qs PDFDocument5 pagesDerivatives Qs PDFLara Camille CelestialPas encore d'évaluation

- JPIA-MCL Academic-EventsDocument17 pagesJPIA-MCL Academic-EventsJana BercasioPas encore d'évaluation

- Special TransactionsDocument5 pagesSpecial TransactionsJehannahBarat100% (1)

- Business Combination.: Pfrs 3Document33 pagesBusiness Combination.: Pfrs 3Reginald Valencia100% (1)

- MODULE 1 2 Bonds PayableDocument10 pagesMODULE 1 2 Bonds PayableFujoshi BeePas encore d'évaluation

- FAR.2850 - Interim Financial Reporting.Document4 pagesFAR.2850 - Interim Financial Reporting.Ashley LegaspiPas encore d'évaluation

- Morales, Jonalyn M.Document7 pagesMorales, Jonalyn M.Jonalyn MoralesPas encore d'évaluation

- P2 - AnswerKeyDocument9 pagesP2 - AnswerKeyoizys131Pas encore d'évaluation

- Advanced Accounting1Document8 pagesAdvanced Accounting1precious mlb100% (1)

- Installment SalesDocument6 pagesInstallment SalesMarivic C. VelascoPas encore d'évaluation

- Auditing Theory Red Sirug Ra 9298 - Philippine Accountancy Act of 2004 (Multiple Choice Questions)Document10 pagesAuditing Theory Red Sirug Ra 9298 - Philippine Accountancy Act of 2004 (Multiple Choice Questions)Jyznareth TapiaPas encore d'évaluation

- P3Document18 pagesP3Rezzan Joy MejiaPas encore d'évaluation

- Equity YyyDocument33 pagesEquity YyyJude SantosPas encore d'évaluation

- Problem 3 LessorDocument7 pagesProblem 3 LessorGelo Owss33% (9)

- Intercompany (Inventories)Document6 pagesIntercompany (Inventories)Ma Hadassa O. FolientePas encore d'évaluation

- Fourth Year - Bsa: University of Makati Set BDocument11 pagesFourth Year - Bsa: University of Makati Set BYedam BangPas encore d'évaluation

- PRTC Olympiad Reg 12Document14 pagesPRTC Olympiad Reg 12Vincent Larrie MoldezPas encore d'évaluation

- Module QuizsDocument24 pagesModule QuizswsviviPas encore d'évaluation

- Abc Stock AcquisitionDocument13 pagesAbc Stock AcquisitionMary Joy AlbandiaPas encore d'évaluation

- Rey Ocampo Online! Auditing Problems: Audit of InvestmentsDocument4 pagesRey Ocampo Online! Auditing Problems: Audit of InvestmentsSchool FilesPas encore d'évaluation

- Accounting 14 - Applied Auditing OkDocument12 pagesAccounting 14 - Applied Auditing OkNico evansPas encore d'évaluation

- Module 7 NPO Colleges and Universities - Ngovacc PDFDocument8 pagesModule 7 NPO Colleges and Universities - Ngovacc PDFvum preePas encore d'évaluation

- Acc 310 - M004Document12 pagesAcc 310 - M004Edward Glenn BaguiPas encore d'évaluation

- ACELEC 332 Prelim Quiz 2Document9 pagesACELEC 332 Prelim Quiz 2MontenegroPas encore d'évaluation

- 162 003Document5 pages162 003Alvin John San Juan33% (3)

- Auditing Problems Intangibles Impairment and Revaluation PDFDocument44 pagesAuditing Problems Intangibles Impairment and Revaluation PDFMark Domingo MendozaPas encore d'évaluation

- Afar 3 Government Accounting and Accounting For Non-Profit Organizations Course OutlineDocument2 pagesAfar 3 Government Accounting and Accounting For Non-Profit Organizations Course OutlineJamaica DavidPas encore d'évaluation

- C18 - Defined Benefit Plan PDFDocument23 pagesC18 - Defined Benefit Plan PDFKristine Diane CABAnASPas encore d'évaluation

- Module 5 Franchise Accounting WADocument4 pagesModule 5 Franchise Accounting WAMadielyn Santarin MirandaPas encore d'évaluation

- 8 FranchiseDocument8 pages8 FranchiseDJAN IHIAZEL DELA CUADRAPas encore d'évaluation

- Afar Franchise Accounting PDFDocument6 pagesAfar Franchise Accounting PDFArah OpalecPas encore d'évaluation

- Franchise QuizDocument2 pagesFranchise QuizCattleyaPas encore d'évaluation

- Module 5 Franchise Sales Assignments 2bac May 2023Document6 pagesModule 5 Franchise Sales Assignments 2bac May 2023Aaron OsmaPas encore d'évaluation

- Franchise (Applied Auditing)Document4 pagesFranchise (Applied Auditing)Abraham Jr. Manansala100% (3)

- FranchisingDocument2 pagesFranchisingMangoStarr Aibelle VegasPas encore d'évaluation

- Franchise Applied AuditingDocument4 pagesFranchise Applied AuditingMariel RascoPas encore d'évaluation

- FranchiseDocument5 pagesFranchiseSunny DaePas encore d'évaluation

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument5 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionErwin Labayog MedinaPas encore d'évaluation

- Final Quiz and SeatworkDocument3 pagesFinal Quiz and SeatworkMikaela SungaPas encore d'évaluation

- Manpower RequirementDocument12 pagesManpower RequirementJose SasPas encore d'évaluation

- Arts and Culture MapehDocument9 pagesArts and Culture MapehJose SasPas encore d'évaluation

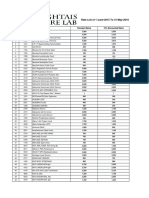

- Fiscal Year Is January-December. All Values PHP MillionsDocument5 pagesFiscal Year Is January-December. All Values PHP MillionsJose SasPas encore d'évaluation

- Logistics 2 (Repaired)Document1 pageLogistics 2 (Repaired)Jose SasPas encore d'évaluation

- Control Matrix - Premiums (PC)Document9 pagesControl Matrix - Premiums (PC)Jose SasPas encore d'évaluation

- Chapter 13 GuerreroDocument40 pagesChapter 13 GuerreroJose Sas100% (2)

- Run Omega Run Lunar Omegaverse Book 5 Shyla Colt All ChapterDocument52 pagesRun Omega Run Lunar Omegaverse Book 5 Shyla Colt All Chapterkate.brown975100% (6)

- Lesson 4Document10 pagesLesson 4Nagiri MuraliPas encore d'évaluation

- MSDS Aradur 2965 PDFDocument9 pagesMSDS Aradur 2965 PDFkamalnandrePas encore d'évaluation

- A Lesson About SpringDocument7 pagesA Lesson About SpringKatjaPas encore d'évaluation

- Brochure - Citadines Flatiron Phnom Penh - EnglishDocument4 pagesBrochure - Citadines Flatiron Phnom Penh - EnglishTix VirakPas encore d'évaluation

- Origami PapiroflexiaDocument6 pagesOrigami PapiroflexiaBraulio RomeroPas encore d'évaluation

- Primbon Command 3GDocument3 pagesPrimbon Command 3GEriska FebriantoPas encore d'évaluation

- 11 Physical Fitness Assessment 1Document40 pages11 Physical Fitness Assessment 1Danilo Sare IIIPas encore d'évaluation

- LightsDocument33 pagesLightsEduardo Almeida SilvaPas encore d'évaluation

- Std9thMathsBridgeCourse (4) (001-040) .MR - enDocument40 pagesStd9thMathsBridgeCourse (4) (001-040) .MR - ensilent gamerPas encore d'évaluation

- X-Ray Radiation and Gamma RadiationDocument13 pagesX-Ray Radiation and Gamma RadiationVence MeraPas encore d'évaluation

- Rate List of 1-June-2015 To 31-May-2016: S.No Code Test Name Standard Rates 15% Discounted RatesDocument25 pagesRate List of 1-June-2015 To 31-May-2016: S.No Code Test Name Standard Rates 15% Discounted RatesMirza BabarPas encore d'évaluation

- Vet CareplanexampleDocument6 pagesVet CareplanexampleAnonymous eJZ5HcPas encore d'évaluation

- 4 TH Sem UG Osmoregulation in Aquatic VertebratesDocument6 pages4 TH Sem UG Osmoregulation in Aquatic VertebratesBasak ShreyaPas encore d'évaluation

- Improving Performance, Proxies, and The Render CacheDocument13 pagesImproving Performance, Proxies, and The Render CacheIOXIRPas encore d'évaluation

- Effect of Toe Treatments On The Fatigue Resistance of Structural Steel WeldsDocument12 pagesEffect of Toe Treatments On The Fatigue Resistance of Structural Steel WeldsVicente Palazzo De MarinoPas encore d'évaluation

- An Analytical Study of Foreign Direct InvestmentDocument19 pagesAn Analytical Study of Foreign Direct InvestmentNeha SachdevaPas encore d'évaluation

- Electrical Inspections: Infrared ThermographyDocument28 pagesElectrical Inspections: Infrared ThermographyManish RajPas encore d'évaluation

- MCA Lab ManualDocument5 pagesMCA Lab ManualV SATYA KISHOREPas encore d'évaluation

- Ncs University System Department of Health Sciences: Discipline (MLT-04) (VIROLOGY &MYCOLOGY)Document5 pagesNcs University System Department of Health Sciences: Discipline (MLT-04) (VIROLOGY &MYCOLOGY)Habib UllahPas encore d'évaluation

- 03N - Top Level View of Computer Function and InterconnectionDocument38 pages03N - Top Level View of Computer Function and InterconnectionDoc TelPas encore d'évaluation

- Grade 7 Information Writing: The Bulldog: A Dog Like No OtherDocument5 pagesGrade 7 Information Writing: The Bulldog: A Dog Like No Otherapi-202727113Pas encore d'évaluation

- Roles and Responsibilities of ASHADocument3 pagesRoles and Responsibilities of ASHAmohanpskohli8310Pas encore d'évaluation

- MPDFDocument5 pagesMPDFRoyalAryansPas encore d'évaluation

- TNM Sites May 2023Document24 pagesTNM Sites May 2023Joseph ChikusePas encore d'évaluation

- I10 Workshop Manual - ADocument292 pagesI10 Workshop Manual - ANorthstartechnology Company82% (11)

- Compaction - AsphaltDocument32 pagesCompaction - Asphaltrskcad100% (1)

- Questions and Answers About Lead in Ceramic Tableware: Contra Costa Health Services / Lead Poisoning Prevention ProjectDocument4 pagesQuestions and Answers About Lead in Ceramic Tableware: Contra Costa Health Services / Lead Poisoning Prevention Projectzorro21072107Pas encore d'évaluation

- BookDocument28 pagesBookFebrian Wardoyo100% (1)

- BS en 6100-3-2 Electromagnetic Compatibility (EMC)Document12 pagesBS en 6100-3-2 Electromagnetic Compatibility (EMC)Arun Jacob CherianPas encore d'évaluation

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamD'EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamPas encore d'évaluation

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialD'EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialPas encore d'évaluation

- The Value of a Whale: On the Illusions of Green CapitalismD'EverandThe Value of a Whale: On the Illusions of Green CapitalismÉvaluation : 5 sur 5 étoiles5/5 (2)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaD'EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaÉvaluation : 3.5 sur 5 étoiles3.5/5 (8)

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthD'EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthÉvaluation : 4 sur 5 étoiles4/5 (20)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSND'Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNÉvaluation : 4.5 sur 5 étoiles4.5/5 (3)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaD'EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (14)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successD'EverandReady, Set, Growth hack:: A beginners guide to growth hacking successÉvaluation : 4.5 sur 5 étoiles4.5/5 (93)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialD'EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialÉvaluation : 4.5 sur 5 étoiles4.5/5 (32)

- Creating Shareholder Value: A Guide For Managers And InvestorsD'EverandCreating Shareholder Value: A Guide For Managers And InvestorsÉvaluation : 4.5 sur 5 étoiles4.5/5 (8)

- An easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyD'EverandAn easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyÉvaluation : 3 sur 5 étoiles3/5 (1)

- Corporate Finance Formulas: A Simple IntroductionD'EverandCorporate Finance Formulas: A Simple IntroductionÉvaluation : 4 sur 5 étoiles4/5 (8)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingD'EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingÉvaluation : 4.5 sur 5 étoiles4.5/5 (17)

- The Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceD'EverandThe Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceÉvaluation : 4 sur 5 étoiles4/5 (1)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisD'EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisÉvaluation : 5 sur 5 étoiles5/5 (6)

- Mastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsD'EverandMastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsÉvaluation : 4.5 sur 5 étoiles4.5/5 (21)

- Value: The Four Cornerstones of Corporate FinanceD'EverandValue: The Four Cornerstones of Corporate FinanceÉvaluation : 5 sur 5 étoiles5/5 (2)

- Product-Led Growth: How to Build a Product That Sells ItselfD'EverandProduct-Led Growth: How to Build a Product That Sells ItselfÉvaluation : 5 sur 5 étoiles5/5 (1)

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorD'EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorPas encore d'évaluation

- Finance Basics (HBR 20-Minute Manager Series)D'EverandFinance Basics (HBR 20-Minute Manager Series)Évaluation : 4.5 sur 5 étoiles4.5/5 (32)

- Financial Leadership for Nonprofit Executives: Guiding Your Organization to Long-Term SuccessD'EverandFinancial Leadership for Nonprofit Executives: Guiding Your Organization to Long-Term SuccessÉvaluation : 4 sur 5 étoiles4/5 (2)

- Mind over Money: The Psychology of Money and How to Use It BetterD'EverandMind over Money: The Psychology of Money and How to Use It BetterÉvaluation : 4 sur 5 étoiles4/5 (24)

- YouTube Marketing: Comprehensive Beginners Guide to Learn YouTube Marketing, Tips & Secrets to Growth Hacking Your Channel and Building Profitable Passive Income Business OnlineD'EverandYouTube Marketing: Comprehensive Beginners Guide to Learn YouTube Marketing, Tips & Secrets to Growth Hacking Your Channel and Building Profitable Passive Income Business OnlineÉvaluation : 4.5 sur 5 étoiles4.5/5 (2)

- The Illusion of Innovation: Escape "Efficiency" and Unleash Radical ProgressD'EverandThe Illusion of Innovation: Escape "Efficiency" and Unleash Radical ProgressPas encore d'évaluation