Vous aimerez peut-être aussi

- Front Office - FormulaSDocument5 pagesFront Office - FormulaSsushanta21100% (1)

- Front Office BudgetingDocument31 pagesFront Office BudgetingOwan Sofwan100% (1)

- Yield Management and ForecastingDocument23 pagesYield Management and ForecastingMandeep KaurPas encore d'évaluation

- Digital Guest Experience: Tools to help hotels to manage and optimize the digital guest experienceD'EverandDigital Guest Experience: Tools to help hotels to manage and optimize the digital guest experiencePas encore d'évaluation

- Revenue Management For DummiesDocument4 pagesRevenue Management For DummiesAna BuduPas encore d'évaluation

- Sem 6 Unit 1 Yield ManagementDocument63 pagesSem 6 Unit 1 Yield ManagementAmaan ShaikhPas encore d'évaluation

- Strategies For Increasing Hotel Room SalesDocument11 pagesStrategies For Increasing Hotel Room SalesKing HiramPas encore d'évaluation

- Elect4 Front OfficeDocument46 pagesElect4 Front OfficeWhine Pechon IliganPas encore d'évaluation

- Hotel Break Even Point PDFDocument6 pagesHotel Break Even Point PDFlau weth100% (1)

- Hotel Management Problems and Solutions For Students.Document9 pagesHotel Management Problems and Solutions For Students.Sam Roger100% (2)

- Sales and MarketingDocument2 pagesSales and MarketingchandaPas encore d'évaluation

- Hosp MarkDocument30 pagesHosp MarkkrishnagetzuPas encore d'évaluation

- FactsheetDocument6 pagesFactsheetsafinditPas encore d'évaluation

- The TajDocument40 pagesThe TajRishendra Singh RathourPas encore d'évaluation

- Front Office DutiesDocument2 pagesFront Office DutiesdianteblakeyPas encore d'évaluation

- Best Practices in Hotel Financial ManagementDocument3 pagesBest Practices in Hotel Financial ManagementDhruv BansalPas encore d'évaluation

- Strategic Management Marketing and Analysis of IHG GroupDocument22 pagesStrategic Management Marketing and Analysis of IHG GroupHarsh wadhwaPas encore d'évaluation

- Comparative Study Between FMCG Sector and Hospitality SectorDocument15 pagesComparative Study Between FMCG Sector and Hospitality SectorpriyaPas encore d'évaluation

- Choice HotelsDocument17 pagesChoice HotelsAmit MisalPas encore d'évaluation

- International Operations Pre-Opening Manual: Training Related InformationDocument25 pagesInternational Operations Pre-Opening Manual: Training Related InformationnelsonretiroPas encore d'évaluation

- Project On Business Hotels: Submitted To: - Submitted ByDocument18 pagesProject On Business Hotels: Submitted To: - Submitted ByVeer CoolBoy0% (1)

- Front Desk WorkDocument17 pagesFront Desk WorkShivnetra RanaPas encore d'évaluation

- A Singh - Hotel Housekeeping-Mc Graw Hill India (2012)Document640 pagesA Singh - Hotel Housekeeping-Mc Graw Hill India (2012)dino leonandriPas encore d'évaluation

- Establishing An Effective Guestroom Lock PolicyDocument4 pagesEstablishing An Effective Guestroom Lock PolicyImee S. YuPas encore d'évaluation

- Terms of Service: 1. Acceptance of Terms of Use, Conditions, Notices and DisclaimersDocument7 pagesTerms of Service: 1. Acceptance of Terms of Use, Conditions, Notices and DisclaimersxnexusPas encore d'évaluation

- How Do Guests Choose A HotelDocument10 pagesHow Do Guests Choose A HotelHazrul ChangminPas encore d'évaluation

- Front Desk Supervisor Job DescriptionDocument7 pagesFront Desk Supervisor Job DescriptionmunyekiPas encore d'évaluation

- Fact Sheet MGM Resorts Seven Point Safety PlanDocument2 pagesFact Sheet MGM Resorts Seven Point Safety PlansusanstapletonPas encore d'évaluation

- Taj Lands End MumbaiDocument26 pagesTaj Lands End Mumbaifrankfcf100% (1)

- Hotel and TourismDocument103 pagesHotel and TourismRahul RajPas encore d'évaluation

- Hotel Operations-1 (Chapter-6)Document14 pagesHotel Operations-1 (Chapter-6)VishnuNarayanan Viswanatha PillaiPas encore d'évaluation

- Chapter 1 The Hospitality Industry and YouDocument31 pagesChapter 1 The Hospitality Industry and Yougeorge theofanousPas encore d'évaluation

- Ratio Analysis For HotelDocument4 pagesRatio Analysis For Hotelwisnu_reza9663100% (1)

- Checkout Settlement GuideDocument11 pagesCheckout Settlement GuideRina FatmasariPas encore d'évaluation

- Habiba Ahsan Muhammad Ali Muhammad Maqbool Sidra Shahid Saleha Afzal Butt Sameer Abdal Malik Zain NoorDocument23 pagesHabiba Ahsan Muhammad Ali Muhammad Maqbool Sidra Shahid Saleha Afzal Butt Sameer Abdal Malik Zain NoorhonestscarryPas encore d'évaluation

- Smiling Holidays Since 1990 .:: 00977 1 4419673 / 4428521 Sister OrganizationsDocument3 pagesSmiling Holidays Since 1990 .:: 00977 1 4419673 / 4428521 Sister OrganizationsSuman Bhattarai100% (1)

- Management: Things To Know AboutDocument28 pagesManagement: Things To Know AboutNataliaPas encore d'évaluation

- Corporate Traveler Hotel Terms GuideDocument3 pagesCorporate Traveler Hotel Terms Guidevickie_sunniePas encore d'évaluation

- FRONT OFFICE TERMINOLOGY AND SERVICESDocument67 pagesFRONT OFFICE TERMINOLOGY AND SERVICESzoltan2011Pas encore d'évaluation

- The Ritz-Carlton's Customer Relationship Management StrategiesDocument11 pagesThe Ritz-Carlton's Customer Relationship Management Strategiesjimmy lecturerPas encore d'évaluation

- ROOMS MANAGEMENT ASSESSMENT REPORTDocument5 pagesROOMS MANAGEMENT ASSESSMENT REPORTSHUBRANSHU SEKHARPas encore d'évaluation

- MIS in Hotel Industry: A Guide to Technology's RoleDocument23 pagesMIS in Hotel Industry: A Guide to Technology's Rolenigam34100% (1)

- Management Consulting Development From Historical Perspective - AftandilyantsDocument9 pagesManagement Consulting Development From Historical Perspective - AftandilyantsVadym AftandilyantsPas encore d'évaluation

- Revpar & Market ShareDocument15 pagesRevpar & Market ShareroyrenaldoPas encore d'évaluation

- Sales and MarketingDocument19 pagesSales and Marketingamar keyzPas encore d'évaluation

- Hotel Business DevelopmentDocument9 pagesHotel Business DevelopmentSuhil PatelPas encore d'évaluation

- Advertising and Sales Promotion StrategyDocument39 pagesAdvertising and Sales Promotion Strategyshivakumar NPas encore d'évaluation

- Measuring The Dinning Experience The Case of Vita NovaDocument16 pagesMeasuring The Dinning Experience The Case of Vita NovaMauricio Zavala100% (1)

- Welcome Letter During Hotel RenovationDocument1 pageWelcome Letter During Hotel RenovationDIAN SAFRIZALPas encore d'évaluation

- So You Want To Go Into Hotel SalesDocument54 pagesSo You Want To Go Into Hotel Salesvanthuannguyen100% (4)

- Hotel Glossary of TermsDocument14 pagesHotel Glossary of Termsmayankjaggi095875Pas encore d'évaluation

- Conventiion HotelDocument40 pagesConventiion HotelJohn PaulPas encore d'évaluation

- Role of hotel reservationDocument3 pagesRole of hotel reservationIndira Ghandhi National Open UniversityPas encore d'évaluation

- The Best Sales and RM Caffeine for HotelsDocument55 pagesThe Best Sales and RM Caffeine for HotelsMihaela WhitneyPas encore d'évaluation

- Vallen Check 2ce Im ch09 PDFDocument6 pagesVallen Check 2ce Im ch09 PDFShweta MathurPas encore d'évaluation

- Role of Room RatesDocument5 pagesRole of Room RatesJonathan JacquezPas encore d'évaluation

- Front Office 3rd Year 5th SemDocument23 pagesFront Office 3rd Year 5th SemJatin RanaPas encore d'évaluation

- Yield ManagementDocument21 pagesYield ManagementBrando ManurungPas encore d'évaluation

- Chapter Eight: Hotel OccupancyDocument7 pagesChapter Eight: Hotel Occupancylioul sileshiPas encore d'évaluation

- Competitive Retail MarketDocument146 pagesCompetitive Retail Marketahmedh_98Pas encore d'évaluation

- Mall Management in India & Revival Strategies For Sick MallsDocument38 pagesMall Management in India & Revival Strategies For Sick Mallspunya.trivedi2003Pas encore d'évaluation

- Goat Farm Feasibility StudyDocument75 pagesGoat Farm Feasibility StudyDaniela Repta86% (7)

- Dubai Insurance Companies1Document39 pagesDubai Insurance Companies1abdulpanasiaPas encore d'évaluation

- TRAPSATUR Company ProfileDocument10 pagesTRAPSATUR Company Profileahmedh_98Pas encore d'évaluation

- Business Model Version 1Document23 pagesBusiness Model Version 1ManivannancPas encore d'évaluation

- Organic DairyDocument2 pagesOrganic Dairyahmedh_98Pas encore d'évaluation

- Managing Risks Drivers PDFDocument214 pagesManaging Risks Drivers PDFahmedh_98Pas encore d'évaluation

- Astmisc169 Research Annual Report AbudhabiDocument11 pagesAstmisc169 Research Annual Report Abudhabiahmedh_98Pas encore d'évaluation

- Practical Guide To Risk Assessment (PWC 2008)Document40 pagesPractical Guide To Risk Assessment (PWC 2008)ducuh80% (5)

- Qatar Review Q1 2016 enDocument6 pagesQatar Review Q1 2016 enahmedh_98Pas encore d'évaluation

- Project Risk Assessment ExamplesDocument10 pagesProject Risk Assessment Examples1094Pas encore d'évaluation

- Revenue Management Manual XotelsDocument65 pagesRevenue Management Manual XotelsElena Andreea MusatPas encore d'évaluation

- TMP LM8DNDocument73 pagesTMP LM8DNahmedh_98Pas encore d'évaluation

- Drinks Survey Under 40 CharactersDocument5 pagesDrinks Survey Under 40 Charactersahmedh_98Pas encore d'évaluation

- Valuation Using Startigic OptionDocument15 pagesValuation Using Startigic Optionahmedh_98Pas encore d'évaluation

- Aniruddh - Knids Green PVT LimitedDocument1 pageAniruddh - Knids Green PVT LimitedAniruddh NaikPas encore d'évaluation

- Om Prakash ResumeDocument3 pagesOm Prakash Resumeomprakashkarn1Pas encore d'évaluation

- Learning Unit 2 Types of Business Letters - Inquiry LetterDocument6 pagesLearning Unit 2 Types of Business Letters - Inquiry Lettercatalina9100wwwPas encore d'évaluation

- Soriano V. Bautista 6 Scra 946 (1962)Document1 pageSoriano V. Bautista 6 Scra 946 (1962)YenPas encore d'évaluation

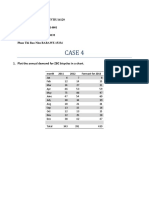

- Case 4: Luyen Ngoc Do Quyen BTFTIU14129 Ngo Khanh Duy BTARIU14601 Pham Gia Huy BTFTIU14132 Phan Thi Bao Nhu BABAWE 15334Document4 pagesCase 4: Luyen Ngoc Do Quyen BTFTIU14129 Ngo Khanh Duy BTARIU14601 Pham Gia Huy BTFTIU14132 Phan Thi Bao Nhu BABAWE 15334HuynhGiangPas encore d'évaluation

- CRM TemplateDocument10 pagesCRM TemplateNipun TantiaPas encore d'évaluation

- Introduction To Sales Management and Its Evolving RolesDocument25 pagesIntroduction To Sales Management and Its Evolving Rolesnazek aliPas encore d'évaluation

- Session 1: Strategic Marketing - Introduction & ScopeDocument38 pagesSession 1: Strategic Marketing - Introduction & ScopeImrul Hasan ChowdhuryPas encore d'évaluation

- Chapter 10 - Vat On Goods 2013Document10 pagesChapter 10 - Vat On Goods 2013roseljoyPas encore d'évaluation

- TD 83 TW SujangarhDocument105 pagesTD 83 TW SujangarhNaveen BishnoiPas encore d'évaluation

- Homework #2: Due: February 1Document6 pagesHomework #2: Due: February 1cvofoxPas encore d'évaluation

- TPS of The Body ShopDocument6 pagesTPS of The Body ShopAashi GargPas encore d'évaluation

- Pasta Restaurant Marketing PlanDocument15 pagesPasta Restaurant Marketing PlanHamad Arif100% (1)

- Writing A Business Plan 20130314Document35 pagesWriting A Business Plan 20130314Mohd FadhilullahPas encore d'évaluation

- Ethics in The MarketplaceDocument19 pagesEthics in The MarketplaceTameem YousafPas encore d'évaluation

- Pidilite Dist FevicolDocument37 pagesPidilite Dist FevicolKULDEEP KAMBLEPas encore d'évaluation

- International Trade FinanceDocument33 pagesInternational Trade Financemesba_17Pas encore d'évaluation

- Sales Career Path - 2019 PDFDocument1 pageSales Career Path - 2019 PDFAnonymous AGbmiyjAkPas encore d'évaluation

- Introduction to Consumption TaxesDocument38 pagesIntroduction to Consumption TaxesGenie Gonzales DimaanoPas encore d'évaluation

- Multiple Organizations Overview - R12: Multi-Org Is Operating UnitsDocument6 pagesMultiple Organizations Overview - R12: Multi-Org Is Operating Unitssudharsan49Pas encore d'évaluation

- Dryousry Hospitality Consulting: Hotel Pre Opening RoadmapDocument35 pagesDryousry Hospitality Consulting: Hotel Pre Opening RoadmapTix VirakPas encore d'évaluation

- Chapter 3 (Kuliah) - Cost Estimation TechniquesDocument32 pagesChapter 3 (Kuliah) - Cost Estimation TechniquesZaki AsyrafPas encore d'évaluation

- Sap Retail Two Step PricingDocument4 pagesSap Retail Two Step PricingShams TabrezPas encore d'évaluation

- Developing New Products and Services: © 2006 Mcgraw-Hill Ryerson Ltd. All Rights ReservedDocument36 pagesDeveloping New Products and Services: © 2006 Mcgraw-Hill Ryerson Ltd. All Rights ReservedSav SinghPas encore d'évaluation

- Performing Strong by Docc HilfordDocument5 pagesPerforming Strong by Docc Hilfordwronged75% (4)

- Quick Progress Test 4Document6 pagesQuick Progress Test 4amPas encore d'évaluation

- MA Tutorial 2Document6 pagesMA Tutorial 2Jia WenPas encore d'évaluation

- Internal Control QuestionnaireDocument3 pagesInternal Control QuestionnaireDyanne Yssabelle DisturaPas encore d'évaluation

- Take Home Quiz 1Document9 pagesTake Home Quiz 1Your MaterialsPas encore d'évaluation

- Creating Custom Context AttributesDocument19 pagesCreating Custom Context AttributesahosainyPas encore d'évaluation