Vous aimerez peut-être aussi

- Elastic NetworksDocument16 pagesElastic NetworksJazzi SehrawatPas encore d'évaluation

- 2015 VERNA Ebrochure 1519269571059Document14 pages2015 VERNA Ebrochure 1519269571059Jazzi SehrawatPas encore d'évaluation

- Audit View Entertainment and Media PDFDocument2 pagesAudit View Entertainment and Media PDFJazzi SehrawatPas encore d'évaluation

- How To Read French Financial Statements PDFDocument4 pagesHow To Read French Financial Statements PDFJazzi SehrawatPas encore d'évaluation

- WagamamaUK Vegan Menu 1017Document2 pagesWagamamaUK Vegan Menu 1017Jazzi SehrawatPas encore d'évaluation

- CR-V Brochure 2016 Apr 17 PDFDocument26 pagesCR-V Brochure 2016 Apr 17 PDFJazzi SehrawatPas encore d'évaluation

- Car Prayers Vahan PujaDocument9 pagesCar Prayers Vahan PujaJazzi SehrawatPas encore d'évaluation

- How To Read French Financial Statements PDFDocument4 pagesHow To Read French Financial Statements PDFJazzi SehrawatPas encore d'évaluation

- Ara 20 F 2016Document203 pagesAra 20 F 2016Jazzi SehrawatPas encore d'évaluation

- Audit View Entertainment and Media PDFDocument2 pagesAudit View Entertainment and Media PDFJazzi SehrawatPas encore d'évaluation

- How To Read French Financial Statements PDFDocument4 pagesHow To Read French Financial Statements PDFJazzi SehrawatPas encore d'évaluation

- How To Read French Financial Statements PDFDocument4 pagesHow To Read French Financial Statements PDFJazzi SehrawatPas encore d'évaluation

- Civic 5 Door Brochure May 16 V1Document24 pagesCivic 5 Door Brochure May 16 V1Jazzi SehrawatPas encore d'évaluation

- CR-V Brochure 2016 Apr 17 PDFDocument26 pagesCR-V Brochure 2016 Apr 17 PDFJazzi SehrawatPas encore d'évaluation

- Nine Trends Transforming Asset ManagementDocument12 pagesNine Trends Transforming Asset ManagementJerry SaksenaPas encore d'évaluation

- Argos Respects Your Privacy. Our Chat Experts Cannot View Your Screen and Will Not Ask For Your Credit Card DetailsDocument1 pageArgos Respects Your Privacy. Our Chat Experts Cannot View Your Screen and Will Not Ask For Your Credit Card DetailsJazzi SehrawatPas encore d'évaluation

- PWC Aifmd Regulatory Brief Impact ManagersDocument3 pagesPWC Aifmd Regulatory Brief Impact ManagersJerry SaksenaPas encore d'évaluation

- Civic 5 Door Brochure May 16 V1Document24 pagesCivic 5 Door Brochure May 16 V1Jazzi SehrawatPas encore d'évaluation

- The Future of Asset ManagementDocument24 pagesThe Future of Asset ManagementJerry SaksenaPas encore d'évaluation

- PWC Top Health Industry Issues of 2014Document17 pagesPWC Top Health Industry Issues of 2014Jin Thaisongsuwan100% (1)

- Distributed Rate Allocation For Inelastic Flows: Prashanth Hande, Shengyu Zhang, and Mung Chiang, Member, IEEEDocument14 pagesDistributed Rate Allocation For Inelastic Flows: Prashanth Hande, Shengyu Zhang, and Mung Chiang, Member, IEEEJazzi SehrawatPas encore d'évaluation

- TV Chathistory 2015-02-25 11.37.15Document1 pageTV Chathistory 2015-02-25 11.37.15Jazzi SehrawatPas encore d'évaluation

- 2014BankingIndustryOutlook DeloitteDocument20 pages2014BankingIndustryOutlook DeloittelapogkPas encore d'évaluation

- Happy April Fool Day, Ifians!! WE GOT YA!!! - 3970987 - Rules & Announcements ForumDocument9 pagesHappy April Fool Day, Ifians!! WE GOT YA!!! - 3970987 - Rules & Announcements ForumPoojaCambsPas encore d'évaluation

- Surbhi Maniacs CC-3 ReviewDocument6 pagesSurbhi Maniacs CC-3 ReviewJazzi SehrawatPas encore d'évaluation

- Internal AuditDocument1 pageInternal AuditJazzi SehrawatPas encore d'évaluation

- Distributed Rate Allocation For Inelastic Flows: Prashanth Hande, Shengyu Zhang, and Mung Chiang, Member, IEEEDocument14 pagesDistributed Rate Allocation For Inelastic Flows: Prashanth Hande, Shengyu Zhang, and Mung Chiang, Member, IEEEJazzi SehrawatPas encore d'évaluation

- 2014BankingIndustryOutlook DeloitteDocument20 pages2014BankingIndustryOutlook DeloittelapogkPas encore d'évaluation

- StoryDocument1 pageStoryJazzi SehrawatPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Quiz - Basic Corporate ConceptsDocument3 pagesQuiz - Basic Corporate ConceptsKimberly Etulle CelonaPas encore d'évaluation

- Senior Citizen Tax Benefit Rs 300,000Document47 pagesSenior Citizen Tax Benefit Rs 300,000SunitaPas encore d'évaluation

- 654 SampleDocument35 pages654 SampleRaed BoukeilehPas encore d'évaluation

- Ratio Analysis SampleDocument16 pagesRatio Analysis SampleRitoshree paulPas encore d'évaluation

- AFAR QuestionsDocument6 pagesAFAR QuestionsTerence Jeff TamondongPas encore d'évaluation

- Company Final AccountsDocument38 pagesCompany Final AccountsNeeti Chopra50% (2)

- Order in Respect of Madurai Rural Development Transformation India Limited and OthersDocument19 pagesOrder in Respect of Madurai Rural Development Transformation India Limited and OthersShyam SunderPas encore d'évaluation

- ACC 642 - CH 01 SolutionsDocument17 pagesACC 642 - CH 01 SolutionstboneuncwPas encore d'évaluation

- SABECODocument28 pagesSABECO김수영Pas encore d'évaluation

- Income Statement - PEPSICODocument11 pagesIncome Statement - PEPSICOAdriana MartinezPas encore d'évaluation

- How to Invest in Philippine Stock Market for Beginners GuideDocument19 pagesHow to Invest in Philippine Stock Market for Beginners GuideJennybabe Peta100% (1)

- Dwnload Full Foundations of Financial Management Canadian 10th Edition Block Solutions Manual PDFDocument20 pagesDwnload Full Foundations of Financial Management Canadian 10th Edition Block Solutions Manual PDFfruitfulbrawnedom7er4100% (10)

- Analyze Bartlett Company's Financial StatementsDocument46 pagesAnalyze Bartlett Company's Financial StatementsMustakim Bin Aziz 1610534630Pas encore d'évaluation

- (L) Chapter 13 Accounts For Limited CompanyDocument13 pages(L) Chapter 13 Accounts For Limited CompanyCHZE CHZI CHUAHPas encore d'évaluation

- David Hillier (2019)Document12 pagesDavid Hillier (2019)eriwirandanaPas encore d'évaluation

- Company Law: Corporate PersonalityDocument45 pagesCompany Law: Corporate PersonalityRavi shankarPas encore d'évaluation

- Valuation of GoodwillDocument7 pagesValuation of GoodwillRounaq Khanum284Pas encore d'évaluation

- Business Finance ExamDocument8 pagesBusiness Finance Examapi-342895963100% (3)

- BDO Unibank 2021 Annual Report Financial Highlights PDFDocument2 pagesBDO Unibank 2021 Annual Report Financial Highlights PDFJohn Michael Dela CruzPas encore d'évaluation

- 7.1lao v. Yao Bio Lim20210423-12-1v6ji2vDocument16 pages7.1lao v. Yao Bio Lim20210423-12-1v6ji2vSeok Gyeong KangPas encore d'évaluation

- 185f8question BankDocument18 pages185f8question Bank55amonPas encore d'évaluation

- Financial Management-2Document292 pagesFinancial Management-2benard owinoPas encore d'évaluation

- Money & Banking - MGT411 Spring 2010 Final Term Paper PDFDocument59 pagesMoney & Banking - MGT411 Spring 2010 Final Term Paper PDFrimshaPas encore d'évaluation

- ACCO 20043 Financial Accounting and Reporting 2 FinalsDocument16 pagesACCO 20043 Financial Accounting and Reporting 2 FinalsPaul BandolaPas encore d'évaluation

- Mindanao Mission Academy: Business FinanceDocument3 pagesMindanao Mission Academy: Business FinanceHLeigh Nietes-GabutanPas encore d'évaluation

- Maharajkumar Gopal Saran Narain Singh v. CITDocument3 pagesMaharajkumar Gopal Saran Narain Singh v. CITRonit KumarPas encore d'évaluation

- (India Studies in Business and Economics) P.K. Jain, Shveta Singh, Surendra Singh Yadav (Auth.) - Financial Management Practices - An Empirical Study of Indian Corporates (2013, Springer India) PDFDocument426 pages(India Studies in Business and Economics) P.K. Jain, Shveta Singh, Surendra Singh Yadav (Auth.) - Financial Management Practices - An Empirical Study of Indian Corporates (2013, Springer India) PDFmuj_aliPas encore d'évaluation

- Capital and FinancingDocument11 pagesCapital and FinancingaliyahnicoleeeePas encore d'évaluation

- ACTG 2011 - Midterm Package - 2012-2013Document44 pagesACTG 2011 - Midterm Package - 2012-2013waysPas encore d'évaluation

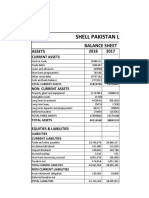

- Shell Pakistan LTD: Assets 2018 2017Document11 pagesShell Pakistan LTD: Assets 2018 2017mohammad bilalPas encore d'évaluation