Vous aimerez peut-être aussi

- CCHR Opening StatementDocument4 pagesCCHR Opening StatementThe Daily LinePas encore d'évaluation

- Emergency City EO2020-1Document6 pagesEmergency City EO2020-1The Daily LinePas encore d'évaluation

- Divvy Case DismissalDocument20 pagesDivvy Case DismissalThe Daily LinePas encore d'évaluation

- Woodlawn Housing Preservation Ordinance DRAFTDocument26 pagesWoodlawn Housing Preservation Ordinance DRAFTThe Daily LinePas encore d'évaluation

- COFA Analysis of Chicago's 2020 Expenditure PrioritiesDocument24 pagesCOFA Analysis of Chicago's 2020 Expenditure PrioritiesThe Daily Line100% (2)

- COVID-19 Telework PolicyDocument3 pagesCOVID-19 Telework PolicyThe Daily LinePas encore d'évaluation

- Consultant's 3rd Report On ISRsDocument139 pagesConsultant's 3rd Report On ISRsThe Daily LinePas encore d'évaluation

- Legal Memo in Support of D4 Complaint SignedDocument6 pagesLegal Memo in Support of D4 Complaint SignedThe Daily LinePas encore d'évaluation

- Health - Opening Statement-2020 Budget - FinalDocument3 pagesHealth - Opening Statement-2020 Budget - FinalThe Daily LinePas encore d'évaluation

- DOF Opening StatementDocument3 pagesDOF Opening StatementThe Daily LinePas encore d'évaluation

- OBM Opening StatementDocument3 pagesOBM Opening StatementThe Daily LinePas encore d'évaluation

- Chicago Consent Decree Year One Monitoring PlanDocument78 pagesChicago Consent Decree Year One Monitoring PlanThe Daily LinePas encore d'évaluation

- CPD Opening Statement FinalDocument5 pagesCPD Opening Statement FinalThe Daily LinePas encore d'évaluation

- CFO Opening StatementDocument3 pagesCFO Opening StatementThe Daily LinePas encore d'évaluation

- June 20, 2019 Cook County Democrats Pre-Slating ScheduleDocument2 pagesJune 20, 2019 Cook County Democrats Pre-Slating ScheduleThe Daily LinePas encore d'évaluation

- 2019 09 23 Working Toward A Healed City FINALDocument16 pages2019 09 23 Working Toward A Healed City FINALThe Daily LinePas encore d'évaluation

- Dkt. 23 Second Amended ComplaintDocument22 pagesDkt. 23 Second Amended ComplaintThe Daily LinePas encore d'évaluation

- Cfwo Draft - 07172019Document10 pagesCfwo Draft - 07172019The Daily LinePas encore d'évaluation

- FWW 072219Document12 pagesFWW 072219The Daily LinePas encore d'évaluation

- 2019-08-02 Uber V Chicago ComplaintDocument16 pages2019-08-02 Uber V Chicago ComplaintThe Daily LinePas encore d'évaluation

- June 21, 2019 Cook County Democrats Pre-Slating ScheduleDocument2 pagesJune 21, 2019 Cook County Democrats Pre-Slating ScheduleThe Daily LinePas encore d'évaluation

- Grant Thornton Audit AppendicesDocument51 pagesGrant Thornton Audit AppendicesThe Daily LinePas encore d'évaluation

- Advancing Equity 2019 - FINALBOOKDocument26 pagesAdvancing Equity 2019 - FINALBOOKThe Daily LinePas encore d'évaluation

- Mlel Sixtyday RPRT FinalDocument46 pagesMlel Sixtyday RPRT FinalThe Daily LinePas encore d'évaluation

- Cook County 2020 Preliminary Budget PresentationDocument23 pagesCook County 2020 Preliminary Budget PresentationThe Daily LinePas encore d'évaluation

- Assessor Listening Tour SlidesDocument22 pagesAssessor Listening Tour SlidesThe Daily LinePas encore d'évaluation

- MAY 30 Final Proposal Memo Press ReleaseDocument21 pagesMAY 30 Final Proposal Memo Press ReleaseThe Daily LinePas encore d'évaluation

- 5.28.19 - City Club Speech - FINALDocument16 pages5.28.19 - City Club Speech - FINALThe Daily LinePas encore d'évaluation

- Enhancing Our Culture Anti-Harassment Working Group Report 5-30-19Document32 pagesEnhancing Our Culture Anti-Harassment Working Group Report 5-30-19The Daily LinePas encore d'évaluation

- Stakeholder Letter On SB 1379 IIDocument3 pagesStakeholder Letter On SB 1379 IIThe Daily LinePas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (120)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Case 1Document8 pagesCase 1Pratibha SeshamPas encore d'évaluation

- Corporate Social Responsibility at Bharat Petroleum Corporation Limited IJERTCONV1IS02003Document4 pagesCorporate Social Responsibility at Bharat Petroleum Corporation Limited IJERTCONV1IS02003siddhartha karPas encore d'évaluation

- Terms and Conditions For Advertisement and ProformaDocument3 pagesTerms and Conditions For Advertisement and ProformaMallikarjunayya HiremathPas encore d'évaluation

- Labor Bar Syllabus 2020Document13 pagesLabor Bar Syllabus 2020Ronaldo ValladoresPas encore d'évaluation

- Research Proposal of Bba 7th SemesterDocument10 pagesResearch Proposal of Bba 7th SemesterAhmed MumtazPas encore d'évaluation

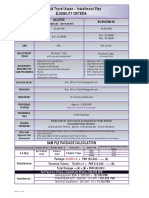

- Labbaik Travel Asaan - Installment Plan Eligibility CriteriaDocument1 pageLabbaik Travel Asaan - Installment Plan Eligibility CriteriamuhammadTzPas encore d'évaluation

- Unit 1 Business and Its EnvironmentDocument28 pagesUnit 1 Business and Its EnvironmentMaham ButtPas encore d'évaluation

- An Overview of Labour Law in RwandaDocument12 pagesAn Overview of Labour Law in Rwandap pPas encore d'évaluation

- LPA120 Fees Exemptions RemissionsDocument4 pagesLPA120 Fees Exemptions RemissionssriharshamysuruPas encore d'évaluation

- Chapter 6 - Income TaxDocument12 pagesChapter 6 - Income TaxlovelyrichPas encore d'évaluation

- Business Annals. Willard Long Thorp 8Document16 pagesBusiness Annals. Willard Long Thorp 8kirchyPas encore d'évaluation

- LM A1.1Document17 pagesLM A1.1Dat HoangPas encore d'évaluation

- Conference Board of Canada ReportDocument230 pagesConference Board of Canada ReportcaleyramsayPas encore d'évaluation

- Commissioned Officer's HandbookDocument133 pagesCommissioned Officer's HandbookBONDCK88507100% (2)

- Truth About TrustsDocument6 pagesTruth About TrustsCathy Reed100% (5)

- Public AdminstrationDocument19 pagesPublic AdminstrationUjjwal AnandPas encore d'évaluation

- HRMS QuestionnaireDocument16 pagesHRMS Questionnairearif61400% (1)

- NASSCOM Annual Report 2011-2012Document41 pagesNASSCOM Annual Report 2011-2012Devarsh YagnikPas encore d'évaluation

- CSR of Exim Bank of BanhladeshDocument10 pagesCSR of Exim Bank of BanhladeshZahid HasanPas encore d'évaluation

- International Journal of Organisational Innovation Final Issue Vol 7 Num 3 January 2015Document161 pagesInternational Journal of Organisational Innovation Final Issue Vol 7 Num 3 January 2015Vinit DawanePas encore d'évaluation

- DDUGKY - DARPG - Goa - Anil SubramaniamDocument24 pagesDDUGKY - DARPG - Goa - Anil SubramaniamRS ShekhawatPas encore d'évaluation

- US Passport ApplicationDocument6 pagesUS Passport ApplicationThe Slang Market100% (9)

- 6-Confederation For Unity, Et. Al. vs. Bureau of Internal and RevenueDocument6 pages6-Confederation For Unity, Et. Al. vs. Bureau of Internal and RevenueLandrel MatagaPas encore d'évaluation

- TWP 93272105 IffcoTokioDocument2 pagesTWP 93272105 IffcoTokioSudeep Kumar67% (3)

- L05 Occupational Health & Safety in SchoolsDocument63 pagesL05 Occupational Health & Safety in SchoolsJapsay Francisco GranadaPas encore d'évaluation

- Project Report On Employee SatisfactionDocument75 pagesProject Report On Employee SatisfactionNavpreet Singh100% (1)

- Study On Compensation and Benefits Its Influence oDocument8 pagesStudy On Compensation and Benefits Its Influence oStha RamabelePas encore d'évaluation

- E Ch6 Mathis Job AnalysisDocument64 pagesE Ch6 Mathis Job AnalysisNatik Bi IllahPas encore d'évaluation

- Anfin208 Mid Term AssignmentDocument6 pagesAnfin208 Mid Term Assignmentprince matamboPas encore d'évaluation

- Labor Case Digests (Doctrines) - Rhapsody P. JoseDocument8 pagesLabor Case Digests (Doctrines) - Rhapsody P. JoseRhapsody JosePas encore d'évaluation