Vous aimerez peut-être aussi

- A Market in WheatDocument14 pagesA Market in Wheatapi-27308853150% (2)

- How To Master Your Investment In 30 Minutes A Day (Preparation)D'EverandHow To Master Your Investment In 30 Minutes A Day (Preparation)Pas encore d'évaluation

- Pervert Trading: Advanced Candlestick AnalysisD'EverandPervert Trading: Advanced Candlestick AnalysisÉvaluation : 2 sur 5 étoiles2/5 (1)

- Forex Trading 3: Part 3: Trading with the Weekly High and LowD'EverandForex Trading 3: Part 3: Trading with the Weekly High and LowÉvaluation : 5 sur 5 étoiles5/5 (1)

- How to View and Forecast the Market: Forex Fundamental IndicatorsD'EverandHow to View and Forecast the Market: Forex Fundamental IndicatorsÉvaluation : 4 sur 5 étoiles4/5 (8)

- Trading with the Trendlines: Harmonic Patterns Strategy Trading Strategy. Forex, Stocks, FuturesD'EverandTrading with the Trendlines: Harmonic Patterns Strategy Trading Strategy. Forex, Stocks, FuturesPas encore d'évaluation

- Testing Neoclassical Competitive Market Theory in The Field: John A. ListDocument4 pagesTesting Neoclassical Competitive Market Theory in The Field: John A. ListpempaPas encore d'évaluation

- Forex Trading 1-2: Book 1: Practical examples,Book 2: How Do I Rate my Trading Results?D'EverandForex Trading 1-2: Book 1: Practical examples,Book 2: How Do I Rate my Trading Results?Évaluation : 5 sur 5 étoiles5/5 (5)

- The $300,000 Forex Trading StrategiesD'EverandThe $300,000 Forex Trading StrategiesÉvaluation : 4.5 sur 5 étoiles4.5/5 (11)

- Trading Options: Using Technical Analysis to Design Winning TradesD'EverandTrading Options: Using Technical Analysis to Design Winning TradesPas encore d'évaluation

- Lesson 2 Euro ActivityDocument17 pagesLesson 2 Euro ActivityFlyEngineerPas encore d'évaluation

- The Ultimate Forex Trading System-Unbeatable Strategy to Place 92% Winning TradesD'EverandThe Ultimate Forex Trading System-Unbeatable Strategy to Place 92% Winning TradesÉvaluation : 4 sur 5 étoiles4/5 (4)

- Cyber Bidding GatewayDocument5 pagesCyber Bidding GatewayMegha HalasangimathPas encore d'évaluation

- Strategize Your Investment In 30 Minutes A Day (Steps)D'EverandStrategize Your Investment In 30 Minutes A Day (Steps)Pas encore d'évaluation

- Lesson 3 - Trading Tactics 3Document1 pageLesson 3 - Trading Tactics 3salemivoryconsultingPas encore d'évaluation

- 4 Keys to Profitable Forex Trend Trading: Unlocking the Profit Potential of Trending Currency PairsD'Everand4 Keys to Profitable Forex Trend Trading: Unlocking the Profit Potential of Trending Currency PairsÉvaluation : 5 sur 5 étoiles5/5 (13)

- Economics for Investment Decision Makers Workbook: Micro, Macro, and International EconomicsD'EverandEconomics for Investment Decision Makers Workbook: Micro, Macro, and International EconomicsPas encore d'évaluation

- Options Basics: How To Read An Options Table: Printer Friendly Version (PDF Format) Jay KaeppelDocument4 pagesOptions Basics: How To Read An Options Table: Printer Friendly Version (PDF Format) Jay KaeppelRaunak MukherjeePas encore d'évaluation

- 1016 F Exp 1 WorksheetDocument5 pages1016 F Exp 1 WorksheetSaurav Tuladhar0% (2)

- Point and Figure - Brandon WendellDocument18 pagesPoint and Figure - Brandon WendellarjbakPas encore d'évaluation

- Forex Strategy: ST Patterns Trading Manual, Chart Analysis Step by Step, 300% for One MonthD'EverandForex Strategy: ST Patterns Trading Manual, Chart Analysis Step by Step, 300% for One MonthÉvaluation : 4.5 sur 5 étoiles4.5/5 (29)

- Trading Strategy: Fractal Corridors on the Futures, CFD and Forex Markets, Four Basic ST Patterns, 800% or More in Two MonthsD'EverandTrading Strategy: Fractal Corridors on the Futures, CFD and Forex Markets, Four Basic ST Patterns, 800% or More in Two MonthsÉvaluation : 4.5 sur 5 étoiles4.5/5 (31)

- Pattern, Price and Time: Using Gann Theory in Technical AnalysisD'EverandPattern, Price and Time: Using Gann Theory in Technical AnalysisPas encore d'évaluation

- FOREX Perfection In Manual, Automated And Predictive TradingD'EverandFOREX Perfection In Manual, Automated And Predictive TradingPas encore d'évaluation

- Reading Price Charts Bar by Bar: The Technical Analysis of Price Action for the Serious TraderD'EverandReading Price Charts Bar by Bar: The Technical Analysis of Price Action for the Serious TraderÉvaluation : 4.5 sur 5 étoiles4.5/5 (2)

- Swing Trading using the 4-hour chart 1-3: 3 ManuscriptsD'EverandSwing Trading using the 4-hour chart 1-3: 3 ManuscriptsÉvaluation : 4.5 sur 5 étoiles4.5/5 (27)

- The Supply and Demand Game Part 1: How The Game WorksDocument6 pagesThe Supply and Demand Game Part 1: How The Game WorksJa Mi LahPas encore d'évaluation

- Course Pricing Strategies: Your Guide to Confidently Pricing Your Online CourseD'EverandCourse Pricing Strategies: Your Guide to Confidently Pricing Your Online CoursePas encore d'évaluation

- Case StudyDocument10 pagesCase StudyradiobuonntPas encore d'évaluation

- Babypips Resume KindergardenDocument5 pagesBabypips Resume KindergardenAdhemar QuinteiroPas encore d'évaluation

- Scalping is Fun! 2: Part 2: Practical examplesD'EverandScalping is Fun! 2: Part 2: Practical examplesÉvaluation : 4.5 sur 5 étoiles4.5/5 (26)

- Supply and Demand Trading: How to Master the Trading ZonesD'EverandSupply and Demand Trading: How to Master the Trading ZonesÉvaluation : 4.5 sur 5 étoiles4.5/5 (32)

- Value-based Marketing Strategy: Pricing and Costs for Relationship MarketingD'EverandValue-based Marketing Strategy: Pricing and Costs for Relationship MarketingPas encore d'évaluation

- Making Money with Binary Options Financial TradingD'EverandMaking Money with Binary Options Financial TradingÉvaluation : 4 sur 5 étoiles4/5 (5)

- Case StudyDocument11 pagesCase StudyKester NdabaiPas encore d'évaluation

- Analyzing and Reporting Market TrendsDocument9 pagesAnalyzing and Reporting Market TrendsEnp Gus Agosto100% (1)

- The Sunk-Cost Fallacy in Penny Auctions: Ned Augenblick July 2015Document45 pagesThe Sunk-Cost Fallacy in Penny Auctions: Ned Augenblick July 2015Anonymous abise7Pas encore d'évaluation

- Trading Code is Open: ST Patterns of the Forex and Futures Exchanges, 100% Profit per Month, Proven Market Strategy, Robots, Scripts, AlertsD'EverandTrading Code is Open: ST Patterns of the Forex and Futures Exchanges, 100% Profit per Month, Proven Market Strategy, Robots, Scripts, AlertsÉvaluation : 4.5 sur 5 étoiles4.5/5 (51)

- The SaaS Sales Method for Account Executives: How to Win Customers: Sales Blueprints, #5D'EverandThe SaaS Sales Method for Account Executives: How to Win Customers: Sales Blueprints, #5Pas encore d'évaluation

- TASK 16 Vidhi SanchetiDocument22 pagesTASK 16 Vidhi SanchetiVidhi SanchetiPas encore d'évaluation

- 98eer-Ascending-Auctions 1Document12 pages98eer-Ascending-Auctions 1Ad AcrPas encore d'évaluation

- The Trading Game InstructionsDocument12 pagesThe Trading Game InstructionsJoeWaller0% (1)

- Fw15-Marketing Mix: DurationDocument17 pagesFw15-Marketing Mix: DurationVinod PandeyPas encore d'évaluation

- Advanced MP Manual RezaDocument33 pagesAdvanced MP Manual RezaAyman erPas encore d'évaluation

- Price StructureDocument30 pagesPrice StructureMASTERfun GAMINGPas encore d'évaluation

- The Trading Playbook: Two rule-based plans for day trading and swing tradingD'EverandThe Trading Playbook: Two rule-based plans for day trading and swing tradingÉvaluation : 4 sur 5 étoiles4/5 (16)

- Selling Real Estate Services: Third-Level Secrets of Top ProducersD'EverandSelling Real Estate Services: Third-Level Secrets of Top ProducersPas encore d'évaluation

- Post 1 of 4: The First and Foremost Lesson Learned Is To Have An EdgeDocument30 pagesPost 1 of 4: The First and Foremost Lesson Learned Is To Have An EdgeJuan Miguel llPas encore d'évaluation

- PepsodentDocument12 pagesPepsodentMansha ShaikhPas encore d'évaluation

- Ch05 Part 2 Questions and Problems AnswersDocument5 pagesCh05 Part 2 Questions and Problems AnswersJemma JadePas encore d'évaluation

- PH Conditional Sentences (Nadia Fairuz Shafa XI OTKP 2)Document3 pagesPH Conditional Sentences (Nadia Fairuz Shafa XI OTKP 2)nadia fairuz shafaPas encore d'évaluation

- Supply and DemandDocument3 pagesSupply and DemandKeira TanPas encore d'évaluation

- Mock Exam Paper - 28 - April - 2022Document3 pagesMock Exam Paper - 28 - April - 2022dilinhtinh04Pas encore d'évaluation

- Margin UpdatedDocument35 pagesMargin Updatedparinita raviPas encore d'évaluation

- Chapter 4. Understanding Interest RatesDocument40 pagesChapter 4. Understanding Interest RatesThive PhinaPas encore d'évaluation

- General Comments: The Chartered Institute of Management AccountantsDocument25 pagesGeneral Comments: The Chartered Institute of Management AccountantsSritijhaaPas encore d'évaluation

- Brown Photo Travel Sales - Product Landscape Z-Fold BrochureDocument1 pageBrown Photo Travel Sales - Product Landscape Z-Fold BrochureDavid ColmenaresPas encore d'évaluation

- Exercises IA 2Document7 pagesExercises IA 2Amaurrie ArpilledaPas encore d'évaluation

- Assignment Nos. 11 OligopolyDocument2 pagesAssignment Nos. 11 OligopolyJoana MariePas encore d'évaluation

- Ketan Parekh ScamDocument3 pagesKetan Parekh ScamNeha SinghPas encore d'évaluation

- Merger and Acquistion 3Document15 pagesMerger and Acquistion 3Nidhi KabraPas encore d'évaluation

- Marketing Management Lecture 4Document27 pagesMarketing Management Lecture 4Mandeep Kumar HassaniPas encore d'évaluation

- PricingDocument3 pagesPricingDisha AroraPas encore d'évaluation

- 05 - Risk and Return Practice QuestionsDocument4 pages05 - Risk and Return Practice QuestionsANUJA RAPURKARPas encore d'évaluation

- Comparative Study of Two Brands-Demand Patterns and Pricing StrategiesDocument6 pagesComparative Study of Two Brands-Demand Patterns and Pricing Strategiesparth saklechaPas encore d'évaluation

- 08 Costing by Products Joint ProductsDocument15 pages08 Costing by Products Joint ProductsMichael Brian TorresPas encore d'évaluation

- Investment & Portfolio MGT AssignmentDocument2 pagesInvestment & Portfolio MGT AssignmentAgidew ShewalemiPas encore d'évaluation

- Worksheet - Chapter 2: True or False?Document2 pagesWorksheet - Chapter 2: True or False?Niloy BiswasPas encore d'évaluation

- TYBFM MinDocument48 pagesTYBFM MinBeauty AkterPas encore d'évaluation

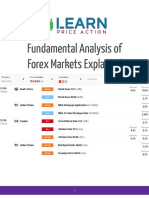

- Fundamental Analysis of Forex Markets ExplainedDocument13 pagesFundamental Analysis of Forex Markets ExplainedAar Rageedi0% (1)

- Commercial Correspondence Unit 2: Enquiries and RepliesDocument31 pagesCommercial Correspondence Unit 2: Enquiries and RepliesTovinPas encore d'évaluation

- Employee Share Schemes: Group Sharesave Scheme (SAYE)Document4 pagesEmployee Share Schemes: Group Sharesave Scheme (SAYE)Steve MedhurstPas encore d'évaluation

- Chapter 3: Management of Working Capital 3.0 Current Asset ManagementDocument15 pagesChapter 3: Management of Working Capital 3.0 Current Asset Managementraqib ayubPas encore d'évaluation

- Pricing Strategy Comprehensive ReportDocument20 pagesPricing Strategy Comprehensive ReportSapphire AliasPas encore d'évaluation

- Module 5 Short Term Decision MakingDocument26 pagesModule 5 Short Term Decision MakingPang Siulien100% (1)

- Ca Final Strategic Financial Management Full Test 1 May 2022 Test Paper 1644507041Document12 pagesCa Final Strategic Financial Management Full Test 1 May 2022 Test Paper 1644507041itaxkgcPas encore d'évaluation

- Stock PitchDocument6 pagesStock PitchL57Sejal SastePas encore d'évaluation

- CH 7 The Production Process - The Behaviour of Profit Maximising FirmDocument32 pagesCH 7 The Production Process - The Behaviour of Profit Maximising FirmBhargav D.S.Pas encore d'évaluation