Vous aimerez peut-être aussi

- Volatilidad Del Tipo de CambioDocument23 pagesVolatilidad Del Tipo de CambioRamiro PazPas encore d'évaluation

- Stock Returns and Inflation: The Impact of Inflation TargetingDocument8 pagesStock Returns and Inflation: The Impact of Inflation TargetingVANNGUYEN84Pas encore d'évaluation

- Long Run Dynamics of Regional Growth 2002 Oyarzun & Araya Estudios de EconomiaDocument10 pagesLong Run Dynamics of Regional Growth 2002 Oyarzun & Araya Estudios de EconomiaCristián Patricio Machuca CabreraPas encore d'évaluation

- Nonlinear Income Convergence and Structural Breaks: Further Empirical EvidenceDocument8 pagesNonlinear Income Convergence and Structural Breaks: Further Empirical EvidenceViverPas encore d'évaluation

- Alesina TogetherDocument17 pagesAlesina TogetherfabiocasaliPas encore d'évaluation

- Applied Economics LettersDocument6 pagesApplied Economics LettersHimani ChoudharyPas encore d'évaluation

- New Root Test PPP 1997Document6 pagesNew Root Test PPP 1997Christofer JimenezPas encore d'évaluation

- Theoretical FrameworkDocument2 pagesTheoretical FrameworkMark Dennis AsuncionPas encore d'évaluation

- Jfamm 21 3 2015Document6 pagesJfamm 21 3 2015Arzu ZeynalovPas encore d'évaluation

- 4.applied - Cointegration Approach A Solvency-Adewojo AdekunbiDocument8 pages4.applied - Cointegration Approach A Solvency-Adewojo AdekunbiImpact JournalsPas encore d'évaluation

- Determinants of Economic Growth: Empirical Evidence From Russian RegionsDocument19 pagesDeterminants of Economic Growth: Empirical Evidence From Russian RegionsRoberto GuzmánPas encore d'évaluation

- Bank Credit and Economic Growth in EU-27Document10 pagesBank Credit and Economic Growth in EU-27subornoPas encore d'évaluation

- Two-Stage BudgetingDocument5 pagesTwo-Stage BudgetingdelodiloPas encore d'évaluation

- Neutrality in US - AangDocument20 pagesNeutrality in US - AangDidiek Handayani GustiPas encore d'évaluation

- Public Capital Stock and State ProductivDocument9 pagesPublic Capital Stock and State ProductivPili MesaPas encore d'évaluation

- Tax Evasion Influence in Public DebtsDocument12 pagesTax Evasion Influence in Public DebtslilyanamaPas encore d'évaluation

- Abstract ExampleDocument26 pagesAbstract ExampleloloPas encore d'évaluation

- Abstract - Dr. Sunetra Ghatak - Session 2Document4 pagesAbstract - Dr. Sunetra Ghatak - Session 2সাদিক মাহবুব ইসলামPas encore d'évaluation

- Recession InequalityDocument24 pagesRecession InequalityThe IsaiasPas encore d'évaluation

- Granger Causality PanelDocument15 pagesGranger Causality PanelpareekPas encore d'évaluation

- An Econometric View On The Estimation of Gravity Models and The Calculation of Trade PotentialsDocument16 pagesAn Econometric View On The Estimation of Gravity Models and The Calculation of Trade PotentialsJaime RicardoPas encore d'évaluation

- BCM in Small Open EconomyDocument25 pagesBCM in Small Open EconomycarogonherPas encore d'évaluation

- Does Domestic Saving Cause Economic GrowthDocument23 pagesDoes Domestic Saving Cause Economic GrowthAparajay SurnamelessPas encore d'évaluation

- New Structuralist Exchange Rate PolicyDocument28 pagesNew Structuralist Exchange Rate PolicyAlexandre FreitasPas encore d'évaluation

- Fractionally Integrated Generalized AutoregressiveDocument28 pagesFractionally Integrated Generalized AutoregressiveDimitrios KolomvasPas encore d'évaluation

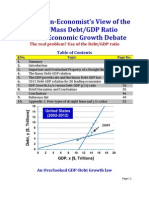

- An MIT Non-Economist's View of The Harvard-UMass Debt/GDP Ratio and The Economic Growth DebateDocument74 pagesAn MIT Non-Economist's View of The Harvard-UMass Debt/GDP Ratio and The Economic Growth DebateVJLaxmananPas encore d'évaluation

- Ferson Harvey 94 Sources of Risk and Expected Returns in Global Equity MarketsDocument29 pagesFerson Harvey 94 Sources of Risk and Expected Returns in Global Equity MarketsPeterParker1983Pas encore d'évaluation

- Permanent and Transitory Components of European Business CycleDocument17 pagesPermanent and Transitory Components of European Business CycleDeborah KimPas encore d'évaluation

- Export Growth and Output GrowthDocument11 pagesExport Growth and Output GrowthMOHD NOR HIDAYAT MELBINPas encore d'évaluation

- Accounting For Real and Nominal Exchange Rate Movements in The Post-Bretton Woods PeriodDocument22 pagesAccounting For Real and Nominal Exchange Rate Movements in The Post-Bretton Woods PeriodStephanie GleasonPas encore d'évaluation

- Barro ConvergenceDocument30 pagesBarro ConvergenceIrán ApolinarPas encore d'évaluation

- Financial Leverage ResearchDocument45 pagesFinancial Leverage ResearchGaucho MisaPas encore d'évaluation

- MANDIMIKA Et Al-2012-South African Journal of EconomicsDocument22 pagesMANDIMIKA Et Al-2012-South African Journal of EconomicsRym CharefPas encore d'évaluation

- 2015 Fiscal SustainabilityDocument6 pages2015 Fiscal SustainabilityjamelPas encore d'évaluation

- Impact of Money Supply On Current Account: Extent of PakistanDocument9 pagesImpact of Money Supply On Current Account: Extent of Pakistanhuma788Pas encore d'évaluation

- The Determinants of Future Economic Growth - 0Document27 pagesThe Determinants of Future Economic Growth - 0Shivam KumarPas encore d'évaluation

- Stock Watson Ecta 1993Document38 pagesStock Watson Ecta 1993lorenzo costaPas encore d'évaluation

- Actuarial Note On Loss RatingDocument7 pagesActuarial Note On Loss RatingHenry MensahPas encore d'évaluation

- 06quah EER1993 PDFDocument10 pages06quah EER1993 PDFSkylark VaipheiPas encore d'évaluation

- Common Dynamics Between The US and Puerto Rico EconomiesDocument11 pagesCommon Dynamics Between The US and Puerto Rico EconomiesCésar R. SobrinoPas encore d'évaluation

- 14-Capital Account Liberalization and InflationDocument5 pages14-Capital Account Liberalization and InflationkiagengmenakPas encore d'évaluation

- Import Competition and Market Power: Canadian Evidence: Aileen J. Thompson Federal Trade Commission Washington, DCDocument24 pagesImport Competition and Market Power: Canadian Evidence: Aileen J. Thompson Federal Trade Commission Washington, DCmarhelunPas encore d'évaluation

- Understanding VolatilityDocument9 pagesUnderstanding VolatilityrajadeyPas encore d'évaluation

- Ruge Murcia PDFDocument43 pagesRuge Murcia PDFJoab Dan Valdivia CoriaPas encore d'évaluation

- Exchange Rate Pass-Through To Import Prices, and Monetary Policy in South AfricaDocument5 pagesExchange Rate Pass-Through To Import Prices, and Monetary Policy in South AfricaArif SetyaPas encore d'évaluation

- Solow y DataDocument7 pagesSolow y DataVanessa Carlos morianoPas encore d'évaluation

- HHM 020Document35 pagesHHM 020piwegod476Pas encore d'évaluation

- The Sources of The Great Moderation: A Survey: Bcoric@efst - HRDocument26 pagesThe Sources of The Great Moderation: A Survey: Bcoric@efst - HRtim__2002Pas encore d'évaluation

- Divisia Monetary Aggregates, The Great Ratios, and Classical Money Demand FunctionsDocument13 pagesDivisia Monetary Aggregates, The Great Ratios, and Classical Money Demand FunctionsEugenio MartinezPas encore d'évaluation

- Beta, Size, Book-To-Market, and The Cross-Section of Stock Returns in Taiwan: Measurement Errors and SeasonalitiesDocument30 pagesBeta, Size, Book-To-Market, and The Cross-Section of Stock Returns in Taiwan: Measurement Errors and SeasonalitiesQuan LePas encore d'évaluation

- Data and Methodology: Effect On Foreign Direct Investment (FDI)Document6 pagesData and Methodology: Effect On Foreign Direct Investment (FDI)ArafatPas encore d'évaluation

- ICOA 2010 Spinthropoulos KonstantinosDocument9 pagesICOA 2010 Spinthropoulos Konstantinosspithas_teikozPas encore d'évaluation

- Drawbacks in The 3-Factor Approach of Fama and French (2018)Document36 pagesDrawbacks in The 3-Factor Approach of Fama and French (2018)Zain-ul- FaridPas encore d'évaluation

- The University of Chicago PressDocument17 pagesThe University of Chicago PressaghamcPas encore d'évaluation

- The Relationship Between Risk and Expected Return in Europe: Ángel León (University of Alicante)Document33 pagesThe Relationship Between Risk and Expected Return in Europe: Ángel León (University of Alicante)Rym CharefPas encore d'évaluation

- Determinants of Economic Growth: Empirical Evidence From Russian RegionsDocument32 pagesDeterminants of Economic Growth: Empirical Evidence From Russian RegionsChristopher ImanuelPas encore d'évaluation

- Guo 2017Document8 pagesGuo 2017Ilham SetiawanPas encore d'évaluation

- Barrio Castaro New Evidence On International R&D Spillovers, Human Capital and Productivity in The OECDDocument5 pagesBarrio Castaro New Evidence On International R&D Spillovers, Human Capital and Productivity in The OECDIpsita RoyPas encore d'évaluation

- Jcotter RomeDocument33 pagesJcotter RomeAugustin Tadiamba PambiPas encore d'évaluation

- Learnings From DJ SirDocument94 pagesLearnings From DJ SirHare KrishnaPas encore d'évaluation

- Taxation in Ghana Re Digibooks 1 PDFDocument183 pagesTaxation in Ghana Re Digibooks 1 PDFLetsah BrightPas encore d'évaluation

- Banks Credit and Agricultural Sector Output in NigeriaDocument12 pagesBanks Credit and Agricultural Sector Output in NigeriaPORI ENTERPRISESPas encore d'évaluation

- Hedge Funds: Origins and Evolution: John H. MakinDocument17 pagesHedge Funds: Origins and Evolution: John H. MakinHiren ShahPas encore d'évaluation

- Corruption in Japan - An Economist's PerspectiveDocument19 pagesCorruption in Japan - An Economist's PerspectiveKarthikeyan ArumugathandavanPas encore d'évaluation

- PenswastaanDocument11 pagesPenswastaanRidawati LimpuPas encore d'évaluation

- Problems On Internal ReconstructionDocument24 pagesProblems On Internal ReconstructionYashodhan Mithare100% (4)

- SBI PO Application FormDocument4 pagesSBI PO Application FormPranav SahilPas encore d'évaluation

- Hedge Funds-Case StudyDocument20 pagesHedge Funds-Case StudyRohan BurmanPas encore d'évaluation

- Anti Take Over Tactics Merger and AcquisitionDocument29 pagesAnti Take Over Tactics Merger and AcquisitionMuhammad Nabeel Muhammad0% (1)

- Universiti Teknologi Mara Common Test 1: Confidential 1 AC/JAN 2017/FAR320Document5 pagesUniversiti Teknologi Mara Common Test 1: Confidential 1 AC/JAN 2017/FAR320NURAISHA AIDA ATANPas encore d'évaluation

- Fin Statement AnalysisDocument22 pagesFin Statement AnalysisJon MickPas encore d'évaluation

- Horngren'S Accounting - Tenth Edition: Chapter 2: Recording Business Transactions Page 1 of 111Document111 pagesHorngren'S Accounting - Tenth Edition: Chapter 2: Recording Business Transactions Page 1 of 111Sally MillerPas encore d'évaluation

- Group Assignment FIN533 - Group 4Document22 pagesGroup Assignment FIN533 - Group 4Muhammad Atiq100% (1)

- Jose Luis Colon Roman v. United States of America, 817 F.2d 1, 1st Cir. (1987)Document4 pagesJose Luis Colon Roman v. United States of America, 817 F.2d 1, 1st Cir. (1987)Scribd Government DocsPas encore d'évaluation

- TAK CH 12 - Group 2Document70 pagesTAK CH 12 - Group 2Azka AhdiPas encore d'évaluation

- 10000000296Document132 pages10000000296Chapter 11 DocketsPas encore d'évaluation

- Budgeting and Goal Setting 27715 20231031183226Document111 pagesBudgeting and Goal Setting 27715 20231031183226Nicolle MoranPas encore d'évaluation

- Church Quiet TitleDocument119 pagesChurch Quiet Titlejerry mcleodPas encore d'évaluation

- 2021 BEA1101 Study Unit 5 SolutionsDocument13 pages2021 BEA1101 Study Unit 5 SolutionsKhanyisilePas encore d'évaluation

- Risk Management For Banking SectorDocument46 pagesRisk Management For Banking SectorNaeem Uddin88% (17)

- 2 Ac4Document2 pages2 Ac4Rafols AnnabellePas encore d'évaluation

- Mariner QuestionnaireDocument2 pagesMariner QuestionnaireMonique Van Kan-WierstraPas encore d'évaluation

- Banking RegulationsDocument22 pagesBanking RegulationsBinay AcharyaPas encore d'évaluation

- Week 1 Notes From Chapter 2 - Investment in Equity SecuritiesDocument14 pagesWeek 1 Notes From Chapter 2 - Investment in Equity SecuritiesgloriyaPas encore d'évaluation

- Beps Action 2Document32 pagesBeps Action 2qi liuPas encore d'évaluation

- Solutions Manual: Modern Auditing & Assurance ServicesDocument17 pagesSolutions Manual: Modern Auditing & Assurance ServicessanjanaPas encore d'évaluation

- Module 4Document3 pagesModule 4Robin Mar AcobPas encore d'évaluation

- Project Two Chainz (Dual Process - Marry or Stay Single)Document10 pagesProject Two Chainz (Dual Process - Marry or Stay Single)TucsonTycoonPas encore d'évaluation

- Topics Covered: Does Debt Policy Matter ?Document11 pagesTopics Covered: Does Debt Policy Matter ?Tam DoPas encore d'évaluation