Vous aimerez peut-être aussi

- DynaLiners Weekly 49-2015Document12 pagesDynaLiners Weekly 49-2015Somayajula SuryaramPas encore d'évaluation

- Tankers Dry Bulk: Published by Fearnresearch 18. September 2013Document3 pagesTankers Dry Bulk: Published by Fearnresearch 18. September 2013SimmarinePas encore d'évaluation

- Intermodal Weekly 01-2012Document8 pagesIntermodal Weekly 01-2012Wisnu KertaningnagoroPas encore d'évaluation

- Container Market PDFDocument3 pagesContainer Market PDFDhruv AgarwalPas encore d'évaluation

- Shipping Market Report 17082011Document18 pagesShipping Market Report 17082011bleuwinzPas encore d'évaluation

- CRSL Presentation 2nd October 2013 FinalDocument41 pagesCRSL Presentation 2nd October 2013 FinalWilliam FergusonPas encore d'évaluation

- Worldyards May 2007 NewsletterDocument20 pagesWorldyards May 2007 Newsletternestor mospanPas encore d'évaluation

- Daily Market Report: Poten & PartnersDocument1 pageDaily Market Report: Poten & PartnersalgeriacandaPas encore d'évaluation

- Willis Energy Market Review 2013 PDFDocument92 pagesWillis Energy Market Review 2013 PDFsushilk28Pas encore d'évaluation

- Intermodal Weekly Market Report 3rd February 2015, Week 5Document9 pagesIntermodal Weekly Market Report 3rd February 2015, Week 5Budi PrayitnoPas encore d'évaluation

- SRJ Aug Sep 2009Document76 pagesSRJ Aug Sep 2009majdirossrossPas encore d'évaluation

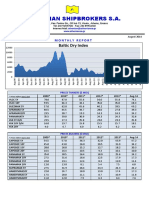

- Athenian Shipbrokers - Monthy Report - 14.08.15Document17 pagesAthenian Shipbrokers - Monthy Report - 14.08.15georgevarsasPas encore d'évaluation

- Polymerscan: Americas Polymer Spot Price AssessmentsDocument29 pagesPolymerscan: Americas Polymer Spot Price AssessmentsmcontrerjPas encore d'évaluation

- SSY Chemical WeeklyDocument3 pagesSSY Chemical WeeklyBeytullah KokoçPas encore d'évaluation

- Po 20140910Document30 pagesPo 20140910mcontrerjPas encore d'évaluation

- Complete Reference ListDocument10 pagesComplete Reference ListdocdumpsterPas encore d'évaluation

- Monthly Oil Market Report - Feb 2023Document24 pagesMonthly Oil Market Report - Feb 2023asaPas encore d'évaluation

- Euro Gas DailyDocument8 pagesEuro Gas DailyJose DenizPas encore d'évaluation

- Week 34Document18 pagesWeek 34notaristisPas encore d'évaluation

- LPGDocument15 pagesLPGMilkiss SweetPas encore d'évaluation

- Chemf 2007 3Document124 pagesChemf 2007 3Anupam AsthanaPas encore d'évaluation

- Daily Market ReportDocument1 pageDaily Market ReportSmitha MohanPas encore d'évaluation

- Argus: Tanker FreightDocument25 pagesArgus: Tanker FreightIvan OsipovPas encore d'évaluation

- Platts 2020 Outlook Report PDFDocument21 pagesPlatts 2020 Outlook Report PDFKamal ShayedPas encore d'évaluation

- Fixation of JLPL & VSPL Tariff by PNGRB: An Overview of Gail'S Submissions To The BoardDocument10 pagesFixation of JLPL & VSPL Tariff by PNGRB: An Overview of Gail'S Submissions To The BoardSanjai bhadouriaPas encore d'évaluation

- Market ScanDocument23 pagesMarket ScanGhasem2010Pas encore d'évaluation

- Chemical Forecaster Exec Summary TOCDocument12 pagesChemical Forecaster Exec Summary TOCalgeriacandaPas encore d'évaluation

- Shipping Intelligence 26.novDocument20 pagesShipping Intelligence 26.novleejingsongPas encore d'évaluation

- RDocument34 pagesRJhoel HuanacoPas encore d'évaluation

- Compass Weekly Report November 20-2009Document7 pagesCompass Weekly Report November 20-2009Abdul BasitPas encore d'évaluation

- Shipping OutlookDocument27 pagesShipping OutlookmervynteoPas encore d'évaluation

- Chemf 2007 2Document120 pagesChemf 2007 2Anupam AsthanaPas encore d'évaluation

- Drimcgrawhill - Platts - Oilgram Price Report Nov 96Document12 pagesDrimcgrawhill - Platts - Oilgram Price Report Nov 96Cristhian AymaPas encore d'évaluation

- LW 20180731Document10 pagesLW 20180731Victor FernandezPas encore d'évaluation

- Ihs Markit Is SectorsDocument2 pagesIhs Markit Is SectorsKapilanNavaratnamPas encore d'évaluation

- Opr 20181205Document32 pagesOpr 20181205rojovies24Pas encore d'évaluation

- Dry Bulk Research 9sep16Document13 pagesDry Bulk Research 9sep16Takis RappasPas encore d'évaluation

- Chart of The Week: Inside This IssueDocument13 pagesChart of The Week: Inside This IssueAdrian Marin100% (1)

- Dry BulkDocument28 pagesDry BulkyousfinacerPas encore d'évaluation

- RS Platou Global Support Vessel Monthly February 2012Document15 pagesRS Platou Global Support Vessel Monthly February 2012kelvin_chong_38Pas encore d'évaluation

- Chemf 2007 1Document126 pagesChemf 2007 1Anupam AsthanaPas encore d'évaluation

- Platts LPG Gaswire 23082013Document6 pagesPlatts LPG Gaswire 23082013udelmarkPas encore d'évaluation

- Shipyards: Builders Risks & Conversion Risks: What Is Builders Risks Insurance and Who Buys This Coverage?Document2 pagesShipyards: Builders Risks & Conversion Risks: What Is Builders Risks Insurance and Who Buys This Coverage?Indra SatriaPas encore d'évaluation

- Shipping Market Fearnleys Week 52Document1 pageShipping Market Fearnleys Week 52VizziniPas encore d'évaluation

- (E) Drybulk Daily Report 2018-12-11 (Vol. 180)Document3 pages(E) Drybulk Daily Report 2018-12-11 (Vol. 180)amornrat kampitthayakulPas encore d'évaluation

- Argus: Coal Daily InternationalDocument15 pagesArgus: Coal Daily InternationalUmang KadivarPas encore d'évaluation

- The Worlds Top Ship Broking FirmsDocument2 pagesThe Worlds Top Ship Broking Firmsjikkuabraham2Pas encore d'évaluation

- AMR SummaryDocument37 pagesAMR SummaryChatkamol KaewbuddeePas encore d'évaluation

- The Platou Report 2014Document30 pagesThe Platou Report 2014Tze Yi Tay100% (1)

- QA Monthly Report 2022-09 SeptemberDocument32 pagesQA Monthly Report 2022-09 SeptemberMark Mirosevic-SorgoPas encore d'évaluation

- Affinity Research Crude Oil Tanker Outlook 2016-11-16Document64 pagesAffinity Research Crude Oil Tanker Outlook 2016-11-16LondonguyPas encore d'évaluation

- Shipping Market Review May 2020Document80 pagesShipping Market Review May 2020stanleyPas encore d'évaluation

- Case Study: Ocean Carriers Inc.: Members Team: TitanicDocument9 pagesCase Study: Ocean Carriers Inc.: Members Team: TitanicAnkitPas encore d'évaluation

- Urea Weekly Market Report 6 Sept17Document18 pagesUrea Weekly Market Report 6 Sept17Victor VazquezPas encore d'évaluation

- Athenian Shipbrokers - Monthy Report - 13.11.15 PDFDocument20 pagesAthenian Shipbrokers - Monthy Report - 13.11.15 PDFgeorgevarsas0% (1)

- Vam PricesDocument28 pagesVam PricesMandar J DeshpandePas encore d'évaluation

- REPORT SPB Vessel ForecastDocument139 pagesREPORT SPB Vessel ForecastLucyoy5358Pas encore d'évaluation

- White Paper - Steve Wray - Economies of Scale in Container Ships and Terminals - ENDocument8 pagesWhite Paper - Steve Wray - Economies of Scale in Container Ships and Terminals - ENNicolePas encore d'évaluation

- Three Shipping Alliances To Control Container ShippingDocument6 pagesThree Shipping Alliances To Control Container ShippingThavam RatnaPas encore d'évaluation

- Ship Project - Final PDFDocument230 pagesShip Project - Final PDFSamir Alshaar100% (3)

- Salary Slip & Transfer Confirmation: Date: Period: Bank: Account # Name: Title: Dept: Emp #Document2 pagesSalary Slip & Transfer Confirmation: Date: Period: Bank: Account # Name: Title: Dept: Emp #Adheesh SanthoshPas encore d'évaluation

- Internal Sales Representative As of SAP ERP EhP5 (New)Document32 pagesInternal Sales Representative As of SAP ERP EhP5 (New)Khalid SayeedPas encore d'évaluation

- Problem: Regular Model Advanced Model Deluxe ModelDocument8 pagesProblem: Regular Model Advanced Model Deluxe ModelExpert Answers100% (1)

- Muhammad Rashid Khan: EmployerDocument3 pagesMuhammad Rashid Khan: EmployerAzam BanuriPas encore d'évaluation

- RAD Project PlanDocument9 pagesRAD Project PlannasoonyPas encore d'évaluation

- Indian Law Solved Case StudiesDocument14 pagesIndian Law Solved Case StudiesJay PatelPas encore d'évaluation

- Web Based Crime Management SystemDocument22 pagesWeb Based Crime Management SystemZain Ul Abedin SaleemPas encore d'évaluation

- CR 2015Document13 pagesCR 2015Agr AcabdiaPas encore d'évaluation

- NNN Bank Report Q1 2019Document3 pagesNNN Bank Report Q1 2019netleasePas encore d'évaluation

- Costa CoffeeDocument18 pagesCosta CoffeeNuwan Liyanagamage75% (4)

- Introduction To Operation ManagementDocument78 pagesIntroduction To Operation ManagementNico Pascual IIIPas encore d'évaluation

- Aeon Corporate EthicsDocument0 pageAeon Corporate EthicsTan SuzenPas encore d'évaluation

- BCG MatrixDocument1 pageBCG MatrixFritz IgnacioPas encore d'évaluation

- Additional Private Admissions List 2014 2015Document25 pagesAdditional Private Admissions List 2014 2015Mayra GarrettPas encore d'évaluation

- Funds FlowDocument5 pagesFunds FlowSubha KalyanPas encore d'évaluation

- She Bsa 4-2Document7 pagesShe Bsa 4-2Justine GuilingPas encore d'évaluation

- Comparing FTTH Access Networks Based On P2P and PMP Fibre TopologiesDocument9 pagesComparing FTTH Access Networks Based On P2P and PMP Fibre TopologiesWewe SlmPas encore d'évaluation

- Engleski 3 Pocetni - Nastavak Vezbanja Za Prvi KolokvijumDocument8 pagesEngleski 3 Pocetni - Nastavak Vezbanja Za Prvi KolokvijumJeanette McmillanPas encore d'évaluation

- Jis B 1196Document19 pagesJis B 1196indecePas encore d'évaluation

- NAFTA Verification and Audit ManualDocument316 pagesNAFTA Verification and Audit Manualbiharris22Pas encore d'évaluation

- Baspelancongan 30 Jun 2015Document1 400 pagesBaspelancongan 30 Jun 2015Mohd Shahlan Sidi AhmadPas encore d'évaluation

- Lunar Rubbers PVT LTDDocument76 pagesLunar Rubbers PVT LTDSabeer Hamsa67% (3)

- Purchase 50.000 MT of CoalDocument1 pagePurchase 50.000 MT of CoalFarlinton HutagaolPas encore d'évaluation

- QuestionnaireDocument5 pagesQuestionnaireDivya BajajPas encore d'évaluation

- Vishal Mega Mart Survey Atl BTLDocument2 pagesVishal Mega Mart Survey Atl BTLShuvajit BiswasPas encore d'évaluation

- TCI Letter To Safran Chairman 2017-02-14Document4 pagesTCI Letter To Safran Chairman 2017-02-14marketfolly.comPas encore d'évaluation

- Latihan AdvanceDocument9 pagesLatihan AdvanceMellya KomaraPas encore d'évaluation

- Microsoft Project Training ManualDocument15 pagesMicrosoft Project Training ManualAfif Kamal Fiska100% (1)

- Design and Implementation of Real Processing in Accounting Information SystemDocument66 pagesDesign and Implementation of Real Processing in Accounting Information Systemenbassey100% (2)

- Keeney v. Larkin, 4th Cir. (2004)Document4 pagesKeeney v. Larkin, 4th Cir. (2004)Scribd Government DocsPas encore d'évaluation