Vous aimerez peut-être aussi

- Co-Operative Housing SocietyDocument29 pagesCo-Operative Housing SocietyVish Patilvs67% (3)

- Co Operative Housing SocietyDocument29 pagesCo Operative Housing Societyraj odiyarPas encore d'évaluation

- Final Account of C0-Oprative SocietyDocument22 pagesFinal Account of C0-Oprative SocietyKomalPas encore d'évaluation

- Visit To A Co Operative SocietyDocument15 pagesVisit To A Co Operative SocietySOHEL BANGI75% (4)

- Project On Co Operative Society India PDFDocument42 pagesProject On Co Operative Society India PDFRig VedPas encore d'évaluation

- A STUDY OF ACCOUNTING AND STATUTORY REQUIREMENT OF SAI KRUPA C.H.S (Nerul East)Document29 pagesA STUDY OF ACCOUNTING AND STATUTORY REQUIREMENT OF SAI KRUPA C.H.S (Nerul East)Pankaj Rathod67% (3)

- Cooperative Society M.com 2Document27 pagesCooperative Society M.com 2Shankari MaharajanPas encore d'évaluation

- Financial AccountingDocument36 pagesFinancial Accountingkhanafsha100% (1)

- Introduction To Project Report:: Shiva Credit Co-Operative Society LimitedDocument83 pagesIntroduction To Project Report:: Shiva Credit Co-Operative Society Limitedpmcmbharat264Pas encore d'évaluation

- A Study On The Urban Cooperative Banks Success and Growth in Vellore DistrictDocument4 pagesA Study On The Urban Cooperative Banks Success and Growth in Vellore DistrictSrikara AcharyaPas encore d'évaluation

- The Co-Operative Societies Rules, 1927Document33 pagesThe Co-Operative Societies Rules, 1927Muzaffar IqbalPas encore d'évaluation

- Co Operative BankDocument20 pagesCo Operative BankRakesh RockyPas encore d'évaluation

- Neelam ReportDocument86 pagesNeelam Reportrjjain07100% (2)

- Banking Regulation ActDocument19 pagesBanking Regulation Actgattani.swatiPas encore d'évaluation

- A Projct Report On Cooperative SocietyDocument6 pagesA Projct Report On Cooperative Societymonikaagarwalitm333073% (15)

- Effect of Taxation On Small BusinessDocument37 pagesEffect of Taxation On Small BusinessBhanu pratap singh100% (1)

- Co - Operative Banks in Kerala - An OverviewDocument27 pagesCo - Operative Banks in Kerala - An Overviewmalayali100100% (1)

- A Project Report On Taxation in IndiaDocument59 pagesA Project Report On Taxation in IndiaYash Bhagat100% (1)

- Punjab State Cooperative Bank 1 (Repaired)Document60 pagesPunjab State Cooperative Bank 1 (Repaired)DeepikaSaini75% (4)

- SEBIDocument29 pagesSEBISanjana Sen100% (1)

- Comparative Study of Home Loans of Abhyudaya Co-Operative Bank and NKGSB Co-Operative Bank .Document85 pagesComparative Study of Home Loans of Abhyudaya Co-Operative Bank and NKGSB Co-Operative Bank .meenakshi dange100% (1)

- Abhyudaya Co-Operative BankDocument58 pagesAbhyudaya Co-Operative Bankrahuldearest71% (7)

- Co Operative Banking Final ProjectDocument65 pagesCo Operative Banking Final ProjectYogi525Pas encore d'évaluation

- Loans and Advances of The Sutex Co-Opertive Bank Ltd.Document62 pagesLoans and Advances of The Sutex Co-Opertive Bank Ltd.sumesh8940% (1)

- Report On Organisation Study Cover Page1 DeekshaDocument51 pagesReport On Organisation Study Cover Page1 Deekshadeeksha jPas encore d'évaluation

- SCFS Co-Operative Society LTDDocument23 pagesSCFS Co-Operative Society LTDLïkïth Räj100% (3)

- The Surat Dist. Co-Op BankDocument94 pagesThe Surat Dist. Co-Op BankVijay Gohil0% (3)

- A Study On Retail Loans, at UTI Bank Retail Asset CentreDocument74 pagesA Study On Retail Loans, at UTI Bank Retail Asset CentreBilal Ahmad LonePas encore d'évaluation

- A Study On Credit Management at District CoDocument86 pagesA Study On Credit Management at District CoIMAM JAVOOR100% (2)

- A Comparative Study of NBFC in IndiaDocument28 pagesA Comparative Study of NBFC in IndiaGuru Prasad0% (1)

- Co Operative BankDocument76 pagesCo Operative BankGursharan Singh Anamika0% (1)

- Report On Sutex BankDocument55 pagesReport On Sutex Bankjkpatel221Pas encore d'évaluation

- SEBI Guidelines For MBDocument34 pagesSEBI Guidelines For MB9958331534100% (1)

- Project On Co-Operative Banks and Rural DevelopmentDocument52 pagesProject On Co-Operative Banks and Rural DevelopmentDileep94% (17)

- Project Report On Saraswat BankDocument49 pagesProject Report On Saraswat BankAbhijit Kumar87% (23)

- NPA PROJECT For Surat Dist Co-Op BankDocument62 pagesNPA PROJECT For Surat Dist Co-Op BankVijay Gohil33% (3)

- Steps in A Pre and Post Public IssueDocument8 pagesSteps in A Pre and Post Public Issuearmailgm100% (1)

- Project On Punjab National BankDocument86 pagesProject On Punjab National BankPrakash Singh100% (1)

- Nabard Project On Rural Development.Document44 pagesNabard Project On Rural Development.babubls100% (1)

- History of Audit in IndiaDocument4 pagesHistory of Audit in Indiapodder0% (1)

- Introduction of The Study: Meaning and Importance of FinanceDocument69 pagesIntroduction of The Study: Meaning and Importance of FinanceJeevitha MuruganPas encore d'évaluation

- Co OperativeDocument220 pagesCo OperativeMeenukutty MeenuPas encore d'évaluation

- 3.1 Industry Profile 3.1.1 Banking Industry in IndiaDocument25 pages3.1 Industry Profile 3.1.1 Banking Industry in IndiaUma MaheshwariPas encore d'évaluation

- ProjectDocument70 pagesProjectnramkumar00775% (4)

- Sutex Co-Op Bank ProjectDocument49 pagesSutex Co-Op Bank ProjectHinal Prajapati100% (4)

- A Study On Loans and Advances at Pragathi Krishna Gramin Bank Bangalore PDFDocument101 pagesA Study On Loans and Advances at Pragathi Krishna Gramin Bank Bangalore PDFMANI SAGAR SPas encore d'évaluation

- Ranchi University M.com SyllabusDocument42 pagesRanchi University M.com SyllabusFarhan AkhtarPas encore d'évaluation

- Project On Apex BankDocument32 pagesProject On Apex BankRishi Agarwal67% (3)

- Tax PlanningDocument109 pagesTax PlanningrahulPas encore d'évaluation

- Advance Payment of TaxDocument35 pagesAdvance Payment of TaxTrapti Garg Goyal0% (1)

- AmalgamationDocument35 pagesAmalgamationKaran VyasPas encore d'évaluation

- Regional Rural Banks of India: Evolution, Performance and ManagementD'EverandRegional Rural Banks of India: Evolution, Performance and ManagementPas encore d'évaluation

- Co-Op Soc.Document19 pagesCo-Op Soc.NainaPas encore d'évaluation

- Project On Co-Operative Society - IndiaDocument42 pagesProject On Co-Operative Society - IndiaNikul Kanaiya67% (36)

- Chapter-16 Audit of Co-Operative Societies: CA Ravi Taori Co-Op SocietyDocument8 pagesChapter-16 Audit of Co-Operative Societies: CA Ravi Taori Co-Op SocietyArpit ShuklaPas encore d'évaluation

- RFBTDocument18 pagesRFBTHalsey Shih TzuPas encore d'évaluation

- 68 Managemsnt and Leg DiscriptiveDocument10 pages68 Managemsnt and Leg DiscriptiveParames MuruganPas encore d'évaluation

- Arvind FaDocument43 pagesArvind FaSayliKadvePas encore d'évaluation

- Cooperative Housing Society Byculla Final TMDDocument73 pagesCooperative Housing Society Byculla Final TMDYogita TokePas encore d'évaluation

- The Cooperative Societies Act, 1925Document18 pagesThe Cooperative Societies Act, 1925Muzaffar IqbalPas encore d'évaluation

- Objectives of StudiesDocument6 pagesObjectives of Studiesvenkynaidu100% (1)

- RM ProjectDocument45 pagesRM Projectvenkynaidu100% (1)

- Index: Sr. No. Description 1 2 3Document63 pagesIndex: Sr. No. Description 1 2 3venkynaiduPas encore d'évaluation

- Introduction To International Standards On AuditingDocument30 pagesIntroduction To International Standards On Auditingvenkynaidu100% (1)

- Chapter No.1 Introduction To International Standards On AuditingDocument34 pagesChapter No.1 Introduction To International Standards On AuditingvenkynaiduPas encore d'évaluation

- Project Report On "Working Capital On QCML Company": Miss. Micheal Augustine Mary Roll No: 18Document60 pagesProject Report On "Working Capital On QCML Company": Miss. Micheal Augustine Mary Roll No: 18venkynaiduPas encore d'évaluation

- Project Report On HR PoliciesDocument58 pagesProject Report On HR PoliciesRJ Rishabh Tyagi86% (21)

- Mcom Part 2 Project of Mvat Cen VatDocument53 pagesMcom Part 2 Project of Mvat Cen Vatrani26oct100% (4)

- Serial No NoDocument27 pagesSerial No NovenkynaiduPas encore d'évaluation

- Index: Sr. No. Description 1 2 3Document63 pagesIndex: Sr. No. Description 1 2 3venkynaiduPas encore d'évaluation

- A026 2010 Iaasb Handbook Isa 520Document8 pagesA026 2010 Iaasb Handbook Isa 520rangga0411Pas encore d'évaluation

- F A ProjectDocument46 pagesF A ProjectvenkynaiduPas encore d'évaluation

- F A ProjectDocument46 pagesF A ProjectvenkynaiduPas encore d'évaluation

- Project Report: Masters of Commerce Degree Semester-3 ACADEMIC YEAR: 2015-16 Submitted byDocument41 pagesProject Report: Masters of Commerce Degree Semester-3 ACADEMIC YEAR: 2015-16 Submitted byvenkynaiduPas encore d'évaluation

- Sole TradingDocument15 pagesSole TradingvenkynaiduPas encore d'évaluation

- AuditDocument60 pagesAuditvenkynaiduPas encore d'évaluation

- Financial Statement On Sole Trading Ok ProjectDocument51 pagesFinancial Statement On Sole Trading Ok Projectvenkynaidu57% (14)

- 1 Messages Reply To: To: CC:: ResumeDocument1 page1 Messages Reply To: To: CC:: ResumevenkynaiduPas encore d'évaluation

- Assignment AnswersDocument4 pagesAssignment AnswersvenkynaiduPas encore d'évaluation

- RM 1Document44 pagesRM 1venkynaiduPas encore d'évaluation

- Project On Finalization of Partnership FirmDocument38 pagesProject On Finalization of Partnership Firmvenkynaidu67% (3)

- Financial Statement On Sole Trading Ok ProjectDocument51 pagesFinancial Statement On Sole Trading Ok Projectvenkynaidu57% (14)

- Coperative Society FinalDocument41 pagesCoperative Society Finalvenkynaidu100% (1)

- Public Private PartnershipDocument23 pagesPublic Private PartnershipvenkynaiduPas encore d'évaluation

- Marginal Costing PROJECTDocument38 pagesMarginal Costing PROJECTvenkynaidu67% (9)

- FINAL DONE Sem 2 PPP SM ProjectDocument44 pagesFINAL DONE Sem 2 PPP SM Projectraj odiyarPas encore d'évaluation

- Marginal Costing PROJECTDocument38 pagesMarginal Costing PROJECTvenkynaidu67% (9)

- Foreign Capital FlowsDocument8 pagesForeign Capital Flowsraj odiyarPas encore d'évaluation

- Project Report: Masters of Commerce Degree Semester-2 ACADEMIC YEAR: 2015-16 Submitted byDocument47 pagesProject Report: Masters of Commerce Degree Semester-2 ACADEMIC YEAR: 2015-16 Submitted byvenkynaidu100% (1)

- Accounting CycleDocument4 pagesAccounting CycleAirish A. MicarandayoPas encore d'évaluation

- Continue PDFDocument26 pagesContinue PDFDanny FarrukhPas encore d'évaluation

- The Burger House: (Business Plan) Submitted To: MR - Shree Ranjan Wasti Kathmandu College of ManagementDocument31 pagesThe Burger House: (Business Plan) Submitted To: MR - Shree Ranjan Wasti Kathmandu College of ManagementSEERAT IMTIAZ100% (1)

- Profile of PandayanDocument26 pagesProfile of PandayanmpdoPas encore d'évaluation

- Club Accounts: by Mr. Conor Foley, B. Comm., Macc., Fca, Dip Ifr Examiner: Foundation Financial AccountingDocument15 pagesClub Accounts: by Mr. Conor Foley, B. Comm., Macc., Fca, Dip Ifr Examiner: Foundation Financial AccountingGodfrey MakurumurePas encore d'évaluation

- Financial Aspects of Spotify Streaming Model: October 2020Document6 pagesFinancial Aspects of Spotify Streaming Model: October 2020Gaurav ManiyarPas encore d'évaluation

- F6 - IPRO - 2021 - Mock 1 - QuestionsDocument23 pagesF6 - IPRO - 2021 - Mock 1 - QuestionsHussein SeetalPas encore d'évaluation

- Lecture-13 Standard Costing Review ProblemDocument22 pagesLecture-13 Standard Costing Review ProblemNazmul-Hassan Sumon67% (3)

- Coc Model Level Ivpractical: SolutionDocument2 pagesCoc Model Level Ivpractical: SolutionAye TubePas encore d'évaluation

- RWE Annual Report 2011Document240 pagesRWE Annual Report 2011eboskovskiPas encore d'évaluation

- Financial Accounting 7th Edition Harrison Solutions ManualDocument74 pagesFinancial Accounting 7th Edition Harrison Solutions ManualBrandonCoopergnzxy100% (16)

- Annual Budget BalogñonanDocument54 pagesAnnual Budget Balogñonanjenny lyn toledoPas encore d'évaluation

- Flash Memory ExcelDocument4 pagesFlash Memory ExcelHarshita SethiyaPas encore d'évaluation

- Schedule of Repayment of Term Loan With Principal and Interest Break-UpDocument14 pagesSchedule of Repayment of Term Loan With Principal and Interest Break-UpaejosePas encore d'évaluation

- ACC707 Auditing Assurance Services AssignmentDocument2 pagesACC707 Auditing Assurance Services AssignmentHaris AliPas encore d'évaluation

- Department of Accountancy: Holy Angel UniversityDocument14 pagesDepartment of Accountancy: Holy Angel UniversityMichaella ManlapazPas encore d'évaluation

- Review of Income Tax Reporting For Individuals & Corporate TaxpayersDocument159 pagesReview of Income Tax Reporting For Individuals & Corporate TaxpayersRyan Christian BalanquitPas encore d'évaluation

- Coc Level 1-4Document149 pagesCoc Level 1-4eferem100% (14)

- Basics of Accounting TermsDocument11 pagesBasics of Accounting TermsFarhat Ullah KhanPas encore d'évaluation

- Assessment 1 - Assignment 1Document5 pagesAssessment 1 - Assignment 1Ten NinePas encore d'évaluation

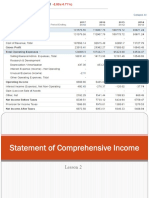

- Lesson 2 Statement of Comprehensive IncomeDocument23 pagesLesson 2 Statement of Comprehensive IncomePaulette Sarno80% (5)

- BSBFIM501 Manage Budgets and Financial Plans Learner Instructions 2 (Implement Financial Management Approaches)Document7 pagesBSBFIM501 Manage Budgets and Financial Plans Learner Instructions 2 (Implement Financial Management Approaches)vipulclasses01 vipulclassPas encore d'évaluation

- Suggested Solutions/ Answers - Fall 2018 Examinations Financial Accounting (M4) - Managerial Level-2Document6 pagesSuggested Solutions/ Answers - Fall 2018 Examinations Financial Accounting (M4) - Managerial Level-2Shiza ArifPas encore d'évaluation

- 2 Financial Accounting ReportingDocument5 pages2 Financial Accounting ReportingBizness Zenius HantPas encore d'évaluation

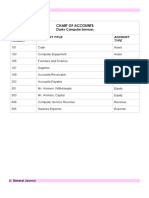

- ACTIVITY 2. Setting Up of Chart of Accounts and Journalizing of Entries ActivityDocument2 pagesACTIVITY 2. Setting Up of Chart of Accounts and Journalizing of Entries Activityfernandez 4Pas encore d'évaluation

- FAR Problem Quiz 1Document6 pagesFAR Problem Quiz 1Ednalyn CruzPas encore d'évaluation

- TOR IndonesiaDocument37 pagesTOR IndonesiaAdit Ramdhani0% (1)

- Herbal GutkaDocument8 pagesHerbal GutkaKamlesh Rajput0% (1)

- Compa Ny Profile - Bata India LTD.: Amarbir - Anand@bata - Co.in WWW - Bata.inDocument5 pagesCompa Ny Profile - Bata India LTD.: Amarbir - Anand@bata - Co.in WWW - Bata.inSachin Kumar BassiPas encore d'évaluation

- TEMPLATE Financial Projections WorkbookDocument22 pagesTEMPLATE Financial Projections WorkbookFrancois ChampenoisPas encore d'évaluation