Vous aimerez peut-être aussi

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

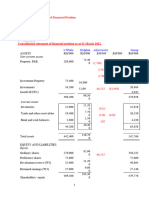

- Tutorial 4 Consolidated FS I (CBS) (A)Document10 pagesTutorial 4 Consolidated FS I (CBS) (A)fooyy8Pas encore d'évaluation

- Indigo ProspectusDocument557 pagesIndigo Prospectusvbt999123yahoo100% (1)

- Foundations of Financial Management Canadian 8th Edition Block Test BankDocument25 pagesFoundations of Financial Management Canadian 8th Edition Block Test BankJenniferDiazqmfsi100% (54)

- Final Exam Spring 2021 - Hikmet - IsgenderovDocument15 pagesFinal Exam Spring 2021 - Hikmet - IsgenderovAydin NajafovPas encore d'évaluation

- 11 - Working Capital ManagementDocument39 pages11 - Working Capital Managementrajeshkandel345Pas encore d'évaluation

- Daimler AG Closed USD 21168 Millions Revolving Credit or Bridge Loan (RC or Bridge)Document3 pagesDaimler AG Closed USD 21168 Millions Revolving Credit or Bridge Loan (RC or Bridge)Othman Alaoui Mdaghri BenPas encore d'évaluation

- CBM Lopez Moghadasi Moustahsine KrishnakumarDocument21 pagesCBM Lopez Moghadasi Moustahsine KrishnakumarkhalidibrahimalsafadiPas encore d'évaluation

- Handout - Chapter 9 - NPV and Other Investment CriteriaDocument65 pagesHandout - Chapter 9 - NPV and Other Investment CriteriaNhư Quỳnh Dương ThịPas encore d'évaluation

- Comprehensive Guide To Real Estate InvestmentDocument156 pagesComprehensive Guide To Real Estate Investmentpllssdsd100% (2)

- Absorption & Marginal CostingDocument10 pagesAbsorption & Marginal CostingFaraz SiddiquiPas encore d'évaluation

- Corporate Finance Chapter 26Document83 pagesCorporate Finance Chapter 26billy930% (1)

- DHFL CrisisDocument2 pagesDHFL CrisisCritiPas encore d'évaluation

- Stockholder's EquityDocument8 pagesStockholder's EquityKaila stinerPas encore d'évaluation

- Chapter Four:Capital Budgeting: 4.2. Project ClassificationsDocument17 pagesChapter Four:Capital Budgeting: 4.2. Project Classificationssamuel kebedePas encore d'évaluation

- Compiled 202 204 206 208 210 Bcom Iv Even 2020Document237 pagesCompiled 202 204 206 208 210 Bcom Iv Even 2020Dhanush ShettyPas encore d'évaluation

- Banking Chapter NineDocument46 pagesBanking Chapter NinefikremariamPas encore d'évaluation

- MCQ On International Finance PDFDocument16 pagesMCQ On International Finance PDFArfath BaigPas encore d'évaluation

- Engro FertilizerDocument31 pagesEngro FertilizerHussain Jummani100% (3)

- Reaction Paper No 5 (Role of Business To Shareholders)Document1 pageReaction Paper No 5 (Role of Business To Shareholders)ANGELINE LABBUTANPas encore d'évaluation

- 5.chapter 5 - Multinational Capital BudgetingDocument26 pages5.chapter 5 - Multinational Capital BudgetingLê Quỳnh ChiPas encore d'évaluation

- The Heston Model: Hui Gong, UCLDocument12 pagesThe Heston Model: Hui Gong, UCLharish dassPas encore d'évaluation

- Financial Reporting: Final Course Study Material P 1Document20 pagesFinancial Reporting: Final Course Study Material P 1vandv printsPas encore d'évaluation

- Quiz On The Accounting EquationDocument5 pagesQuiz On The Accounting EquationCeejay MancillaPas encore d'évaluation

- HW 2 - Ch03 P15 Build A Model - HrncarDocument2 pagesHW 2 - Ch03 P15 Build A Model - HrncarsusikralovaPas encore d'évaluation

- Corporate Finance NotesDocument24 pagesCorporate Finance NotesAkash Gupta100% (1)

- Antony Waste Handling Cell Limited - DRHP - 20200930183544Document428 pagesAntony Waste Handling Cell Limited - DRHP - 20200930183544SubscriptionPas encore d'évaluation

- Mergers and Acquisitions Toolkit - Overview and ApproachDocument55 pagesMergers and Acquisitions Toolkit - Overview and ApproachMaria AngelPas encore d'évaluation

- 03 Fischer10e SM Ch03 FinalDocument99 pages03 Fischer10e SM Ch03 Finalvivi anggi100% (1)

- Business Canvas and Value Proposition Design TemplateDocument5 pagesBusiness Canvas and Value Proposition Design TemplateggpinedaPas encore d'évaluation

- Report On Sumeru Securities PVT LTD 2Document18 pagesReport On Sumeru Securities PVT LTD 2sagar timilsinaPas encore d'évaluation