Vous aimerez peut-être aussi

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (894)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Phase 1 & 2: 50% OFF On NABARD Courses Code: NABARD50Document23 pagesPhase 1 & 2: 50% OFF On NABARD Courses Code: NABARD50SaumyaPas encore d'évaluation

- Introduction to Derivatives: Risk Management, Trading Efficiency and ParticipantsDocument82 pagesIntroduction to Derivatives: Risk Management, Trading Efficiency and Participantskware215Pas encore d'évaluation

- Share CapitalDocument58 pagesShare CapitalCyreene RodelasPas encore d'évaluation

- Space MatrixDocument9 pagesSpace MatrixKrisca DepalubosPas encore d'évaluation

- Managerial Accounting Reviewer PreFinalsxDocument10 pagesManagerial Accounting Reviewer PreFinalsxGenelyn BalancarPas encore d'évaluation

- MR Ranjit SinghDocument77 pagesMR Ranjit SinghMonu MehanPas encore d'évaluation

- The Institute of Chartered Accountants of IndiaDocument17 pagesThe Institute of Chartered Accountants of IndiaSATYANARAYANA MOTAMARRIPas encore d'évaluation

- 3rd Periodical Exam - FABM1Document6 pages3rd Periodical Exam - FABM1Arven DulayPas encore d'évaluation

- Investment in PSX Project. Investment Portfolio Management.: Group Members. Rabee Shahzad Zahid Ch. Arslan WattooDocument14 pagesInvestment in PSX Project. Investment Portfolio Management.: Group Members. Rabee Shahzad Zahid Ch. Arslan WattooAhmad MalikPas encore d'évaluation

- RBL Bank Ltd. BUYDocument7 pagesRBL Bank Ltd. BUYpajadhavPas encore d'évaluation

- MAF653 TEST 1 NOV 2022 QuestionDocument11 pagesMAF653 TEST 1 NOV 2022 QuestionAyunieazahaPas encore d'évaluation

- Interview Questions: Satyadev KalraDocument8 pagesInterview Questions: Satyadev Kalrasatyadev_146Pas encore d'évaluation

- IOWA HARNESS HORSEMENS ASSOCIATION PAC - 9737 - DR2 - SummaryDocument1 pageIOWA HARNESS HORSEMENS ASSOCIATION PAC - 9737 - DR2 - SummaryZach EdwardsPas encore d'évaluation

- AIESEC Benak Account Balances 2022-06-20Document2 pagesAIESEC Benak Account Balances 2022-06-20sadi raniaPas encore d'évaluation

- Project Financing: Structure, Risks & Real CasesDocument23 pagesProject Financing: Structure, Risks & Real CasesTushar AtreyPas encore d'évaluation

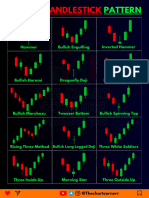

- Chart Pattern Cheat Sheet-1Document18 pagesChart Pattern Cheat Sheet-1YASHANK VISHWAKARMAPas encore d'évaluation

- Cox & Kings (CNKLIM) : Peak Season of HBR Drives ToplineDocument6 pagesCox & Kings (CNKLIM) : Peak Season of HBR Drives ToplineDarshan MaldePas encore d'évaluation

- (Jointly Administered) The Rhodes Companies, LLC, Aka "Rhodes Homes," Et At.Document105 pages(Jointly Administered) The Rhodes Companies, LLC, Aka "Rhodes Homes," Et At.Chapter 11 DocketsPas encore d'évaluation

- Startups ShabdkoshDocument89 pagesStartups ShabdkoshRujuta Kulkarni0% (1)

- Karvy Fraud Shivansh - 3438Document7 pagesKarvy Fraud Shivansh - 34383438SHIVANSH AggarwalPas encore d'évaluation

- Negotiable Instruments AIB PDFDocument488 pagesNegotiable Instruments AIB PDFgomerpiles100% (2)

- Pro Forma Financial StatementsDocument13 pagesPro Forma Financial StatementsAlex liaoPas encore d'évaluation

- What is Share Capital? Types and DefinitionsDocument1 pageWhat is Share Capital? Types and DefinitionsJuhaima BayaoPas encore d'évaluation

- Law Project - The Negotiable Instrument Act - RevisedV1Document48 pagesLaw Project - The Negotiable Instrument Act - RevisedV1Teena Varma100% (3)

- L1R41 - Annotated - LiveDocument52 pagesL1R41 - Annotated - LiveAlex PaulPas encore d'évaluation

- UK Bank ListDocument5 pagesUK Bank ListPV BhaskarPas encore d'évaluation

- Account Transfer Form: Fax Cover SheetDocument6 pagesAccount Transfer Form: Fax Cover SheetJitendra SharmaPas encore d'évaluation

- Skolkovo InvestmentsDocument14 pagesSkolkovo InvestmentsSegah MeerPas encore d'évaluation

- Financial Performance of Rinl Using Financial Ratios and Comparision With Tata, Sail and JSWDocument6 pagesFinancial Performance of Rinl Using Financial Ratios and Comparision With Tata, Sail and JSWNIHANTH MALAPATIPas encore d'évaluation

- Financial Support StudyDocument101 pagesFinancial Support Studypriyanka repalle100% (2)