Vous aimerez peut-être aussi

- Digest-Sesbreno Vs CADocument2 pagesDigest-Sesbreno Vs CAKennethRobles100% (3)

- Ang Tek Lian Vs CADocument2 pagesAng Tek Lian Vs CALee Somar100% (1)

- Metrobank Vs CabilzoDocument1 pageMetrobank Vs CabilzoSheilah Mae PadallaPas encore d'évaluation

- Metropolitan Bank v. CA NEGO CASE DIGESTDocument4 pagesMetropolitan Bank v. CA NEGO CASE DIGESTCoreine Valledor-Sarraga100% (2)

- Philippine Education Co v. Mauricio Soriano, Et Al.Document2 pagesPhilippine Education Co v. Mauricio Soriano, Et Al.Katrina PerezPas encore d'évaluation

- Juanita Salas Vs Court of Appeals (Negotiable Instruments Law)Document1 pageJuanita Salas Vs Court of Appeals (Negotiable Instruments Law)Lance ClementePas encore d'évaluation

- Digest - Wong vs. CADocument1 pageDigest - Wong vs. CAPaul Vincent Cunanan100% (1)

- Metrobank vs. CA (GR No 88866)Document1 pageMetrobank vs. CA (GR No 88866)Katharina CantaPas encore d'évaluation

- Checks and Negotiable Instruments Case BriefsDocument3 pagesChecks and Negotiable Instruments Case BriefsMaria Anna M Legaspi50% (2)

- Metropol Vs Sambok Case DigestDocument1 pageMetropol Vs Sambok Case DigestRj2100% (1)

- PNB V Manila Oil Refining CoDocument2 pagesPNB V Manila Oil Refining Cosmtm06100% (3)

- Pal V Ca Nego CASE DIGEST WITH FULL TEXTDocument5 pagesPal V Ca Nego CASE DIGEST WITH FULL TEXTCoreine Valledor-SarragaPas encore d'évaluation

- Case Digest NIL - Without Rigor YetDocument3 pagesCase Digest NIL - Without Rigor YetKik EtcPas encore d'évaluation

- De Ocampo Vs Gatchalian DigestDocument1 pageDe Ocampo Vs Gatchalian DigestChic PabalanPas encore d'évaluation

- International Corporate Bank V GuecoDocument2 pagesInternational Corporate Bank V Guecovirvsha IndolozPas encore d'évaluation

- PNB V PicornellDocument2 pagesPNB V PicornellJassy Bustamante100% (3)

- Travel-On Vs CADocument1 pageTravel-On Vs CAAnonymous NiKZKWgKqPas encore d'évaluation

- Westmont Bank Liable for ForgeryDocument1 pageWestmont Bank Liable for ForgeryEmelie Marie Diez100% (1)

- Digest - Bataan Cigar vs. CADocument1 pageDigest - Bataan Cigar vs. CAPaul Vincent Cunanan100% (1)

- MATERIAL ALTERATION DISCHARGES NEGOTIABLE INSTRUMENTDocument3 pagesMATERIAL ALTERATION DISCHARGES NEGOTIABLE INSTRUMENTLenie SanchezPas encore d'évaluation

- DIGEST Republic Bank V Ebrada PDFDocument1 pageDIGEST Republic Bank V Ebrada PDFAnonymous gy7lIr8Pas encore d'évaluation

- Sps. Evangelista Vs Mercator Finance CorpDocument2 pagesSps. Evangelista Vs Mercator Finance CorpToni CalsadoPas encore d'évaluation

- NIL Complitation of Case DigestsDocument50 pagesNIL Complitation of Case DigestsGalilee Paraiso Patdu100% (1)

- Republic Planters Bank Vs CA 216 SCRA 738Document3 pagesRepublic Planters Bank Vs CA 216 SCRA 738Chino CabreraPas encore d'évaluation

- Development Bank vs. Sima WeiDocument2 pagesDevelopment Bank vs. Sima WeiMichelle Montenegro - Araujo100% (1)

- Aglibot V Santia DigestDocument1 pageAglibot V Santia DigestJoshua LanzonPas encore d'évaluation

- Juanita Salas vs CA et al Promissory Note DisputeDocument2 pagesJuanita Salas vs CA et al Promissory Note DisputeMary Joyce Lacambra Aquino100% (1)

- Philippine Education Corporation Vs SorianoDocument6 pagesPhilippine Education Corporation Vs SorianoSo ULPas encore d'évaluation

- PBCom Vs Aruego NEGO DigestDocument2 pagesPBCom Vs Aruego NEGO DigestMary LouisePas encore d'évaluation

- Allied Banking Corporation V Court of Appeals DigestDocument2 pagesAllied Banking Corporation V Court of Appeals DigestIna Villarica67% (3)

- BPI V CADocument2 pagesBPI V CARubyPas encore d'évaluation

- Samsung Construction vs. FEBTC Case DigestDocument3 pagesSamsung Construction vs. FEBTC Case Digestkikhay11Pas encore d'évaluation

- Patrimonio v. GutierrezDocument2 pagesPatrimonio v. GutierrezNikkiZai100% (1)

- RCBC vs. Odrada CDDocument3 pagesRCBC vs. Odrada CDMarco LucmanPas encore d'évaluation

- Metropolitan Bank vs. CA (194 SCRA 169, 18 February 1991)Document2 pagesMetropolitan Bank vs. CA (194 SCRA 169, 18 February 1991)Howard ClarkPas encore d'évaluation

- 17 - de Ocampo V GatchalianDocument2 pages17 - de Ocampo V Gatchaliansmtm06100% (1)

- NEGO - 30. Far East vs. Gold Palace Jewelry, G.R. No. 168274Document2 pagesNEGO - 30. Far East vs. Gold Palace Jewelry, G.R. No. 168274annedefranco50% (4)

- N-08-02 Consolidated Plywood V IFC LeasingDocument2 pagesN-08-02 Consolidated Plywood V IFC LeasingMalcolm Cruz100% (1)

- Philippine Bank of Commerce v. AruegoDocument1 pagePhilippine Bank of Commerce v. AruegoPre PacionelaPas encore d'évaluation

- Bank liability of endorser released without notice of dishonorDocument2 pagesBank liability of endorser released without notice of dishonorEileen Kay A. MañiboPas encore d'évaluation

- ICB vs. Gueco: No Fraud in Requiring Signing of Joint Motion to DismissDocument2 pagesICB vs. Gueco: No Fraud in Requiring Signing of Joint Motion to DismissAlan GultiaPas encore d'évaluation

- Digest BANK OF AMERICA NT & SA vs. PHILIPPINE RACING CLUB INCORPORATEDDocument2 pagesDigest BANK OF AMERICA NT & SA vs. PHILIPPINE RACING CLUB INCORPORATEDemolotrabPas encore d'évaluation

- Ilusorio Vs CA DigestDocument1 pageIlusorio Vs CA DigestSansa StarkPas encore d'évaluation

- THE INTERNATIONAL CORPORATE BANK Vs GuecoDocument1 pageTHE INTERNATIONAL CORPORATE BANK Vs GuecoAlexir MendozaPas encore d'évaluation

- Samsung Construction Co. Phils, Inc. vs. FEBTC, Et. Al. G.R. No. 129015Document2 pagesSamsung Construction Co. Phils, Inc. vs. FEBTC, Et. Al. G.R. No. 129015Jay EmPas encore d'évaluation

- Court rules material alteration invalidates checkDocument2 pagesCourt rules material alteration invalidates checkTerence Tomol100% (1)

- JAI-ALAI VS BANK OF THE PHILIPPINE ISLANDS FORGED CHECK DEPOSIT DISPUTEDocument1 pageJAI-ALAI VS BANK OF THE PHILIPPINE ISLANDS FORGED CHECK DEPOSIT DISPUTEmargaserrano100% (1)

- Philippine Education Co Vs SorianoDocument2 pagesPhilippine Education Co Vs SorianoMon Che100% (1)

- Associated Bank V CA DigestDocument1 pageAssociated Bank V CA DigestSolomon Malinias BugatanPas encore d'évaluation

- Dino v. Judal-LootDocument3 pagesDino v. Judal-LootAntonJohnVincentFriasPas encore d'évaluation

- Asian Banking Corporation vs. Juan JavierDocument2 pagesAsian Banking Corporation vs. Juan JavierMichelle Montenegro - Araujo100% (1)

- Loreto D. de La Victoria V Hon. Jose P. Burgos G.R. No. 111190 June 27, 1995Document2 pagesLoreto D. de La Victoria V Hon. Jose P. Burgos G.R. No. 111190 June 27, 1995Angela Louise Sabaoan100% (1)

- Vaca Vs People (Digest)Document1 pageVaca Vs People (Digest)Glorious El Domine100% (1)

- Philippine Education Co. v. Soriano Money Order RulingDocument1 pagePhilippine Education Co. v. Soriano Money Order RulingLiaa AquinoPas encore d'évaluation

- Chan Wan v. Tan Kim DigestDocument3 pagesChan Wan v. Tan Kim Digestkathrynmaydeveza100% (2)

- FEBTC vs. Querimit ruling on CD paymentDocument1 pageFEBTC vs. Querimit ruling on CD paymentFayda Cariaga100% (3)

- de La Victoria Vs Burgos 245 Scra 374Document10 pagesde La Victoria Vs Burgos 245 Scra 374Mp CasPas encore d'évaluation

- 56 Metropol Vs SambokDocument3 pages56 Metropol Vs SambokCharm Divina LascotaPas encore d'évaluation

- NEGO - Holder - de Ocampo v. GatchalianDocument2 pagesNEGO - Holder - de Ocampo v. GatchalianPerkymePas encore d'évaluation

- Negotiable Instruments Law - NotesDocument57 pagesNegotiable Instruments Law - Notesstubborn_dawg100% (7)

- 162 Agabon vs. NLRCDocument149 pages162 Agabon vs. NLRCMaria Anna M LegaspiPas encore d'évaluation

- Danube Dam CaseDocument81 pagesDanube Dam CaseVince Llamazares LupangoPas encore d'évaluation

- WPP MKTG vs. GaleraDocument2 pagesWPP MKTG vs. GaleraMaria Anna M Legaspi100% (2)

- FULL Olympia International Vs CADocument14 pagesFULL Olympia International Vs CAMaria Anna M LegaspiPas encore d'évaluation

- FULL Cabrera vs. TianoDocument7 pagesFULL Cabrera vs. TianoMaria Anna M LegaspiPas encore d'évaluation

- Ang Yu Asuncion Vs CADocument16 pagesAng Yu Asuncion Vs CAJorace Tena LampaPas encore d'évaluation

- FULL Tambunting, Jr. vs. Sumabat PDFDocument8 pagesFULL Tambunting, Jr. vs. Sumabat PDFMaria Anna M LegaspiPas encore d'évaluation

- FULL Permanent Savings vs. VelardeDocument17 pagesFULL Permanent Savings vs. VelardeMaria Anna M LegaspiPas encore d'évaluation

- FULL Republic vs. BañezDocument30 pagesFULL Republic vs. BañezMaria Anna M LegaspiPas encore d'évaluation

- FULL Ramos vs. CondezDocument7 pagesFULL Ramos vs. CondezMaria Anna M LegaspiPas encore d'évaluation

- FULL Philippine National Bank vs. OseteDocument8 pagesFULL Philippine National Bank vs. OseteMaria Anna M LegaspiPas encore d'évaluation

- FULL Ledesma vs. CADocument8 pagesFULL Ledesma vs. CAMaria Anna M LegaspiPas encore d'évaluation

- CDSJL vs. ROSA-MERISDocument1 pageCDSJL vs. ROSA-MERISMaria Anna M Legaspi0% (1)

- FULL Banaga vs. MajaduconDocument17 pagesFULL Banaga vs. MajaduconMaria Anna M LegaspiPas encore d'évaluation

- FULL Camarines Sur IV Electric Cooperative, Inc. vs. AquinoDocument18 pagesFULL Camarines Sur IV Electric Cooperative, Inc. vs. AquinoMaria Anna M LegaspiPas encore d'évaluation

- CASE DIGEST: Caballes vs. DARDocument2 pagesCASE DIGEST: Caballes vs. DARMaria Anna M Legaspi100% (4)

- Antonio v. MoralesDocument7 pagesAntonio v. MoralesAnonymous P5vqjUdmLyPas encore d'évaluation

- CASE DIGEST SIOL v. ASUNCIONDocument2 pagesCASE DIGEST SIOL v. ASUNCIONMaria Anna M LegaspiPas encore d'évaluation

- CASE DIGEST: Villaviza Vs PanganibanDocument1 pageCASE DIGEST: Villaviza Vs PanganibanMaria Anna M Legaspi100% (2)

- CASE DIGEST Luna Vs AlladoDocument1 pageCASE DIGEST Luna Vs AlladoMaria Anna M LegaspiPas encore d'évaluation

- CASE DIGEST: Land Bank of The Philippines vs. BanalDocument2 pagesCASE DIGEST: Land Bank of The Philippines vs. BanalMaria Anna M LegaspiPas encore d'évaluation

- Court Rules Lack of Correct Docket Fee Deprives Court of JurisdictionDocument1 pageCourt Rules Lack of Correct Docket Fee Deprives Court of JurisdictionMaria Anna M LegaspiPas encore d'évaluation

- Case Digest - People vs. BaykerDocument1 pageCase Digest - People vs. BaykerMaria Anna M Legaspi100% (2)

- CASE DIGEST: Caballes vs. DARDocument2 pagesCASE DIGEST: Caballes vs. DARMaria Anna M Legaspi100% (4)

- Rules of Procedure For IP Rights CasesDocument20 pagesRules of Procedure For IP Rights CasesJay GarciaPas encore d'évaluation

- Coca-Cola Liable for Illegal Dismissal of Route Helpers Despite Manpower AgenciesDocument2 pagesCoca-Cola Liable for Illegal Dismissal of Route Helpers Despite Manpower AgenciesMaria Anna M Legaspi100% (1)

- Case Digest: Yrasuegui Vs PalDocument1 pageCase Digest: Yrasuegui Vs PalMaria Anna M LegaspiPas encore d'évaluation

- Case Digest: Assoc of Small Landowners vs. Sec. of Agrarian ReformDocument2 pagesCase Digest: Assoc of Small Landowners vs. Sec. of Agrarian ReformMaria Anna M Legaspi100% (3)

- 3rd Year - Agrarian Reform Syllabus 1st Sem 2017Document10 pages3rd Year - Agrarian Reform Syllabus 1st Sem 2017Maria Anna M LegaspiPas encore d'évaluation

- Full Case - Peñaranda vs. Baganga Plywood CorporationDocument16 pagesFull Case - Peñaranda vs. Baganga Plywood CorporationMaria Anna M LegaspiPas encore d'évaluation

- Daan v. Sandiganbayan, GR Nos. 163972-77, March 28, 2008Document1 pageDaan v. Sandiganbayan, GR Nos. 163972-77, March 28, 2008Jemson Ivan WalcienPas encore d'évaluation

- ATR Aircraft Performance 2Document160 pagesATR Aircraft Performance 2Nicky Holden100% (9)

- Title Seven (Termination of Employment Contract and End of Service Gratuity)Document12 pagesTitle Seven (Termination of Employment Contract and End of Service Gratuity)DrMohamed RifasPas encore d'évaluation

- Iloilo City Regulation Ordinance 2016-115Document2 pagesIloilo City Regulation Ordinance 2016-115Iloilo City CouncilPas encore d'évaluation

- MSP-EXP430F5529LP Software ManifestDocument7 pagesMSP-EXP430F5529LP Software ManifestsrikanthPas encore d'évaluation

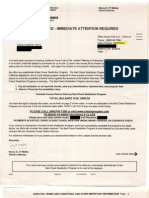

- Letter From Bad Check Restitution ProgramDocument5 pagesLetter From Bad Check Restitution Programnoahclements1877Pas encore d'évaluation

- CE Laws Ethics Contracts ReviewerDocument24 pagesCE Laws Ethics Contracts ReviewerMARY ROSE MANONGSONGPas encore d'évaluation

- Government of Andhra Pradesh Transport Department: WarningDocument1 pageGovernment of Andhra Pradesh Transport Department: WarningSwathi SumanPas encore d'évaluation

- Carno PhallogocentrismDocument9 pagesCarno PhallogocentrismmadspeterPas encore d'évaluation

- Charitable Trusts: What Are The Advantages?Document3 pagesCharitable Trusts: What Are The Advantages?Derek FoldsPas encore d'évaluation

- PNP Tel Dir 2014Document101 pagesPNP Tel Dir 2014Nowie AtanacioPas encore d'évaluation

- Motion For Stay Exh BDocument306 pagesMotion For Stay Exh BAndi MoronyPas encore d'évaluation

- (Jianfu Chen) Chinese Law Context and TransformatDocument793 pages(Jianfu Chen) Chinese Law Context and TransformatConsultingGroup Suceava100% (1)

- Antigone AnalysisDocument2 pagesAntigone AnalysisBrett Murphy0% (1)

- Crash Course On International Humanitarian LawDocument17 pagesCrash Course On International Humanitarian LawSittie Aina MunderPas encore d'évaluation

- 10 - Hyborian Age GovernmentsDocument9 pages10 - Hyborian Age GovernmentspfckainPas encore d'évaluation

- Transportation LawDocument26 pagesTransportation LawelsaPas encore d'évaluation

- Natres Full CasesDocument260 pagesNatres Full CasesN.SantosPas encore d'évaluation

- EVID 1st Set of Cases (Digests)Document22 pagesEVID 1st Set of Cases (Digests)Rachel Ann Katrina AbadPas encore d'évaluation

- Sample Booking Agreement PDFDocument1 pageSample Booking Agreement PDFgshearod2uPas encore d'évaluation

- Brokenshire Mem Hosp Vs NLRCDocument2 pagesBrokenshire Mem Hosp Vs NLRCtengloyPas encore d'évaluation

- 1385 PDFDocument70 pages1385 PDFEdmund ZinPas encore d'évaluation

- Public Interest vs. ElmaDocument1 pagePublic Interest vs. ElmaCzarina Lea D. MoradoPas encore d'évaluation

- Updated MP - Procedure To Set Up Representative Office (KPPA) in IndonesiaDocument3 pagesUpdated MP - Procedure To Set Up Representative Office (KPPA) in IndonesiaYohan AlamsyahPas encore d'évaluation

- D - Internet - Myiemorgmy - Intranet - Assets - Doc - Alldoc - Document - 5762 - Jurutera July 2014 PDFDocument47 pagesD - Internet - Myiemorgmy - Intranet - Assets - Doc - Alldoc - Document - 5762 - Jurutera July 2014 PDFDiana MashrosPas encore d'évaluation

- in Re - Petition of Al Argosino To Take The Lawyers Oath (1997)Document3 pagesin Re - Petition of Al Argosino To Take The Lawyers Oath (1997)Franch GalanzaPas encore d'évaluation

- 'Synopsis Ignou Environmental Protection & LawDocument10 pages'Synopsis Ignou Environmental Protection & Lawarun19740% (1)

- SC Rules on Rescission of Deed of Sale and Obligation to Return BusesDocument7 pagesSC Rules on Rescission of Deed of Sale and Obligation to Return BusesGino LascanoPas encore d'évaluation

- Christopher Martens v. James Shannon, Attorney General, 836 F.2d 715, 1st Cir. (1988)Document5 pagesChristopher Martens v. James Shannon, Attorney General, 836 F.2d 715, 1st Cir. (1988)Scribd Government DocsPas encore d'évaluation

- Go+tek+vs +deportation+boardDocument1 pageGo+tek+vs +deportation+boardaj salazarPas encore d'évaluation