Vous aimerez peut-être aussi

- Strengthening the Operational Pillar: The Building Blocks of World-Class Production Planning and Inventory Control SystemsD'EverandStrengthening the Operational Pillar: The Building Blocks of World-Class Production Planning and Inventory Control SystemsPas encore d'évaluation

- Cost Management: A Case for Business Process Re-engineeringD'EverandCost Management: A Case for Business Process Re-engineeringPas encore d'évaluation

- An Objective-Oriented and Product-Line-Based Manufacturing Performance MeasurementDocument11 pagesAn Objective-Oriented and Product-Line-Based Manufacturing Performance MeasurementGalih PermadiPas encore d'évaluation

- 14 Dimensions and Measures of Manufacturing PerformanceDocument6 pages14 Dimensions and Measures of Manufacturing PerformancekhmortezaPas encore d'évaluation

- Chapter 1 ObjectivesDocument9 pagesChapter 1 ObjectivesMuhammad NadeemPas encore d'évaluation

- TQM - Lean and Six SigmaDocument4 pagesTQM - Lean and Six SigmaMohamad AbrarPas encore d'évaluation

- Operation ManagementDocument6 pagesOperation ManagementLYRA MAE JOCSON- PATIAMPas encore d'évaluation

- OM With TQMDocument14 pagesOM With TQMMaridette SedaPas encore d'évaluation

- Performance Measurement. The ENAPS ApproachDocument33 pagesPerformance Measurement. The ENAPS ApproachPavel Yandyganov100% (1)

- KMBN 205 Unit 1Document12 pagesKMBN 205 Unit 1Ramesh ChandraPas encore d'évaluation

- Performance Measurement System Design - A Literature Review and Research AgendaDocument37 pagesPerformance Measurement System Design - A Literature Review and Research AgendaAlfa Riza GryffiePas encore d'évaluation

- Performance Measurement System Design A Literature Review and Research Agenda PDFDocument5 pagesPerformance Measurement System Design A Literature Review and Research Agenda PDFgvzh54d3Pas encore d'évaluation

- Performance and Evaluation of Manufacturing SystemsDocument16 pagesPerformance and Evaluation of Manufacturing SystemsMochammad Ridwan Aditya100% (1)

- Measuring Maintenance Performance) in Search For A Maintenance Productivity IndexDocument12 pagesMeasuring Maintenance Performance) in Search For A Maintenance Productivity Indexlospin1Pas encore d'évaluation

- Performance Measurement of Logistics ProcessesDocument10 pagesPerformance Measurement of Logistics ProcessesEr Suhail ManjardekarPas encore d'évaluation

- Labor Productivity Process ImprovementDocument3 pagesLabor Productivity Process ImprovementattaurrehmanPas encore d'évaluation

- Performance Measurement System Design A Literature Review and Research AgendaDocument7 pagesPerformance Measurement System Design A Literature Review and Research AgendaafdtzfutnPas encore d'évaluation

- A Cost Model of Industrial Maintenance For Profitability Analysis and Benchmarking PDFDocument17 pagesA Cost Model of Industrial Maintenance For Profitability Analysis and Benchmarking PDFHugoCabanillasPas encore d'évaluation

- 72 An Integrated Dynamic Performance Measurement System For Improving Manufacturing Competitiveness GhalayiniDocument19 pages72 An Integrated Dynamic Performance Measurement System For Improving Manufacturing Competitiveness Ghalayinimorteza kheirkhahPas encore d'évaluation

- 1-Productivity - Concept, Measurement & ImprovementDocument30 pages1-Productivity - Concept, Measurement & ImprovementShriya Gupta0% (1)

- Productivity Concepts..: A Little Different Way of Looking at ProductivityDocument8 pagesProductivity Concepts..: A Little Different Way of Looking at ProductivityArshad AbbasPas encore d'évaluation

- Bench Marking ReportDocument8 pagesBench Marking ReportNitesh SasidharanPas encore d'évaluation

- Measuring Performance of White-Collar WorkforceDocument19 pagesMeasuring Performance of White-Collar WorkforceP S Lakshmi KanthanPas encore d'évaluation

- Activity-Based Costing/management and Its Implications For Operations ManagementDocument8 pagesActivity-Based Costing/management and Its Implications For Operations ManagementYeyPas encore d'évaluation

- Activity-Based Costing System Advantages and Disadvantages: SSRN Electronic Journal July 2004Document13 pagesActivity-Based Costing System Advantages and Disadvantages: SSRN Electronic Journal July 2004sandraPas encore d'évaluation

- Key Performance Indicators MST NDocument14 pagesKey Performance Indicators MST NmscarreraPas encore d'évaluation

- KPI For Lean Implementation in Manufacturing PDFDocument14 pagesKPI For Lean Implementation in Manufacturing PDFHadee SaberPas encore d'évaluation

- Session 1 Introduction To The Subject (MTM) : Basic Terms Used in IEDocument8 pagesSession 1 Introduction To The Subject (MTM) : Basic Terms Used in IEShivangiPas encore d'évaluation

- EssayDocument7 pagesEssayCarlos Eduardo Mora CifuentesPas encore d'évaluation

- Measuring Knowledge Worker ProductivityDocument7 pagesMeasuring Knowledge Worker ProductivitydelinandrewPas encore d'évaluation

- Lean Manufacturing Literature Review PDFDocument13 pagesLean Manufacturing Literature Review PDFwzsatbcnd100% (1)

- Optimizing Maintenance Management Efforts by The Application Od TOC-a Case StudyDocument15 pagesOptimizing Maintenance Management Efforts by The Application Od TOC-a Case StudyAlex J. Tocto BustamantePas encore d'évaluation

- Implementing Lean ManufacturingDocument46 pagesImplementing Lean ManufacturingAg0% (2)

- MethodsDocument34 pagesMethodsjavarice653Pas encore d'évaluation

- Activity Based Costing TPLDocument14 pagesActivity Based Costing TPLMiguel HernandezPas encore d'évaluation

- Management Control System in Manufacturing Companies: A Case of BGI EthiopiaDocument16 pagesManagement Control System in Manufacturing Companies: A Case of BGI EthiopiaTeshome GetachewPas encore d'évaluation

- A Study On Total Quality Management and Lean Manufacturing: Through Lean Thinking ApproachDocument12 pagesA Study On Total Quality Management and Lean Manufacturing: Through Lean Thinking ApproachDian AndriliaPas encore d'évaluation

- Adding Value Through HR - Reorienting HR Measurement To Drive Business PerformanceDocument16 pagesAdding Value Through HR - Reorienting HR Measurement To Drive Business PerformanceTeddy SiuPas encore d'évaluation

- ABC System Advantages and Disadvantages ExplainedDocument13 pagesABC System Advantages and Disadvantages Explainedhardeep waliaPas encore d'évaluation

- 1-Ans. Competitiveness Is at The Core of All Strategies. Even Among Them, Priorities Tend ToDocument5 pages1-Ans. Competitiveness Is at The Core of All Strategies. Even Among Them, Priorities Tend Toajayabhi21Pas encore d'évaluation

- SSRN Id644561Document12 pagesSSRN Id644561yoyo.yy614Pas encore d'évaluation

- Activity-Based Costing System Advantages and Disadvantages: SSRN Electronic Journal July 2004Document13 pagesActivity-Based Costing System Advantages and Disadvantages: SSRN Electronic Journal July 2004bhupPas encore d'évaluation

- A Study On Total Quality Management and Lean Manufacturing: Through Lean Thinking ApproachDocument12 pagesA Study On Total Quality Management and Lean Manufacturing: Through Lean Thinking Approachhusam-h2252Pas encore d'évaluation

- Performance measurement system design process researchDocument27 pagesPerformance measurement system design process researchhakikPas encore d'évaluation

- The Activity Based Costing and Target Costing As Modern Techniques in Determination of Product CostDocument5 pagesThe Activity Based Costing and Target Costing As Modern Techniques in Determination of Product CostdevinaPas encore d'évaluation

- Key Performance Indicators KPIs and Shipping Compa PDFDocument14 pagesKey Performance Indicators KPIs and Shipping Compa PDFPramana SaputraPas encore d'évaluation

- Intangible ResourcesDocument14 pagesIntangible ResourcesPat NPas encore d'évaluation

- Marketing ProductivityDocument29 pagesMarketing ProductivityEnkhbat DulamtsetsegPas encore d'évaluation

- Performance Management Through Strategic Total Productivity OptimisationDocument10 pagesPerformance Management Through Strategic Total Productivity OptimisationVerónicaCastroPas encore d'évaluation

- AJBASR 1 PublishedDocument10 pagesAJBASR 1 PublishedAbdul WazedPas encore d'évaluation

- QFD Model DesignDocument35 pagesQFD Model Designchinthaka18389021Pas encore d'évaluation

- Project performance measurement for productivity improvementsDocument12 pagesProject performance measurement for productivity improvementsGeorge NunesPas encore d'évaluation

- A Hybrid Performance Evaluation System For Notebook Computer ODM CompaniesDocument14 pagesA Hybrid Performance Evaluation System For Notebook Computer ODM CompaniesKharis FadillahPas encore d'évaluation

- Bhasin - 2012 - Performance of Lean in Large OrganisationsDocument9 pagesBhasin - 2012 - Performance of Lean in Large OrganisationsDragan DragičevićPas encore d'évaluation

- Question # 1 (A) Define Scope and Significance of Operation ManagementDocument11 pagesQuestion # 1 (A) Define Scope and Significance of Operation ManagementHuzaifa KhalilPas encore d'évaluation

- Improving Manufacturing Productivity Through Lean TechniquesDocument4 pagesImproving Manufacturing Productivity Through Lean TechniquesVikas SuryavanshiPas encore d'évaluation

- Sustainability Measurement GINDocument36 pagesSustainability Measurement GINEliasAyoubPas encore d'évaluation

- Applying Lean Management in Textile IndustryDocument12 pagesApplying Lean Management in Textile IndustryZakria ArshadPas encore d'évaluation

- Are Smes Ready For Abc?: Owen P. Hall, Jr. Pepperdine University Charles. J. Mcpeak Pepperdine UniversityDocument12 pagesAre Smes Ready For Abc?: Owen P. Hall, Jr. Pepperdine University Charles. J. Mcpeak Pepperdine UniversitySantosh DeshpandePas encore d'évaluation

- The Role of Just-In-Time Implementation in Relation To Performance: An Exploratory StudyDocument19 pagesThe Role of Just-In-Time Implementation in Relation To Performance: An Exploratory Studyalicia whitePas encore d'évaluation

- The Roi of Employee Training and DevelopmentDocument4 pagesThe Roi of Employee Training and DevelopmentalbchilePas encore d'évaluation

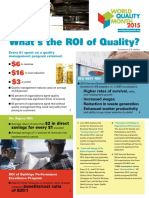

- WQM 2015 ROI of Quality Fact Sheet F PDFDocument1 pageWQM 2015 ROI of Quality Fact Sheet F PDFalbchilePas encore d'évaluation

- Hayes John-The Theory and Practice of Change Management-Chapter 4-Pp68-85Document19 pagesHayes John-The Theory and Practice of Change Management-Chapter 4-Pp68-85albchilePas encore d'évaluation

- Quality Management in Public Sector Organizations Evidence From Six EU CountriesDocument14 pagesQuality Management in Public Sector Organizations Evidence From Six EU Countriesalbchile100% (1)

- Composable Infrastructure by Dummies PDFDocument53 pagesComposable Infrastructure by Dummies PDFsajidalisajid100% (1)

- Nos Response Rate and Nonresponse BiasDocument12 pagesNos Response Rate and Nonresponse BiasalbchilePas encore d'évaluation

- Innovations in Service Strategy in Airline - KiatcharoenpolDocument5 pagesInnovations in Service Strategy in Airline - KiatcharoenpolalbchilePas encore d'évaluation

- Digital Business Transformation Framework PDFDocument16 pagesDigital Business Transformation Framework PDFalbchile100% (3)

- Navigating IT Transformation Tales From The Front LinesDocument26 pagesNavigating IT Transformation Tales From The Front LinesalbchilePas encore d'évaluation

- Quality Management Universal or Context DependentDocument22 pagesQuality Management Universal or Context DependentalbchilePas encore d'évaluation

- Quality Management Revisited PDFDocument19 pagesQuality Management Revisited PDFalbchilePas encore d'évaluation

- Hayes John-The Theory and Practice of Change Management-Chapter 4-Pp68-85Document19 pagesHayes John-The Theory and Practice of Change Management-Chapter 4-Pp68-85albchilePas encore d'évaluation

- Assessing The Effectiveness of Quality Management in A Global ContextDocument16 pagesAssessing The Effectiveness of Quality Management in A Global ContextalbchilePas encore d'évaluation

- Quality Management and Quality Practice Perspectives On History and FutureDocument29 pagesQuality Management and Quality Practice Perspectives On History and FuturealbchilePas encore d'évaluation

- The Role of Quality Managers in Contemporary OrganisationsDocument13 pagesThe Role of Quality Managers in Contemporary OrganisationsalbchilePas encore d'évaluation

- The Willingness of Professionals To Contribute To Their Organisation's CertificationDocument18 pagesThe Willingness of Professionals To Contribute To Their Organisation's CertificationalbchilePas encore d'évaluation

- Quality Strategy For Transformation A Case StudyDocument18 pagesQuality Strategy For Transformation A Case StudyalbchilePas encore d'évaluation

- Approaches To Quality Management at European LevelDocument11 pagesApproaches To Quality Management at European LevelalbchilePas encore d'évaluation

- Developing Strategic Continuous Improvement Capability - Bessant FrancisDocument24 pagesDeveloping Strategic Continuous Improvement Capability - Bessant FrancisalbchilePas encore d'évaluation

- Continuous Process Improvement Using Business Process Execution MeasuresDocument29 pagesContinuous Process Improvement Using Business Process Execution MeasuresalbchilePas encore d'évaluation

- Learning To Evolve A Review of Contemporary Lean - Hines Holweg RichDocument52 pagesLearning To Evolve A Review of Contemporary Lean - Hines Holweg Richalbchile100% (1)

- Continuous improvement essential criteriaDocument28 pagesContinuous improvement essential criteriaalbchilePas encore d'évaluation

- Modeling Continuous Improvement Service - Milner Savage PDFDocument24 pagesModeling Continuous Improvement Service - Milner Savage PDFalbchilePas encore d'évaluation

- Incremental Innovation in Services Through Continuous Improvement - AudretschDocument11 pagesIncremental Innovation in Services Through Continuous Improvement - AudretschalbchilePas encore d'évaluation

- Service Quality Models A Review - SethDocument53 pagesService Quality Models A Review - SethalbchilePas encore d'évaluation

- Impact of TQM On Org PerformanceDocument20 pagesImpact of TQM On Org PerformancealbchilePas encore d'évaluation

- The Role of Performance Measurement in Continuous Improvement - BondDocument23 pagesThe Role of Performance Measurement in Continuous Improvement - BondalbchilePas encore d'évaluation

- Three Decades of Continuous Improvement - SanchezDocument17 pagesThree Decades of Continuous Improvement - SanchezalbchilePas encore d'évaluation

- Continuous Improvement Beyond The Lean Understanding - HoltskogDocument5 pagesContinuous Improvement Beyond The Lean Understanding - HoltskogalbchilePas encore d'évaluation

- Using Mixed Methods Designs - HarrisonDocument10 pagesUsing Mixed Methods Designs - HarrisonalbchilePas encore d'évaluation

- Balanced Scorecard For Quality Excellence in The Construction IndustryDocument44 pagesBalanced Scorecard For Quality Excellence in The Construction Industrym.w lawrancePas encore d'évaluation

- Kaplan 2005 Strategy BSC and McKinseyDocument6 pagesKaplan 2005 Strategy BSC and McKinseyAgustinus Agung WirawanPas encore d'évaluation

- BSC2200 Balanced Scorecard in Public SectorDocument12 pagesBSC2200 Balanced Scorecard in Public Sectorapi-3825626100% (1)

- IPMS For McDonald IndonesiaDocument10 pagesIPMS For McDonald Indonesiadedysuryawan89Pas encore d'évaluation

- Balanced Scorecard ExampleDocument6 pagesBalanced Scorecard ExampleMark Geneve75% (4)

- Management Control Systems As A PackageDocument15 pagesManagement Control Systems As A PackageErnaFitrianaPas encore d'évaluation

- Employee Engagement That WorksDocument7 pagesEmployee Engagement That WorksAntoni Gosalvez MorgadesPas encore d'évaluation

- Stevenson 14e Chap002Document41 pagesStevenson 14e Chap002CheskaPas encore d'évaluation

- Quality-Access To SuccessDocument131 pagesQuality-Access To SuccessAdelaPas encore d'évaluation

- IT Service DeliveryDocument19 pagesIT Service DeliveryBambang Puji Haryo WicaksonoPas encore d'évaluation

- PNP Patrol Plan 2030-GuidebookDocument31 pagesPNP Patrol Plan 2030-GuidebookFadz Juhasan100% (1)

- EVA and BSCDocument24 pagesEVA and BSCroue2000Pas encore d'évaluation

- Balanced Scorecard For UPVTC by VillegasDocument14 pagesBalanced Scorecard For UPVTC by VillegasEmaylyn AdapPas encore d'évaluation

- Accounting Dept's Standard Costing PresentationDocument46 pagesAccounting Dept's Standard Costing PresentationAbu Noman AsifPas encore d'évaluation

- BSC-An Implementation RoadmapDocument16 pagesBSC-An Implementation RoadmapseescriPas encore d'évaluation

- Balanced Scorecard-Enabled Project ManagementDocument40 pagesBalanced Scorecard-Enabled Project ManagementEdson Andres Valencia SuazaPas encore d'évaluation

- Performance ManagementDocument7 pagesPerformance ManagementJasper KroegerPas encore d'évaluation

- The Balanced Scorecard and Intangible AssetsDocument10 pagesThe Balanced Scorecard and Intangible Assetsxoltar1854Pas encore d'évaluation

- Balanced Scorecard Implementation in A Local Government Authority: Issues and ChallengesDocument35 pagesBalanced Scorecard Implementation in A Local Government Authority: Issues and ChallengessukeksiPas encore d'évaluation

- Voluntary Corporate Disclosures: The Trend TowardDocument9 pagesVoluntary Corporate Disclosures: The Trend TowardfayfivePas encore d'évaluation

- Putting Balance Scorecard To WorkDocument12 pagesPutting Balance Scorecard To WorkShivangi BansalPas encore d'évaluation

- MC DonaldDocument15 pagesMC DonaldShreya PatelPas encore d'évaluation

- Case Study 3 - Turkish Apparel IndustryDocument11 pagesCase Study 3 - Turkish Apparel IndustryShagun SinhaPas encore d'évaluation

- Balance Score CardDocument61 pagesBalance Score CardmadhurbvmPas encore d'évaluation

- HRM 602 - Final Master SyllabusDocument16 pagesHRM 602 - Final Master SyllabusAshley JacksonPas encore d'évaluation

- BSC Operations: Operations Management: An IntroductionDocument33 pagesBSC Operations: Operations Management: An IntroductionMuhammad Sajid SaeedPas encore d'évaluation

- Performance AppraisalDocument30 pagesPerformance AppraisalSwyam DuggalPas encore d'évaluation

- Examples of Organizational Performance Management SystemsDocument6 pagesExamples of Organizational Performance Management SystemsAnswaf AnsuPas encore d'évaluation

- Chapter 18 Foundation of ControlDocument25 pagesChapter 18 Foundation of Controlhalka2314Pas encore d'évaluation

- CH 11 Strategy Monitoring Kel 7Document3 pagesCH 11 Strategy Monitoring Kel 7IBGA AGASTYAPas encore d'évaluation