Vous aimerez peut-être aussi

- A Study On Ratio Analysis in Tata MotorsDocument63 pagesA Study On Ratio Analysis in Tata MotorsMeena Sivasubramanian100% (3)

- Profitabilty of Tata Motors by Vivek PatelDocument28 pagesProfitabilty of Tata Motors by Vivek Patelram801Pas encore d'évaluation

- Financial Statement and Ratio Analysis of Tata MotorsDocument75 pagesFinancial Statement and Ratio Analysis of Tata MotorsAMIT K SINGH0% (1)

- A Ratio Analysis Report On FINAL of TataDocument38 pagesA Ratio Analysis Report On FINAL of TataPoonam GuptaPas encore d'évaluation

- Automobile Industry Ratio AnalysisDocument71 pagesAutomobile Industry Ratio Analysisakshay50% (2)

- Bfsi Report of VipulDocument5 pagesBfsi Report of VipulVipul100% (1)

- Financial Analysis Automobile IndustryDocument38 pagesFinancial Analysis Automobile Industryali iqbalPas encore d'évaluation

- Fundamental Analysis of FMCG Sector Ashish Chanchlani PDFDocument61 pagesFundamental Analysis of FMCG Sector Ashish Chanchlani PDFSAKSHI KHAITAN0% (1)

- SUMMER TRAINING REPORT - CameyDocument99 pagesSUMMER TRAINING REPORT - CameycameyPas encore d'évaluation

- Mahindra and MahindraDocument60 pagesMahindra and MahindraAparna TumbarePas encore d'évaluation

- Case Study For 2nd Year Students PDFDocument3 pagesCase Study For 2nd Year Students PDFArjun JosPas encore d'évaluation

- Fundamental Analysis of IT SectorDocument12 pagesFundamental Analysis of IT SectorManasi Kalgutkar100% (2)

- Fundamental Analysis of IT SectorDocument28 pagesFundamental Analysis of IT SectorHasnain BaberPas encore d'évaluation

- Financial Performance Analysis of Force MotorsDocument89 pagesFinancial Performance Analysis of Force Motorsshaaiily100% (2)

- Tata Motors Nano To Roll OutDocument4 pagesTata Motors Nano To Roll OutSymon StefenPas encore d'évaluation

- SIP On CEAT LTD by DharmeshDocument75 pagesSIP On CEAT LTD by DharmeshDharmesh AhirPas encore d'évaluation

- Marketing Mix of Tata Motors - 4p of Tata MotorsDocument4 pagesMarketing Mix of Tata Motors - 4p of Tata Motorskvbtrb9898Pas encore d'évaluation

- Fundamental Analysis of FMCG Sector Ashish ChanchlaniDocument88 pagesFundamental Analysis of FMCG Sector Ashish ChanchlaniVarun P ViswanPas encore d'évaluation

- Project Report: Pune UniversityDocument58 pagesProject Report: Pune UniversityMayur N Malviya100% (1)

- An Analysis of Mutual Fund Performance of SBI & Investor'sDocument56 pagesAn Analysis of Mutual Fund Performance of SBI & Investor'sabhisinghaPas encore d'évaluation

- RATIO ANALYSIS Synopsis For IngnouDocument11 pagesRATIO ANALYSIS Synopsis For IngnouAnonymous 5quBUnmvm1Pas encore d'évaluation

- NSE ProjectDocument24 pagesNSE ProjectRonnie KapoorPas encore d'évaluation

- Abstracts - Financial Performance Analysis of Tata Motors.Document3 pagesAbstracts - Financial Performance Analysis of Tata Motors.N.MUTHUKUMARAN100% (2)

- Fundamental Analysis of Tata Motors 10 September 2008Document23 pagesFundamental Analysis of Tata Motors 10 September 2008raju100% (10)

- Financial Ratio Analysis of Tata Motors RrssDocument48 pagesFinancial Ratio Analysis of Tata Motors RrssYatik GoyalPas encore d'évaluation

- Financial Analysis HDFC BANK1Document66 pagesFinancial Analysis HDFC BANK1Parveen KumarPas encore d'évaluation

- Equity ResearchDocument84 pagesEquity Researchtulasinad123100% (1)

- Working Cap Project 2019Document29 pagesWorking Cap Project 2019KAJAL TIWARI50% (2)

- Performance Analysis of Tata Motors and Maruti SuzukiDocument13 pagesPerformance Analysis of Tata Motors and Maruti SuzukisherlyPas encore d'évaluation

- A Study On Financial Performance Analysis With Reference To TNSC Bank Chennai Ijariie10138Document7 pagesA Study On Financial Performance Analysis With Reference To TNSC Bank Chennai Ijariie10138Jeevitha MuruganPas encore d'évaluation

- Tata Motors Cost of CapitalDocument10 pagesTata Motors Cost of CapitalMia KhalifaPas encore d'évaluation

- Axis Bank Marketing StrategyDocument10 pagesAxis Bank Marketing StrategyVishal KamblePas encore d'évaluation

- Financial Analysis of Hero CyclesDocument106 pagesFinancial Analysis of Hero CyclesD Attitude Kid50% (12)

- Dabur Working Capital Management Dabur IndiaDocument55 pagesDabur Working Capital Management Dabur IndiaPankaj ThakurPas encore d'évaluation

- Project On Capital MarketDocument106 pagesProject On Capital Marketgsravan_23Pas encore d'évaluation

- Equity Research Summer ProjectDocument66 pagesEquity Research Summer Projectpajhaveri4009Pas encore d'évaluation

- Final Project Format For Profitability Ratio Analysis of Company A, Company B and Company C in Same Industry For FY 20X1 20X2 20X3Document15 pagesFinal Project Format For Profitability Ratio Analysis of Company A, Company B and Company C in Same Industry For FY 20X1 20X2 20X3janimeetmePas encore d'évaluation

- Tata Consultancy Services - Wikipedia, The Free EncyclopediaDocument13 pagesTata Consultancy Services - Wikipedia, The Free Encyclopediakrinunn100% (1)

- Comparative Ratio Analysis of Britannia and CadburyDocument21 pagesComparative Ratio Analysis of Britannia and CadburyPriyank Galaw57% (7)

- Equity Research On Cement SectorDocument85 pagesEquity Research On Cement Sectorpawansup100% (2)

- A Project Report On Technical Analysis at Share KhanDocument105 pagesA Project Report On Technical Analysis at Share KhanBabasab Patil (Karrisatte)100% (3)

- AtulDocument14 pagesAtulatul_rockstarPas encore d'évaluation

- Impacts of GST On Indian EconomyDocument14 pagesImpacts of GST On Indian EconomyR.Deepak KannaPas encore d'évaluation

- Project Report On Internship at Geojit BNP ParibasDocument7 pagesProject Report On Internship at Geojit BNP ParibasFebin Roy100% (1)

- Recent Trends in Banking & Financial Services'Document24 pagesRecent Trends in Banking & Financial Services'Anil BatraPas encore d'évaluation

- TATA MOTORS RATIO ANALYSIS (1) (4) Final Report LajdlfjhdgskDocument30 pagesTATA MOTORS RATIO ANALYSIS (1) (4) Final Report LajdlfjhdgskVishal SajgurePas encore d'évaluation

- Fundamental and Technical Analysis of Maruti SuzukiDocument24 pagesFundamental and Technical Analysis of Maruti Suzuki99793765930% (1)

- Epzs, Eous, Tps and SezsDocument23 pagesEpzs, Eous, Tps and Sezssachin patel100% (1)

- Ratio Analysis - Tata and M Amp MDocument38 pagesRatio Analysis - Tata and M Amp MNani BhupalamPas encore d'évaluation

- Financial PerformanceDocument71 pagesFinancial PerformanceTshering Choden Lachungpa50% (2)

- Financial Analysis Training ReportDocument71 pagesFinancial Analysis Training ReportSaurav PariyarPas encore d'évaluation

- Equity Research Report - Maruti SuzukiDocument13 pagesEquity Research Report - Maruti SuzukiShubhan Khan100% (1)

- Anand S Project On Customer SatisfactionDocument68 pagesAnand S Project On Customer SatisfactionSreejith NairPas encore d'évaluation

- Tata Motors Company ProfileDocument20 pagesTata Motors Company ProfileShashi KumarPas encore d'évaluation

- Overview of Indian Automobile IndustryDocument9 pagesOverview of Indian Automobile IndustrygokulPas encore d'évaluation

- TATA Motors - MBA Summer Training Project Report - Consumer Perception and Analysis of Future..Document54 pagesTATA Motors - MBA Summer Training Project Report - Consumer Perception and Analysis of Future..jeetu bhaiPas encore d'évaluation

- Project of TATA MOTORSDocument86 pagesProject of TATA MOTORSbijal1399100% (2)

- Summer Traning Project Report ON: Tata MotorsDocument56 pagesSummer Traning Project Report ON: Tata MotorsAbhishek KumarPas encore d'évaluation

- Research ReportDocument86 pagesResearch ReportavnishPas encore d'évaluation

- The Tata NanoDocument21 pagesThe Tata NanoSanjeev ThakurPas encore d'évaluation

- Cbactg01 Complete ModuleDocument170 pagesCbactg01 Complete ModuleJ LagardePas encore d'évaluation

- Chapter 30 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Document25 pagesChapter 30 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Falah Ud Din SheryarPas encore d'évaluation

- CAP III - Suggested Answer Papers - All Subjects - June 2019 PDFDocument133 pagesCAP III - Suggested Answer Papers - All Subjects - June 2019 PDFsantosh thapa chhetriPas encore d'évaluation

- Mock Exam FinalDocument23 pagesMock Exam FinalKamaruslan MustaphaPas encore d'évaluation

- Pre-Quali Examination - Level III - Cluster C, PDF FSUU AccountingDocument13 pagesPre-Quali Examination - Level III - Cluster C, PDF FSUU AccountingRobert CastilloPas encore d'évaluation

- Analysis of Financial StatementDocument51 pagesAnalysis of Financial StatementSumit Rp100% (4)

- Chapter 8 of Cfas by ValixDocument7 pagesChapter 8 of Cfas by ValixLukaPas encore d'évaluation

- Afar 2019Document9 pagesAfar 2019TakuriPas encore d'évaluation

- Key Chapter 11Document3 pagesKey Chapter 11JinAe NaPas encore d'évaluation

- Wiley Chapter 1. Financial Accounting. IFRS EditionDocument67 pagesWiley Chapter 1. Financial Accounting. IFRS Editionshuguftarashid100% (2)

- Final 17ncDocument10 pagesFinal 17ncKevin James Sedurifa OledanPas encore d'évaluation

- National University of Science and TechnologyDocument8 pagesNational University of Science and TechnologyPATIENCE MUSHONGAPas encore d'évaluation

- Cash Flow ProblemsDocument6 pagesCash Flow Problemsvkbm42Pas encore d'évaluation

- ACC 226 Week 4 To 5 SIMDocument33 pagesACC 226 Week 4 To 5 SIMMireya YuePas encore d'évaluation

- Tutorial Corporate Financial ReportingDocument3 pagesTutorial Corporate Financial ReportingrcaesarPas encore d'évaluation

- Instant Download Ebook PDF Financial Accounting 10th Edition by Jerry J Weygandt PDF ScribdDocument41 pagesInstant Download Ebook PDF Financial Accounting 10th Edition by Jerry J Weygandt PDF Scribdmarian.hillis984100% (46)

- QuizDocument5 pagesQuizmiss independent100% (1)

- Advanced Financial Accounting: 2 Year ExaminationDocument32 pagesAdvanced Financial Accounting: 2 Year ExaminationRobertKimtaiPas encore d'évaluation

- Quijonez Fashionables Comprehensive Prob Merchandising Solution - XLSX Direct Extension MethodDocument4 pagesQuijonez Fashionables Comprehensive Prob Merchandising Solution - XLSX Direct Extension MethodzairahPas encore d'évaluation

- Baaccen Shinang-1Document6 pagesBaaccen Shinang-1Prince PierrePas encore d'évaluation

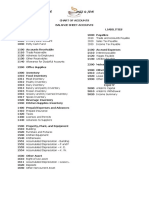

- REAL Chart of AccountsDocument4 pagesREAL Chart of Accountsllerry racuya100% (1)

- Financial Manamegent Prelim ModuleDocument52 pagesFinancial Manamegent Prelim ModuleExequiel Adrada100% (1)

- Excel Dashboard Templates 06Document10 pagesExcel Dashboard Templates 06Akhil RajPas encore d'évaluation

- Case: Ravi Bose, An NSU Business Graduate With Few Years' Experience As An Equities Analyst, Was Recently Brought in As Assistant To TheDocument13 pagesCase: Ravi Bose, An NSU Business Graduate With Few Years' Experience As An Equities Analyst, Was Recently Brought in As Assistant To TheAtik MahbubPas encore d'évaluation

- Chapter 5 - Financial StatementDocument31 pagesChapter 5 - Financial StatementQUYÊN VŨ THỊ THUPas encore d'évaluation

- Assignment POSTING TO THE LEDGERDocument7 pagesAssignment POSTING TO THE LEDGERJie SapornaPas encore d'évaluation

- Comprehensive ProblemDocument15 pagesComprehensive ProblemJacob SheridanPas encore d'évaluation

- Similarities and Differences Between IFRS and US GAApDocument12 pagesSimilarities and Differences Between IFRS and US GAApAlamin Mohammad100% (1)

- TB Chapter03 Analysis of Financial StatementsDocument68 pagesTB Chapter03 Analysis of Financial StatementsReymark BaldoPas encore d'évaluation

- Example Income Statement:: Gross SalesDocument2 pagesExample Income Statement:: Gross Salesabdirahman YonisPas encore d'évaluation

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaD'EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (14)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successD'EverandReady, Set, Growth hack:: A beginners guide to growth hacking successÉvaluation : 4.5 sur 5 étoiles4.5/5 (93)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingD'EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingÉvaluation : 4.5 sur 5 étoiles4.5/5 (17)

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthD'EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthÉvaluation : 4 sur 5 étoiles4/5 (20)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSND'Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNÉvaluation : 4.5 sur 5 étoiles4.5/5 (3)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaD'EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaÉvaluation : 3.5 sur 5 étoiles3.5/5 (8)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursD'EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursÉvaluation : 4.5 sur 5 étoiles4.5/5 (8)

- Creating Shareholder Value: A Guide For Managers And InvestorsD'EverandCreating Shareholder Value: A Guide For Managers And InvestorsÉvaluation : 4.5 sur 5 étoiles4.5/5 (8)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisD'EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisÉvaluation : 5 sur 5 étoiles5/5 (6)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialD'EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialÉvaluation : 4.5 sur 5 étoiles4.5/5 (32)

- Mind over Money: The Psychology of Money and How to Use It BetterD'EverandMind over Money: The Psychology of Money and How to Use It BetterÉvaluation : 4 sur 5 étoiles4/5 (24)

- Finance Basics (HBR 20-Minute Manager Series)D'EverandFinance Basics (HBR 20-Minute Manager Series)Évaluation : 4.5 sur 5 étoiles4.5/5 (32)

- Value: The Four Cornerstones of Corporate FinanceD'EverandValue: The Four Cornerstones of Corporate FinanceÉvaluation : 4.5 sur 5 étoiles4.5/5 (18)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamD'EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamPas encore d'évaluation

- Financial Risk Management: A Simple IntroductionD'EverandFinancial Risk Management: A Simple IntroductionÉvaluation : 4.5 sur 5 étoiles4.5/5 (7)

- Built, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursD'EverandBuilt, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursÉvaluation : 5 sur 5 étoiles5/5 (13)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistD'EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistÉvaluation : 4.5 sur 5 étoiles4.5/5 (73)

- Private Equity and Venture Capital in Europe: Markets, Techniques, and DealsD'EverandPrivate Equity and Venture Capital in Europe: Markets, Techniques, and DealsÉvaluation : 5 sur 5 étoiles5/5 (1)

- The Value of a Whale: On the Illusions of Green CapitalismD'EverandThe Value of a Whale: On the Illusions of Green CapitalismÉvaluation : 5 sur 5 étoiles5/5 (2)

- Product-Led Growth: How to Build a Product That Sells ItselfD'EverandProduct-Led Growth: How to Build a Product That Sells ItselfÉvaluation : 5 sur 5 étoiles5/5 (1)

- Applied Corporate Finance. What is a Company worth?D'EverandApplied Corporate Finance. What is a Company worth?Évaluation : 3 sur 5 étoiles3/5 (2)

- The Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsD'EverandThe Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsPas encore d'évaluation

- Finance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)D'EverandFinance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)Évaluation : 4 sur 5 étoiles4/5 (5)