Vous aimerez peut-être aussi

- Wall Street Playboys-Triangle Investing-Stocks, Real Estate and Crypto CurrenciesDocument139 pagesWall Street Playboys-Triangle Investing-Stocks, Real Estate and Crypto Currenciesboo100% (5)

- AICPA Released Questions FAR 2015 DifficultDocument33 pagesAICPA Released Questions FAR 2015 DifficultAZNGUY100% (2)

- What Is GAAPDocument13 pagesWhat Is GAAPmshashi5Pas encore d'évaluation

- Australian TaxationDocument45 pagesAustralian TaxationEhtesham HaquePas encore d'évaluation

- Business Federal Tax UpdateDocument9 pagesBusiness Federal Tax Updatesean dale porlaresPas encore d'évaluation

- Case Presentation - Woodland Furniture LTDDocument16 pagesCase Presentation - Woodland Furniture LTDLucksonPas encore d'évaluation

- Lecture 5 - A Note On Valuation in Private EquityDocument85 pagesLecture 5 - A Note On Valuation in Private EquitySinan DenizPas encore d'évaluation

- IA Terminal Output 1Document8 pagesIA Terminal Output 1Jannefah Irish Saglayan100% (1)

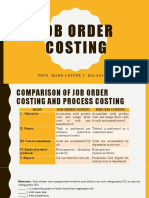

- Job Order Costing: Prof. Mark Lester T. Balasa, CpaDocument24 pagesJob Order Costing: Prof. Mark Lester T. Balasa, CpaNah HamzaPas encore d'évaluation

- Republic Act No. 7279Document25 pagesRepublic Act No. 7279Sharmen Dizon GalleneroPas encore d'évaluation

- Chapter 8 - Short Term FinancingDocument45 pagesChapter 8 - Short Term FinancingCindy Jane Omillio100% (1)

- Kon Kia Hai Dogars Edition PDFDocument296 pagesKon Kia Hai Dogars Edition PDFNoman AzizPas encore d'évaluation

- ADocument67 pagesApiyushsithaPas encore d'évaluation

- Zamora v. CollectorDocument2 pagesZamora v. CollectorPax YabutPas encore d'évaluation

- Acc 100 Quiz AnswersDocument9 pagesAcc 100 Quiz Answersscribdpdfs100% (1)

- Rural Marketing Mix Strategies PDFDocument103 pagesRural Marketing Mix Strategies PDFRangasai TadakamallaPas encore d'évaluation

- Assignment of Income DoctrineDocument20 pagesAssignment of Income DoctrinewxwgmumpdPas encore d'évaluation

- ACCY963 Week2 Lecture Slides GeneralDocument74 pagesACCY963 Week2 Lecture Slides GeneralNIRAJ SharmaPas encore d'évaluation

- Financial AccountingDocument47 pagesFinancial Accountinghuu nguyenPas encore d'évaluation

- ACC101 Chapter9newDocument19 pagesACC101 Chapter9newXiao HoPas encore d'évaluation

- TIF Problems 07-10 (2014)Document141 pagesTIF Problems 07-10 (2014)Mariella NiyoyunguruzaPas encore d'évaluation

- Case Study TaxDocument5 pagesCase Study TaxAnonymous wfLsDXifPas encore d'évaluation

- Exam Prep Taxation COMLAW301Document7 pagesExam Prep Taxation COMLAW301sdea032Pas encore d'évaluation

- FA-FFA September 2018 To August 2019Document7 pagesFA-FFA September 2018 To August 2019leylaPas encore d'évaluation

- Chapter-3Document20 pagesChapter-3rajes wariPas encore d'évaluation

- Acc 702 Assignment 4Document8 pagesAcc 702 Assignment 4laukkeasPas encore d'évaluation

- Accounting Principles and StandardsDocument6 pagesAccounting Principles and StandardswondmagegnPas encore d'évaluation

- Topic 2 Thomas Chapter 27Document16 pagesTopic 2 Thomas Chapter 27skye SPas encore d'évaluation

- Accounting 202 Notes - David HornungDocument28 pagesAccounting 202 Notes - David HornungAvi Goodstein100% (1)

- Assignment On Company Law & Secretary Pactices Group 7Document75 pagesAssignment On Company Law & Secretary Pactices Group 7MdramjanaliPas encore d'évaluation

- Questions Chapter 2Document4 pagesQuestions Chapter 2Minh Thư Phạm HuỳnhPas encore d'évaluation

- Year-End Tax Reminders 2012: Action Area Action StatusDocument2 pagesYear-End Tax Reminders 2012: Action Area Action Statusapi-129279783Pas encore d'évaluation

- MB0041 Financial and Management AccountingDocument8 pagesMB0041 Financial and Management Accountingarunavo22100% (1)

- Partnership AccountsDocument26 pagesPartnership Accountsoneunique.1unqPas encore d'évaluation

- How Are Notes Payable Different From Accounts Payable?Document3 pagesHow Are Notes Payable Different From Accounts Payable?Ellaine Pearl AlmillaPas encore d'évaluation

- How Are Notes Payable Different From Accounts Payable?Document3 pagesHow Are Notes Payable Different From Accounts Payable?Ellaine Pearl AlmillaPas encore d'évaluation

- Af308 WK 07 Text 2020Document29 pagesAf308 WK 07 Text 2020Prisha NarayanPas encore d'évaluation

- Actg Coach Actg Princ1Document3 pagesActg Coach Actg Princ1Amir IrfanPas encore d'évaluation

- Byrd and Chens Canadian Tax Principles Canadian 1st Edition Byrd Test BankDocument36 pagesByrd and Chens Canadian Tax Principles Canadian 1st Edition Byrd Test Bankheadlandsquiteedqfqhi100% (13)

- Byrd and Chens Canadian Tax Principles 2018 2019 1st Edition Byrd Test BankDocument39 pagesByrd and Chens Canadian Tax Principles 2018 2019 1st Edition Byrd Test Bankhumidityhaygsim8p100% (16)

- Ebook Byrd and Chens Canadian Tax Principles 2018 2019 1St Edition Byrd Test Bank Full Chapter PDFDocument68 pagesEbook Byrd and Chens Canadian Tax Principles 2018 2019 1St Edition Byrd Test Bank Full Chapter PDFShannonRussellapcx100% (13)

- RECEIVABLESDocument4 pagesRECEIVABLESCyril DE LA VEGAPas encore d'évaluation

- Pre Tax For InvidualDocument11 pagesPre Tax For InvidualStephanie NGPas encore d'évaluation

- Accounts ReceivableDocument9 pagesAccounts ReceivableTrang LePas encore d'évaluation

- Incorporation For Physicians in British Columbia CanadaDocument9 pagesIncorporation For Physicians in British Columbia CanadachadPas encore d'évaluation

- Quiz 1 2500 2017 FallDocument10 pagesQuiz 1 2500 2017 Fallbraveali999Pas encore d'évaluation

- Tax File Memorandum and Research EssayDocument7 pagesTax File Memorandum and Research EssayAssignmentLab.com0% (1)

- Accounting and ReportingDocument12 pagesAccounting and ReportingDheeraj JainPas encore d'évaluation

- Introduction To Financial Accounting ProjectDocument12 pagesIntroduction To Financial Accounting ProjectYannick HarveyPas encore d'évaluation

- Flash: Bad Debt and Limited Recourse Debt AmendmentsDocument3 pagesFlash: Bad Debt and Limited Recourse Debt Amendmentssajjadcheema3Pas encore d'évaluation

- Cruz2007 Chapter3 SM FinalDocument20 pagesCruz2007 Chapter3 SM Finalasd50% (4)

- Acctg11e SM CH11Document52 pagesAcctg11e SM CH11titirPas encore d'évaluation

- CH 8Document36 pagesCH 8anjo hosmerPas encore d'évaluation

- Treasurer's Report March 2013Document2 pagesTreasurer's Report March 2013redoak8hoaPas encore d'évaluation

- The Accounting Treatment of DividendsDocument5 pagesThe Accounting Treatment of DividendsVictor SantiagoPas encore d'évaluation

- Discounting and Unwinding: Answer 2-No, Deferred Consideration Is Not A Contingent Consideration Because It Does NotDocument5 pagesDiscounting and Unwinding: Answer 2-No, Deferred Consideration Is Not A Contingent Consideration Because It Does NotM Azeem IqbalPas encore d'évaluation

- CSM - CHP 12 - Accounting For Income TaxDocument4 pagesCSM - CHP 12 - Accounting For Income TaxaseppahrudinPas encore d'évaluation

- Financial Accounting (Najeeb)Document8 pagesFinancial Accounting (Najeeb)Najeeb Khan0% (1)

- Wassim Zhani Federal Taxation For Individuals (Chapter 5)Document40 pagesWassim Zhani Federal Taxation For Individuals (Chapter 5)wassim zhaniPas encore d'évaluation

- Tutorial 2 SolutionsDocument4 pagesTutorial 2 SolutionsnaboumilikaPas encore d'évaluation

- CH 13 - Current LiabilitiesDocument85 pagesCH 13 - Current LiabilitiesViviane Tavares60% (5)

- ACC300 Final Exam Score 90%Document9 pagesACC300 Final Exam Score 90%G JhaPas encore d'évaluation

- Chapter 10Document33 pagesChapter 10Usman ShabbirPas encore d'évaluation

- Ch11 WRD25e InstructorDocument72 pagesCh11 WRD25e InstructorFiskal Reguler 15Pas encore d'évaluation

- Interest Is Associated With What? Notes Receivable and Notes Payable Aging For The AllowanceDocument10 pagesInterest Is Associated With What? Notes Receivable and Notes Payable Aging For The Allowanceppate110Pas encore d'évaluation

- 1 Altprob 6eDocument3 pages1 Altprob 6eJane ChungPas encore d'évaluation

- Corporate Finance - Lecture 7Document9 pagesCorporate Finance - Lecture 7Sadia AbidPas encore d'évaluation

- CH 07Document99 pagesCH 07homeboimartinPas encore d'évaluation

- Identifying InformationDocument1 pageIdentifying InformationSambuttPas encore d'évaluation

- New Doc 2020-01-15 08.06.54Document2 pagesNew Doc 2020-01-15 08.06.54SambuttPas encore d'évaluation

- 11 Islamiat Pre Board PaperDocument2 pages11 Islamiat Pre Board PaperSambuttPas encore d'évaluation

- 11th Biology Pre Board Paper-2Document4 pages11th Biology Pre Board Paper-2SambuttPas encore d'évaluation

- Unique College For GirlsDocument2 pagesUnique College For GirlsSambuttPas encore d'évaluation

- A Closer Look at InstinctsDocument1 pageA Closer Look at InstinctsSambuttPas encore d'évaluation

- 8Document1 page8SambuttPas encore d'évaluation

- Password of Zip FileDocument1 pagePassword of Zip FileSambuttPas encore d'évaluation

- A Brief History of The Instinct Theory of MotivationDocument1 pageA Brief History of The Instinct Theory of MotivationSambuttPas encore d'évaluation

- Observations About Instinct TheoryDocument1 pageObservations About Instinct TheorySambuttPas encore d'évaluation

- Of The Members Referred To in Paragrap3Document1 pageOf The Members Referred To in Paragrap3SambuttPas encore d'évaluation

- SummaryDocument1 pageSummarySambuttPas encore d'évaluation

- In HumansDocument1 pageIn HumansSambuttPas encore d'évaluation

- Lot As To Which Two Members Shall Retire After The First Three YearsDocument1 pageLot As To Which Two Members Shall Retire After The First Three YearsSambuttPas encore d'évaluation

- (Please Tick Appropriate Box) Yes No: Comments and Future Action DiscussedDocument1 page(Please Tick Appropriate Box) Yes No: Comments and Future Action DiscussedSambuttPas encore d'évaluation

- Instinct Theory of MotivationDocument1 pageInstinct Theory of MotivationSambuttPas encore d'évaluation

- Substitution of Article 58 of The ConstitutionDocument1 pageSubstitution of Article 58 of The ConstitutionSambuttPas encore d'évaluation

- The Senate Shall Consist of OneDocument1 pageThe Senate Shall Consist of OneSambuttPas encore d'évaluation

- The Senate Shall Not Be Subject To Dissolution But The Term of Its MembersDocument1 pageThe Senate Shall Not Be Subject To Dissolution But The Term of Its MembersSambuttPas encore d'évaluation

- Of The Members Referred To in ParagraphDocument1 pageOf The Members Referred To in ParagraphSambuttPas encore d'évaluation

- Of The Members Referred To in Paragrap3Document1 pageOf The Members Referred To in Paragrap3SambuttPas encore d'évaluation

- Of The Members Referred To in Paragrap3Document1 pageOf The Members Referred To in Paragrap3SambuttPas encore d'évaluation

- Detail of Further Evidence RequiredDocument1 pageDetail of Further Evidence RequiredSambuttPas encore d'évaluation

- Commencement of The Constitution (Eighteenth Amendment) Act, 2010Document1 pageCommencement of The Constitution (Eighteenth Amendment) Act, 2010SambuttPas encore d'évaluation

- Of The Members Referred To in Paragrap2Document1 pageOf The Members Referred To in Paragrap2SambuttPas encore d'évaluation

- Of The Members Referred To in Paragrap3Document1 pageOf The Members Referred To in Paragrap3SambuttPas encore d'évaluation

- (E) Four Technocrats Including Ulema Shall Be Elected by The Members of Each Provincial Assembly andDocument1 page(E) Four Technocrats Including Ulema Shall Be Elected by The Members of Each Provincial Assembly andSambuttPas encore d'évaluation

- Of The Members Referred To in Paragrap1Document1 pageOf The Members Referred To in Paragrap1SambuttPas encore d'évaluation

- Election To Fill Seats in The Senate Allocated To Each Province Shall Be Held in Accordance With The System of Proportional Representation by Means of The Single Transferable VoteDocument1 pageElection To Fill Seats in The Senate Allocated To Each Province Shall Be Held in Accordance With The System of Proportional Representation by Means of The Single Transferable VoteSambuttPas encore d'évaluation

- Government Forms TypesDocument13 pagesGovernment Forms Typesavinash reddyPas encore d'évaluation

- 55 - Chapter 6 Exercises With AnswersDocument4 pages55 - Chapter 6 Exercises With Answersgio gioPas encore d'évaluation

- Sainsbury Financial AnalysisDocument21 pagesSainsbury Financial AnalysisSig SGPas encore d'évaluation

- Back Testing With 99 Percent Modelling V1Document4 pagesBack Testing With 99 Percent Modelling V1drakko_mxPas encore d'évaluation

- Googles Success Ben Morrow Thesis 2008 PDFDocument31 pagesGoogles Success Ben Morrow Thesis 2008 PDFAzim MohammedPas encore d'évaluation

- TEGI0600Document54 pagesTEGI0600Ely TharPas encore d'évaluation

- Investment in Equity SecuritiesDocument19 pagesInvestment in Equity SecuritiesNicholai NonanPas encore d'évaluation

- Cash Flow Statement: by Prof. Anita B. CatolicoDocument12 pagesCash Flow Statement: by Prof. Anita B. CatolicoAngelynDagsaanPas encore d'évaluation

- EOS Accounts and Budget Services Level IVDocument90 pagesEOS Accounts and Budget Services Level IVGAGE COLLEGE REGISTRAR100% (14)

- Factors Influencing Transfer Pricing Compliance An Indonesian Perspective PDFDocument301 pagesFactors Influencing Transfer Pricing Compliance An Indonesian Perspective PDFAlfharis AriyantoPas encore d'évaluation

- Ellerby ResumeDocument3 pagesEllerby ResumeRobEllerbyPas encore d'évaluation

- HTH587 Chapter 1 Intro To FinanceDocument9 pagesHTH587 Chapter 1 Intro To Financesvt joshPas encore d'évaluation

- NCND ImfpaDocument10 pagesNCND Imfpadoug dam100% (1)

- Form No.15gDocument2 pagesForm No.15gPrakash GowdaPas encore d'évaluation

- Safari - Aug 9, 2019 at 7:11 AM PDFDocument1 pageSafari - Aug 9, 2019 at 7:11 AM PDFMikaela SamontePas encore d'évaluation

- Chapter 2 ANALYZING TRANSACTIONS - Rev - CS - 2014Document96 pagesChapter 2 ANALYZING TRANSACTIONS - Rev - CS - 2014Nabila Nur IzzaPas encore d'évaluation

- Account Number Account Name Header Balance 10000 ASSET 11000 Current AssetDocument4 pagesAccount Number Account Name Header Balance 10000 ASSET 11000 Current AssetMuhammad Aziz FikriPas encore d'évaluation

- 00 Tapovan Advanced Accounting Free Fasttrack Batch BenchmarkDocument144 pages00 Tapovan Advanced Accounting Free Fasttrack Batch BenchmarkDhiraj JaiswalPas encore d'évaluation

- Fundamentals of Corporate Finance, 2nd Edition, Selt Test Ch03Document7 pagesFundamentals of Corporate Finance, 2nd Edition, Selt Test Ch03macseuPas encore d'évaluation

- Project On Chocolate Industry in Lotte India Corporation Ltd1Document51 pagesProject On Chocolate Industry in Lotte India Corporation Ltd1Keleti Santhosh100% (1)

- Edelweiss Maiden Opportunities Fund Presentation Jan 2018Document23 pagesEdelweiss Maiden Opportunities Fund Presentation Jan 2018shailabhPas encore d'évaluation

- Intermediate+Financial+Accounting+I+-+Chapter+3+ SDocument26 pagesIntermediate+Financial+Accounting+I+-+Chapter+3+ SNeil StechschultePas encore d'évaluation