Vous aimerez peut-être aussi

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- How Venture Capitalists Evaluate Potential Venture OpportunitiesDocument46 pagesHow Venture Capitalists Evaluate Potential Venture OpportunitiesBiman Bikash KalitaPas encore d'évaluation

- Cost Sheet FormatDocument5 pagesCost Sheet FormatJatin Gadhiya83% (6)

- Capital GainDocument22 pagesCapital GainVikas SinghPas encore d'évaluation

- Hedge Fund Primer Vanguard)Document24 pagesHedge Fund Primer Vanguard)Lee BellPas encore d'évaluation

- Assignment SAPMDocument5 pagesAssignment SAPMAanchal NarulaPas encore d'évaluation

- Humber Course 4 Commercial Study Notes v11Document517 pagesHumber Course 4 Commercial Study Notes v11Karan SarvaiyaPas encore d'évaluation

- 5 2 52 235 PDFDocument6 pages5 2 52 235 PDFChander GcPas encore d'évaluation

- Syllabus Store KeeperDocument4 pagesSyllabus Store KeeperAlok KumarPas encore d'évaluation

- Journal of Accounting - Auditing & Finance-2012-Agarwal-359-85Document28 pagesJournal of Accounting - Auditing & Finance-2012-Agarwal-359-85Atif KhanPas encore d'évaluation

- Introduction To Derivatives and Risk Management 10th Edition Chance Test BankDocument8 pagesIntroduction To Derivatives and Risk Management 10th Edition Chance Test BankMavos OdinPas encore d'évaluation

- Introduction To Business ValuationDocument9 pagesIntroduction To Business Valuationscholta00Pas encore d'évaluation

- Nism Equity Derivatives Study NotesDocument27 pagesNism Equity Derivatives Study NotesHemant bhanawatPas encore d'évaluation

- Mini Case Chapter 5 The Venezuelan Bolivar Black MarketDocument1 pageMini Case Chapter 5 The Venezuelan Bolivar Black MarketNiyant SapaPas encore d'évaluation

- E ServicesDocument11 pagesE ServicesSohaib NaeemPas encore d'évaluation

- PROJECT REPORT of Marketing Strategies of Ashlar Group Bhupendra Dixit Anand Engg. CollegeDocument64 pagesPROJECT REPORT of Marketing Strategies of Ashlar Group Bhupendra Dixit Anand Engg. CollegeAyush TiwariPas encore d'évaluation

- Demystifying Derivatives: Online Training Program OnDocument5 pagesDemystifying Derivatives: Online Training Program OnA K GuptaPas encore d'évaluation

- Pertemuan 13 - Investasi Saham (Kurang Dari 20%) PDFDocument14 pagesPertemuan 13 - Investasi Saham (Kurang Dari 20%) PDFayu utamiPas encore d'évaluation

- FM Assignment AnanduDocument23 pagesFM Assignment AnanduAmrutha P RPas encore d'évaluation

- "Study of Venture Capital in India": Annamalai UniversityDocument153 pages"Study of Venture Capital in India": Annamalai UniversityPraveen JoePas encore d'évaluation

- Consolidated Financial Statements-Date of AcquisitionDocument57 pagesConsolidated Financial Statements-Date of AcquisitionDirga DarmawanPas encore d'évaluation

- CBSE Class 12 April12 Business Studies Syllabus 2023 24Document23 pagesCBSE Class 12 April12 Business Studies Syllabus 2023 24Home Grown CreationPas encore d'évaluation

- GSIS SIF Notes - To - FS 2006Document24 pagesGSIS SIF Notes - To - FS 2006marielPas encore d'évaluation

- Heuristic Biases in Investment Decision-Making and Perceived Market EfficiencyDocument26 pagesHeuristic Biases in Investment Decision-Making and Perceived Market EfficiencyDaniel Pandapotan MarpaungPas encore d'évaluation

- Why Study Financial Markets and Institutions?: All Rights ReservedDocument23 pagesWhy Study Financial Markets and Institutions?: All Rights ReservedДарьяPas encore d'évaluation

- Understanding Order Types and Trading Instructions in Stock TradingDocument2 pagesUnderstanding Order Types and Trading Instructions in Stock TradingBecca SPas encore d'évaluation

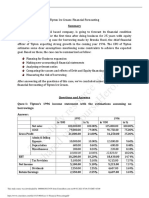

- Case 11 Financial ForecastingDocument9 pagesCase 11 Financial ForecastingFD ReynosoPas encore d'évaluation

- Preservation of RecordsDocument5 pagesPreservation of RecordsKaran GulatiPas encore d'évaluation

- Ch.1 Profit or Loss Pre and Post Incorporation - OrganizedDocument14 pagesCh.1 Profit or Loss Pre and Post Incorporation - OrganizedMonikaPas encore d'évaluation

- Forward ContractsDocument6 pagesForward ContractsAlpa JoshiPas encore d'évaluation

- Financial Statement FraudDocument19 pagesFinancial Statement FraudAulia HidayatPas encore d'évaluation