Vous aimerez peut-être aussi

- TIN Card As ID For Notarization PurposesDocument9 pagesTIN Card As ID For Notarization PurposesBobby Olavides SebastianPas encore d'évaluation

- E-Filing RuleDocument6 pagesE-Filing RuleThe Supreme Court Public Information Office100% (1)

- Deal Memo Terms of AgreementDocument4 pagesDeal Memo Terms of AgreementnagaviharPas encore d'évaluation

- 153 - Chamber of Real Estate and Builders Association V Romulo (2010)Document3 pages153 - Chamber of Real Estate and Builders Association V Romulo (2010)Charvan CharengPas encore d'évaluation

- BIR Form 1600Document39 pagesBIR Form 1600maeshach60% (5)

- J.K. Lasser's Your Income Tax 2019: For Preparing Your 2018 Tax ReturnD'EverandJ.K. Lasser's Your Income Tax 2019: For Preparing Your 2018 Tax ReturnPas encore d'évaluation

- Building Code Requirements and Permit FeesDocument6 pagesBuilding Code Requirements and Permit FeesBobby Olavides SebastianPas encore d'évaluation

- Transfer and Business Taxation - MIDTERMDocument14 pagesTransfer and Business Taxation - MIDTERMYvette Pauline JovenPas encore d'évaluation

- RR 2-98Document21 pagesRR 2-98Joshua HornePas encore d'évaluation

- 07 Other Business TaxesDocument31 pages07 Other Business TaxesGolden ChildPas encore d'évaluation

- WITHHOLDING TAX OBLIGATIONSDocument152 pagesWITHHOLDING TAX OBLIGATIONSemytherese100% (2)

- Simple Loan Agreement Template 3Document6 pagesSimple Loan Agreement Template 3Rem SerranoPas encore d'évaluation

- Business Taxation and VAT GuideDocument50 pagesBusiness Taxation and VAT GuideAllyson VillalobosPas encore d'évaluation

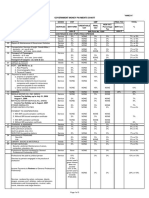

- Government Money Payments Chart - BirDocument3 pagesGovernment Money Payments Chart - BirVan Caz89% (9)

- Other Percentage TaxesDocument40 pagesOther Percentage TaxesKay Hanalee Villanueva NorioPas encore d'évaluation

- SEC Amends FRB No. 6 on Deposits for Future Stock SubscriptionDocument5 pagesSEC Amends FRB No. 6 on Deposits for Future Stock SubscriptionAbraham GuiyabPas encore d'évaluation

- 1040 Exam Prep Module XI: Circular 230 and AMTD'Everand1040 Exam Prep Module XI: Circular 230 and AMTÉvaluation : 1 sur 5 étoiles1/5 (1)

- Regulatory Framework For The Accreditation of Gaming SystemDocument8 pagesRegulatory Framework For The Accreditation of Gaming SystemBobby Olavides SebastianPas encore d'évaluation

- Philippines vs Soriano Land Expropriation Capital Gains TaxDocument2 pagesPhilippines vs Soriano Land Expropriation Capital Gains TaxNivra Lyn EmpialesPas encore d'évaluation

- 1040 Exam Prep Module X: Small Business Income and ExpensesD'Everand1040 Exam Prep Module X: Small Business Income and ExpensesPas encore d'évaluation

- 1600 Tax RatesDocument2 pages1600 Tax RatesmelizzePas encore d'évaluation

- Airport Construction Influencing FactorsDocument4 pagesAirport Construction Influencing FactorsIbrahim AdelPas encore d'évaluation

- 1601E - August 2008Document3 pages1601E - August 2008lovesresearchPas encore d'évaluation

- 1601E BIR FormDocument7 pages1601E BIR FormAdonis Zoleta AranilloPas encore d'évaluation

- Managing Airport Construction ProjectsDocument10 pagesManaging Airport Construction ProjectsTATATAHER100% (1)

- Bank of America v. CA G.R. No. 103092Document6 pagesBank of America v. CA G.R. No. 103092Jopan SJPas encore d'évaluation

- MBTC v. CIRDocument3 pagesMBTC v. CIRAngelique Padilla UgayPas encore d'évaluation

- Monthly Remittance Return of Creditable Income Taxes Withheld (Expanded) : BIR Form No. 1601-E/2307Document5 pagesMonthly Remittance Return of Creditable Income Taxes Withheld (Expanded) : BIR Form No. 1601-E/2307i1958239Pas encore d'évaluation

- EWTDocument12 pagesEWTdawngarcia1797Pas encore d'évaluation

- Tax Rates For CWT (Expanded) PDFDocument2 pagesTax Rates For CWT (Expanded) PDFRoseAnnFloriaPas encore d'évaluation

- Withholding Tax at Source OR Expanded Withholding Tax (EWT)Document32 pagesWithholding Tax at Source OR Expanded Withholding Tax (EWT)rickmortyPas encore d'évaluation

- 2307Document5 pages2307jblopez66Pas encore d'évaluation

- 2307Document3 pages2307Anonymous yCFuth7BL80% (1)

- EPayments Import TemplateDocument10 pagesEPayments Import TemplateGhulam MustafaPas encore d'évaluation

- Certificate of Creditable Tax Withheld at Source: Kawanihan NG Rentas InternasDocument3 pagesCertificate of Creditable Tax Withheld at Source: Kawanihan NG Rentas InternasAurora Pelagio VallejosPas encore d'évaluation

- FinalDocument2 pagesFinalJessica FordPas encore d'évaluation

- Creditable Tax ReportDocument131 pagesCreditable Tax ReportJieve Licca G. FanoPas encore d'évaluation

- Percentage Tax GuideDocument6 pagesPercentage Tax GuideChristine BobisPas encore d'évaluation

- New Payment Sections TemplateDocument1 pageNew Payment Sections Templateiaeste20078797Pas encore d'évaluation

- O o o O: Percentage Tax DescriptionDocument3 pagesO o o O: Percentage Tax Descriptionscartoneros_1Pas encore d'évaluation

- BIR Form 2307 Tax CodesDocument16 pagesBIR Form 2307 Tax CodesAnalyn Velasco Matibag100% (1)

- 2307 PDFDocument2 pages2307 PDFAnonymous BVowhxQPPas encore d'évaluation

- WT Tax RatesDocument2 pagesWT Tax RatesericbacsalPas encore d'évaluation

- Basic Accounting From ICPA AnswersDocument23 pagesBasic Accounting From ICPA AnswersPines MacapagalPas encore d'évaluation

- 2307Document16 pages2307Mika AkimPas encore d'évaluation

- VATable TransactionsDocument2 pagesVATable TransactionsAngelo D. AventuradoPas encore d'évaluation

- RR No. 11-2018Document90 pagesRR No. 11-2018Leticia TaclasPas encore d'évaluation

- 1601e Form PDFDocument3 pages1601e Form PDFLee GhaiaPas encore d'évaluation

- TAXATION LAW HIGHLIGHTSDocument4 pagesTAXATION LAW HIGHLIGHTSJM BermudoPas encore d'évaluation

- RR No. 6-2001 (Digest) PDFDocument1 pageRR No. 6-2001 (Digest) PDFFrancis GuinooPas encore d'évaluation

- Types of Taxes in The PhilippinesDocument4 pagesTypes of Taxes in The PhilippinesJustin Laraño RabagoPas encore d'évaluation

- BIR Form 2307Document20 pagesBIR Form 2307Lean Isidro0% (1)

- Income TaxationDocument32 pagesIncome TaxationkarlPas encore d'évaluation

- 1601EDocument7 pages1601EEnrique Membrere SupsupPas encore d'évaluation

- Summary of Final Tax Under The Nirc, As Amended Individual Citizen AlienDocument16 pagesSummary of Final Tax Under The Nirc, As Amended Individual Citizen AlienXiaoyu KensamePas encore d'évaluation

- Chapter 2.1 - Income Subject To Final TaxDocument30 pagesChapter 2.1 - Income Subject To Final Taxjudel ArielPas encore d'évaluation

- 1601E - August 2008Document4 pages1601E - August 2008HarryPas encore d'évaluation

- Taxation Report Vina MarieDocument12 pagesTaxation Report Vina MarieAnonymous gmDxRbnwOPas encore d'évaluation

- 06 Value Added TaxDocument43 pages06 Value Added TaxGolden ChildPas encore d'évaluation

- Certificate of Creditable Tax Withheld at Source: Kawanihan NG Rentas InternasDocument2 pagesCertificate of Creditable Tax Withheld at Source: Kawanihan NG Rentas InternasgioPas encore d'évaluation

- Tax obligations of resident Filipino citizensDocument2 pagesTax obligations of resident Filipino citizensAJ Quim100% (1)

- Withholding Tax RatesDocument35 pagesWithholding Tax RatesZonia Mae CuidnoPas encore d'évaluation

- Value Added TaxDocument8 pagesValue Added TaxDaniel MweuPas encore d'évaluation

- Epayments Import TemplateDocument6 pagesEpayments Import TemplateMohammad MohsinPas encore d'évaluation

- E. Other Percentage TaxesDocument49 pagesE. Other Percentage TaxesNatalie SerranoPas encore d'évaluation

- Preferential TaxationDocument2 pagesPreferential TaxationPrankyJellyPas encore d'évaluation

- 2010 Tax Matrix - Special RatesDocument2 pages2010 Tax Matrix - Special Ratescmv mendozaPas encore d'évaluation

- TemplateDocument15 pagesTemplateJared BemilPas encore d'évaluation

- Amendments to Revenue Regulations No. 2-98Document55 pagesAmendments to Revenue Regulations No. 2-98Cuayo JuicoPas encore d'évaluation

- OptDocument19 pagesOptDanica SarmientoPas encore d'évaluation

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesD'EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesPas encore d'évaluation

- JK Lasser's Small Business Taxes 2010: Your Complete Guide to a Better Bottom LineD'EverandJK Lasser's Small Business Taxes 2010: Your Complete Guide to a Better Bottom LinePas encore d'évaluation

- BSP Warning Advisory On Virtual CurrenciesDocument2 pagesBSP Warning Advisory On Virtual CurrenciesBobby Olavides SebastianPas encore d'évaluation

- Film Financing and Television Programming - PhilippinesDocument20 pagesFilm Financing and Television Programming - PhilippinesBobby Olavides SebastianPas encore d'évaluation

- SEC MSRD Request For Comments On The Updated Proposed Rules On Initial Coin OfferingDocument46 pagesSEC MSRD Request For Comments On The Updated Proposed Rules On Initial Coin OfferingBobby Olavides SebastianPas encore d'évaluation

- SEC Advisory PHILIPPINE GLOBAL COINDocument2 pagesSEC Advisory PHILIPPINE GLOBAL COINBobby Olavides SebastianPas encore d'évaluation

- SEC Advisory Re MiningDocument3 pagesSEC Advisory Re MiningBobby Olavides SebastianPas encore d'évaluation

- SEC Advisory Secret2SuccessDocument3 pagesSEC Advisory Secret2SuccessBobby Olavides SebastianPas encore d'évaluation

- SEC Advisory PhilcrowdDocument2 pagesSEC Advisory PhilcrowdBobby Olavides SebastianPas encore d'évaluation

- BSP Circular No. 944-2017 (Guidelines For Virtual Currency (VC) Exchanges)Document6 pagesBSP Circular No. 944-2017 (Guidelines For Virtual Currency (VC) Exchanges)Bobby Olavides SebastianPas encore d'évaluation

- SEC Advisory PluggleDocument3 pagesSEC Advisory PluggleBobby Olavides SebastianPas encore d'évaluation

- SEC Advisory Public Participation in Initial Coin OfferingDocument2 pagesSEC Advisory Public Participation in Initial Coin OfferingBobby Olavides SebastianPas encore d'évaluation

- SEC Advisory OnecashDocument2 pagesSEC Advisory OnecashBobby Olavides SebastianPas encore d'évaluation

- TESDA - Program Registration Forms Land-BasedDocument26 pagesTESDA - Program Registration Forms Land-BasedBobby Olavides SebastianPas encore d'évaluation

- 2021NOTICE Extension of Enrollment in OSTDocument1 page2021NOTICE Extension of Enrollment in OSTBobby Olavides SebastianPas encore d'évaluation

- Supreme Court: Administrative Circular No. 14 - 2021Document1 pageSupreme Court: Administrative Circular No. 14 - 2021Bobby Olavides SebastianPas encore d'évaluation

- Guidelines On VideoconferencingDocument23 pagesGuidelines On VideoconferencingBobby Olavides SebastianPas encore d'évaluation

- UTPRAS Guidelines (HTTP://WWW - Tesda.gov - ph/About/TESDA/42)Document5 pagesUTPRAS Guidelines (HTTP://WWW - Tesda.gov - ph/About/TESDA/42)Bobby Olavides SebastianPas encore d'évaluation

- Supreme Court: Administrative Circular No. 15 - 2021Document2 pagesSupreme Court: Administrative Circular No. 15 - 2021Eunice SagunPas encore d'évaluation

- Revised Construction Safety Guidelines During COVID-19Document12 pagesRevised Construction Safety Guidelines During COVID-19Bobby Olavides SebastianPas encore d'évaluation

- RMC 66-03 (Taxability of PAL)Document4 pagesRMC 66-03 (Taxability of PAL)Bobby Olavides SebastianPas encore d'évaluation

- 2019OpinionNo19 40Document3 pages2019OpinionNo19 40Bobby Olavides SebastianPas encore d'évaluation

- All POGOs SPs - Compliance With The 60-40 Foreign Equity RequirementDocument1 pageAll POGOs SPs - Compliance With The 60-40 Foreign Equity RequirementBobby Olavides SebastianPas encore d'évaluation

- SB 1564Document59 pagesSB 1564Bobby Olavides SebastianPas encore d'évaluation

- Cheaper Medicines Act of 2008Document28 pagesCheaper Medicines Act of 2008Bobby Olavides SebastianPas encore d'évaluation

- Overview of International Taxation & DTAA: Apt & Co LLPDocument49 pagesOverview of International Taxation & DTAA: Apt & Co LLPanon_127497276Pas encore d'évaluation

- PUBLIC FINANCE AND TAXATION- BCOM ACC, FIN & BBADocument13 pagesPUBLIC FINANCE AND TAXATION- BCOM ACC, FIN & BBAMaster KihimbwaPas encore d'évaluation

- Payroll Setup ChecklistDocument4 pagesPayroll Setup ChecklistcaliechPas encore d'évaluation

- 1704 BNSF Railway Automates Onboarding and Streamlines Processes With SAP ERecruiting and ERP Workflow PDFDocument43 pages1704 BNSF Railway Automates Onboarding and Streamlines Processes With SAP ERecruiting and ERP Workflow PDFKarthik BalasubramanianPas encore d'évaluation

- Understanding YOUR Bonus RecapDocument17 pagesUnderstanding YOUR Bonus RecapBjenaPas encore d'évaluation

- CIR Vs Procter & GambleDocument44 pagesCIR Vs Procter & GambleDario G. TorresPas encore d'évaluation

- ACCT604 Week 5 Lecture SlidesDocument27 pagesACCT604 Week 5 Lecture SlidesBuddika PrasannaPas encore d'évaluation

- BOKU Billing and Payments ProcessDocument11 pagesBOKU Billing and Payments ProcessAfc DeetweePas encore d'évaluation

- Please DocuSign Tax Certificate of Foreign S PDFDocument6 pagesPlease DocuSign Tax Certificate of Foreign S PDFRent rochorPas encore d'évaluation

- Scanner CAP II Income Tax VATDocument162 pagesScanner CAP II Income Tax VATEdtech NepalPas encore d'évaluation

- Tax 2 Notes FinalDocument91 pagesTax 2 Notes FinalRecson BangibangPas encore d'évaluation

- Tax RemediesDocument8 pagesTax RemediesKhim BebicPas encore d'évaluation

- Between:: Commented (C&G1) : We Note That TheDocument12 pagesBetween:: Commented (C&G1) : We Note That TheRafael JuicoPas encore d'évaluation

- BIR Form No. 0901-T (Transport and Shipping)Document2 pagesBIR Form No. 0901-T (Transport and Shipping)ChristianNicolasBetantosPas encore d'évaluation

- RPH NowDocument2 pagesRPH NowBilling ZamboecozonePas encore d'évaluation

- Tax DeadlinesDocument40 pagesTax DeadlinesSeasaltandsandPas encore d'évaluation

- Anscor Corp Tax CaseDocument8 pagesAnscor Corp Tax Casekimoymoy7Pas encore d'évaluation

- Unemployment Benefits: Who Is Entitled To Unemployment Benefit?Document8 pagesUnemployment Benefits: Who Is Entitled To Unemployment Benefit?DamjanPas encore d'évaluation

- VDS Guideline and VAT Rate For The FY 2020-2021 in Comparison With The FY 2019-2020Document9 pagesVDS Guideline and VAT Rate For The FY 2020-2021 in Comparison With The FY 2019-2020Masum GaziPas encore d'évaluation

- Appendix C - Bid Bond FormDocument2 pagesAppendix C - Bid Bond FormUmair Afrima100% (1)

- Service Guide DistributionsDocument49 pagesService Guide Distributions2361090Pas encore d'évaluation

- GNLD - International and Foster Sponsoring - NewDocument9 pagesGNLD - International and Foster Sponsoring - NewNishit KotakPas encore d'évaluation

- Filipinas Synthetic Fiber Corporation vs. CA, Cta, and CirDocument1 pageFilipinas Synthetic Fiber Corporation vs. CA, Cta, and CirmwaikePas encore d'évaluation

- Remittance Form for Final Income TaxesDocument1 pageRemittance Form for Final Income TaxesDhaine PedeRePas encore d'évaluation