Vous aimerez peut-être aussi

- Flash Memory IncDocument3 pagesFlash Memory IncAhsan IqbalPas encore d'évaluation

- Flash Memory IncDocument7 pagesFlash Memory IncAbhinandan SinghPas encore d'évaluation

- Flash Memory, Inc.Document2 pagesFlash Memory, Inc.Stella Zukhbaia0% (5)

- Flash Memory Case Study SolutionDocument8 pagesFlash Memory Case Study SolutionRohit Parnerkar57% (7)

- Flash - Memory - Inc From Website 0515Document8 pagesFlash - Memory - Inc From Website 0515竹本口木子100% (1)

- FlashMemory SolnDocument8 pagesFlashMemory Solnchopra98harsh3311100% (4)

- Flash Memory IncDocument9 pagesFlash Memory Incxcmalsk100% (1)

- FlashMemory Beta NPVDocument7 pagesFlashMemory Beta NPVShubham Bhatia100% (1)

- Flash MemoryDocument9 pagesFlash MemoryJeffery KaoPas encore d'évaluation

- Harvard Case Study - Flash Inc - AllDocument40 pagesHarvard Case Study - Flash Inc - All竹本口木子100% (1)

- Flash Memory CaseDocument6 pagesFlash Memory Casechitu199233% (3)

- Case - Flash Memory, Inc. - SolutionDocument11 pagesCase - Flash Memory, Inc. - SolutionBryan Meza71% (38)

- Flash Memory AnalysisDocument25 pagesFlash Memory AnalysisTheicon420Pas encore d'évaluation

- Flash Memory AnalysisDocument25 pagesFlash Memory AnalysisaamirPas encore d'évaluation

- Flash Memory Case SolutionDocument10 pagesFlash Memory Case SolutionsahilkuPas encore d'évaluation

- Flash Memory ExcelDocument4 pagesFlash Memory ExcelHarshita SethiyaPas encore d'évaluation

- Pacific Grove Spice CompanyDocument7 pagesPacific Grove Spice CompanySajjad Ahmad100% (1)

- Pacific Grove Spice CompanyDocument3 pagesPacific Grove Spice CompanyLaura JavelaPas encore d'évaluation

- New Heritage Doll CompanDocument9 pagesNew Heritage Doll CompanArima ChatterjeePas encore d'évaluation

- Mercuryathleticfootwera Case AnalysisDocument8 pagesMercuryathleticfootwera Case AnalysisNATOEEPas encore d'évaluation

- Hansson Private Label: Operating ResultsDocument28 pagesHansson Private Label: Operating ResultsShubham SharmaPas encore d'évaluation

- Flash Inc Financial StatementsDocument14 pagesFlash Inc Financial Statementsdummy306075% (4)

- Case Pacific Grove Spice CompanyDocument68 pagesCase Pacific Grove Spice CompanyJose Luis ContrerasPas encore d'évaluation

- New Heritage Doll Company Case SolutionDocument31 pagesNew Heritage Doll Company Case SolutionSoundarya AbiramiPas encore d'évaluation

- Heritage CaseDocument3 pagesHeritage CaseGregory ChengPas encore d'évaluation

- Toy World - ExhibitsDocument9 pagesToy World - Exhibitsakhilkrishnan007Pas encore d'évaluation

- HBS Mercury CaseDocument4 pagesHBS Mercury CaseDavid Petru100% (1)

- NHDC Solution EditedDocument5 pagesNHDC Solution EditedShreesh ChandraPas encore d'évaluation

- New Heritage ExhibitsDocument4 pagesNew Heritage ExhibitsBRobbins12100% (16)

- Question 1Document9 pagesQuestion 1Minh HàPas encore d'évaluation

- This Study Resource Was: Case Study - Flash Memory, IncDocument6 pagesThis Study Resource Was: Case Study - Flash Memory, IncWill TrầnPas encore d'évaluation

- Case - Polar SportsDocument12 pagesCase - Polar SportsSagar SrivastavaPas encore d'évaluation

- Polar SportDocument4 pagesPolar SportKinnary Kinnu0% (2)

- New Heritage Doll Company:: Capital BudgetingDocument27 pagesNew Heritage Doll Company:: Capital BudgetingInêsRosário100% (8)

- Tire City Spreadsheet SolutionDocument7 pagesTire City Spreadsheet SolutionSyed Ali MurtuzaPas encore d'évaluation

- Pacific Grove Spice Company SpreadsheetDocument7 pagesPacific Grove Spice Company SpreadsheetAnonymous 8ooQmMoNs10% (1)

- New Heritage Doll CoDocument3 pagesNew Heritage Doll Copalmis2100% (5)

- New Heritage DollDocument26 pagesNew Heritage DollJITESH GUPTAPas encore d'évaluation

- PGP Heritage Doll ExcelDocument5 pagesPGP Heritage Doll ExcelPGP37 392 Abhishek SinghPas encore d'évaluation

- HPL CaseDocument2 pagesHPL Caseprsnt100% (1)

- Gilbert Lumber LC ExcelDocument3 pagesGilbert Lumber LC ExcelEvelyn De de Leon100% (3)

- New Heritage Doll Company Capital Budgeting SolutionDocument10 pagesNew Heritage Doll Company Capital Budgeting SolutionBiswadeep royPas encore d'évaluation

- New Heritage Doll - SolutionDocument4 pagesNew Heritage Doll - Solutionrath347775% (4)

- Group6 - Heritage Doll CaseDocument6 pagesGroup6 - Heritage Doll Casesanket vermaPas encore d'évaluation

- (Shared) Day5 Harmonic Hearing Co. - 4271Document17 pages(Shared) Day5 Harmonic Hearing Co. - 4271DamTokyo0% (2)

- AirThread G015Document6 pagesAirThread G015sahildharhakim83% (6)

- New Heritage Doll Company Case SolutionDocument42 pagesNew Heritage Doll Company Case SolutionRupesh Sharma100% (6)

- Case AnalysisDocument11 pagesCase AnalysisSagar Bansal50% (2)

- AirThread Class 2020Document21 pagesAirThread Class 2020Son NguyenPas encore d'évaluation

- Hansson Private Label - FinalDocument34 pagesHansson Private Label - Finalincognito12312333% (3)

- 1) Assess The Current Financial Health and Recent Financial Performance of The Firm. Identify Any Strengths or WeaknessesDocument2 pages1) Assess The Current Financial Health and Recent Financial Performance of The Firm. Identify Any Strengths or WeaknessesJane SmithPas encore d'évaluation

- PESTEL Analysis of The Rise and Fall of BlackberryDocument4 pagesPESTEL Analysis of The Rise and Fall of BlackberryVino DhanapalPas encore d'évaluation

- IGNOU MBA MS - 04 Solved Assignment 2011Document16 pagesIGNOU MBA MS - 04 Solved Assignment 2011Kiran PattnaikPas encore d'évaluation

- ULTI Aug 16 Short ReportDocument16 pagesULTI Aug 16 Short ReportAnonymous Ecd8rCPas encore d'évaluation

- IGNOU MBA MS - 04 Solved Assignment 2011Document12 pagesIGNOU MBA MS - 04 Solved Assignment 2011Nazif LcPas encore d'évaluation

- Invests Belligerently in Research and Development of New Products To Stay Ahead of TheDocument1 pageInvests Belligerently in Research and Development of New Products To Stay Ahead of TheAyesha TahirPas encore d'évaluation

- Chapter 6 Prospective Analysis: ForecastingDocument10 pagesChapter 6 Prospective Analysis: ForecastingSheep ersPas encore d'évaluation

- Case Studies in Working Capital Management and ShortDocument13 pagesCase Studies in Working Capital Management and ShortNguyễn Thế LongPas encore d'évaluation

- Financing A New Venture Trough and Initial Public Offering (IPO)Document32 pagesFinancing A New Venture Trough and Initial Public Offering (IPO)Manthan LalanPas encore d'évaluation

- Eastboro Case Write Up For Presentation1Document4 pagesEastboro Case Write Up For Presentation1Paula Elaine ThorpePas encore d'évaluation

- Paper More-Excel SheetDocument133 pagesPaper More-Excel Sheetkiller dramaPas encore d'évaluation

- Combined SPSS in Excel 456Document89 pagesCombined SPSS in Excel 456killer dramaPas encore d'évaluation

- Looper Height TagsDocument1 pageLooper Height Tagskiller dramaPas encore d'évaluation

- PAnelDocument11 pagesPAnelkiller dramaPas encore d'évaluation

- Nedbank Case Study - FinalDocument2 pagesNedbank Case Study - Finalkiller dramaPas encore d'évaluation

- SDDocument1 pageSDkiller dramaPas encore d'évaluation

- Scale For EFA For Resilience ModelDocument9 pagesScale For EFA For Resilience Modelkiller dramaPas encore d'évaluation

- Oep SCMP A5 Minibrochure WebDocument8 pagesOep SCMP A5 Minibrochure Webkiller dramaPas encore d'évaluation

- 1.1. Brief of The CaseDocument6 pages1.1. Brief of The Casekiller dramaPas encore d'évaluation

- Boeing 777 ADocument3 pagesBoeing 777 Akiller dramaPas encore d'évaluation

- Ucalgary 2013 Kano LienaDocument349 pagesUcalgary 2013 Kano Lienakiller dramaPas encore d'évaluation

- What Is The Difference Between Tier 1 Capital and Tier 2 Capital - InvestopediaDocument6 pagesWhat Is The Difference Between Tier 1 Capital and Tier 2 Capital - Investopediakiller dramaPas encore d'évaluation

- Key Takeaways From E&Y WebinarDocument2 pagesKey Takeaways From E&Y Webinarkiller dramaPas encore d'évaluation

- Syntax GG PlotDocument3 pagesSyntax GG Plotkiller dramaPas encore d'évaluation

- Executive Summary:: Sl. No. Areas Implications Under GSTDocument2 pagesExecutive Summary:: Sl. No. Areas Implications Under GSTkiller dramaPas encore d'évaluation

- Specification For - OGPCS008 (Online Grading System)Document1 pageSpecification For - OGPCS008 (Online Grading System)killer dramaPas encore d'évaluation

- Research Papers Ref 30th JanDocument33 pagesResearch Papers Ref 30th Jankiller dramaPas encore d'évaluation

- Zonal Grievance Redressal Officers: Zone States Covered Name & Designation Email Id Tel No. With STD CodeDocument1 pageZonal Grievance Redressal Officers: Zone States Covered Name & Designation Email Id Tel No. With STD Codekiller dramaPas encore d'évaluation

- Manual For Building ANP Decision ModelsDocument84 pagesManual For Building ANP Decision Modelskiller dramaPas encore d'évaluation

- Doe PracticeDocument237 pagesDoe Practicekiller dramaPas encore d'évaluation

- Macro Note BookDocument56 pagesMacro Note Bookkiller dramaPas encore d'évaluation

- Case Study: Incomplete SolutionsDocument6 pagesCase Study: Incomplete Solutionskiller dramaPas encore d'évaluation

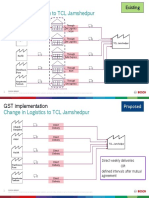

- Annexure 2 - Change in Logistics To TCL JamshedpurDocument2 pagesAnnexure 2 - Change in Logistics To TCL Jamshedpurkiller dramaPas encore d'évaluation

- Type I and Type II Errror in ACCDocument3 pagesType I and Type II Errror in ACCkiller dramaPas encore d'évaluation

- Reliance Trend Store ProjectDocument9 pagesReliance Trend Store Projectkiller dramaPas encore d'évaluation

- PH Case Mexico BOPDocument6 pagesPH Case Mexico BOPkiller dramaPas encore d'évaluation

- Sqms QueryDocument2 pagesSqms Querykiller dramaPas encore d'évaluation

- Mo Os Best Post GST PDFDocument60 pagesMo Os Best Post GST PDFkiller dramaPas encore d'évaluation

- Advertising & Sales Promotion: Salesforce & Channel Distribution AssignmentDocument6 pagesAdvertising & Sales Promotion: Salesforce & Channel Distribution Assignmentkiller dramaPas encore d'évaluation

- Sgco GST PPT 2017Document46 pagesSgco GST PPT 2017killer dramaPas encore d'évaluation

- Chief Operating Officer in NYC Resume William HoganDocument3 pagesChief Operating Officer in NYC Resume William HoganWilliamHoganPas encore d'évaluation

- Competitive Advantage of Reliance MoneyDocument75 pagesCompetitive Advantage of Reliance Moneymo_hit123Pas encore d'évaluation

- 3q21 Earnings ReleaseDocument5 pages3q21 Earnings ReleaseBruno EnriquePas encore d'évaluation

- Solution Chapter 18Document61 pagesSolution Chapter 18xxxxxxxxx100% (3)

- Fin3n Cap Budgeting Quiz 1Document1 pageFin3n Cap Budgeting Quiz 1Kirsten Marie EximPas encore d'évaluation

- MOCK TEST of INCOME TAX WITHOUT SOLUTIONDocument19 pagesMOCK TEST of INCOME TAX WITHOUT SOLUTIONRajender SinghPas encore d'évaluation

- Swaps: Options, Futures, and Other Derivatives, 9th Edition, 1Document34 pagesSwaps: Options, Futures, and Other Derivatives, 9th Edition, 1胡丹阳Pas encore d'évaluation

- Voluntary Dissolution of CorporationsDocument20 pagesVoluntary Dissolution of CorporationsJohn Mark ParacadPas encore d'évaluation

- Mastering Depreciation TestbankDocument18 pagesMastering Depreciation TestbankLade PalkanPas encore d'évaluation

- By Vladimir Basov: Gold Mining: The Worlds Cheapest Jurisdictions // Vladimir BasovDocument6 pagesBy Vladimir Basov: Gold Mining: The Worlds Cheapest Jurisdictions // Vladimir BasovCharles BukowskiPas encore d'évaluation

- Liquidity RatioDocument3 pagesLiquidity RatioJodette Karyl NuyadPas encore d'évaluation

- FIN254 Assignment# 1Document2 pagesFIN254 Assignment# 1Zahidul IslamPas encore d'évaluation

- Epc Vs BotDocument3 pagesEpc Vs BotPayal ChauhanPas encore d'évaluation

- Banque de FranceDocument10 pagesBanque de FranceBianca GabrielaPas encore d'évaluation

- Algonquin Power Acquisition Fact SheetDocument3 pagesAlgonquin Power Acquisition Fact SheetBernewsAdminPas encore d'évaluation

- Chapter-4 Organizational Structure of HDFC BankDocument17 pagesChapter-4 Organizational Structure of HDFC Bankshraddha100% (1)

- The Obstacles To Regulating The Hawala - A Cultural Norm or A TerrDocument57 pagesThe Obstacles To Regulating The Hawala - A Cultural Norm or A TerrBrendan LanzaPas encore d'évaluation

- (Question Papers) RBrtI Grade "B" Officers - Finance and Management Papers of Last 8 Exams (Phase 2) MrunalDocument10 pages(Question Papers) RBrtI Grade "B" Officers - Finance and Management Papers of Last 8 Exams (Phase 2) Mrunalguru1241987babuPas encore d'évaluation

- Hero Motocorp: (Herhon)Document9 pagesHero Motocorp: (Herhon)ayushPas encore d'évaluation

- P2Document20 pagesP2Jemson YandugPas encore d'évaluation

- A Comparative Analysis of ULIP of Bajaj Allianz Life Insurance Co. LTD With Mutual FundDocument18 pagesA Comparative Analysis of ULIP of Bajaj Allianz Life Insurance Co. LTD With Mutual Fundrevanth reddyPas encore d'évaluation

- SALN Annual DeclarationDocument4 pagesSALN Annual DeclarationronaldodigmaPas encore d'évaluation

- Business Planning Insurance 2020 Question Bank SampleDocument50 pagesBusiness Planning Insurance 2020 Question Bank SampleIsavic Alsina100% (1)

- Advacc Chap 1Document22 pagesAdvacc Chap 1Ferdinand FernandoPas encore d'évaluation

- Assignment Print View13.4Document3 pagesAssignment Print View13.4alexie aurelioPas encore d'évaluation

- IFRS at A Glance - BDODocument29 pagesIFRS at A Glance - BDONaim Aqram67% (3)

- WhiteMonk HEG Equity Research ReportDocument15 pagesWhiteMonk HEG Equity Research ReportGirish Ramachandra100% (1)

- Ez 14Document2 pagesEz 14yes yesnoPas encore d'évaluation

- Chapter: Bond FundamentalsDocument28 pagesChapter: Bond FundamentalsUtkarsh VardhanPas encore d'évaluation

- Gianrie Gwyneth Cabigon - Assign - BusCom ExercisesDocument10 pagesGianrie Gwyneth Cabigon - Assign - BusCom ExercisesRie CabigonPas encore d'évaluation