Vous aimerez peut-être aussi

- Flash Memory IncDocument3 pagesFlash Memory IncAhsan IqbalPas encore d'évaluation

- Flash Memory, IncDocument16 pagesFlash Memory, Inckiller drama67% (3)

- Flash Memory, Inc.Document2 pagesFlash Memory, Inc.Stella Zukhbaia0% (5)

- Flash Memory Case Study SolutionDocument8 pagesFlash Memory Case Study SolutionRohit Parnerkar57% (7)

- Flash - Memory - Inc From Website 0515Document8 pagesFlash - Memory - Inc From Website 0515竹本口木子100% (1)

- FlashMemory Beta NPVDocument7 pagesFlashMemory Beta NPVShubham Bhatia100% (1)

- 128,000 forecasted sales in 2012Document8 pages128,000 forecasted sales in 2012chopra98harsh3311100% (4)

- Income Statements and Balance Sheets for Flash Memory, Inc. (2007-2009Document25 pagesIncome Statements and Balance Sheets for Flash Memory, Inc. (2007-2009Theicon420Pas encore d'évaluation

- Flash Memory Income Statements 2007-2009Document10 pagesFlash Memory Income Statements 2007-2009sahilkuPas encore d'évaluation

- TN-1 TN-2 Financials Cost CapitalDocument9 pagesTN-1 TN-2 Financials Cost Capitalxcmalsk100% (1)

- Harvard Case Study - Flash Inc - AllDocument40 pagesHarvard Case Study - Flash Inc - All竹本口木子100% (1)

- Flash MemoryDocument9 pagesFlash MemoryJeffery KaoPas encore d'évaluation

- This Study Resource Was: Case Study - Flash Memory, IncDocument6 pagesThis Study Resource Was: Case Study - Flash Memory, IncWill TrầnPas encore d'évaluation

- Flash Memory CaseDocument6 pagesFlash Memory Casechitu199233% (3)

- Flash Memory AnalysisDocument25 pagesFlash Memory AnalysisaamirPas encore d'évaluation

- Case - Flash Memory, Inc. - SolutionDocument11 pagesCase - Flash Memory, Inc. - SolutionBryan Meza71% (38)

- Jackson Automotive Systems ExcelDocument5 pagesJackson Automotive Systems Excelonyechi2004Pas encore d'évaluation

- Pacific Grove Spice CompanyDocument3 pagesPacific Grove Spice CompanyLaura JavelaPas encore d'évaluation

- Flash Memory ExcelDocument4 pagesFlash Memory ExcelHarshita SethiyaPas encore d'évaluation

- Toy World - ExhibitsDocument9 pagesToy World - Exhibitsakhilkrishnan007Pas encore d'évaluation

- PGSC Debt obj. income statement ratios 2006-2010Document68 pagesPGSC Debt obj. income statement ratios 2006-2010Jose Luis ContrerasPas encore d'évaluation

- Pacific Group Spice Company Fin300 ReportDocument9 pagesPacific Group Spice Company Fin300 ReportMinh HàPas encore d'évaluation

- Burton Sensors SheetDocument128 pagesBurton Sensors Sheetchirag shah17% (6)

- Pacific Grove Spice Company SpreadsheetDocument7 pagesPacific Grove Spice Company SpreadsheetAnonymous 8ooQmMoNs10% (1)

- Friendly CS SolutionDocument8 pagesFriendly CS SolutionEfendiPas encore d'évaluation

- Case 34 - The Wm. Wrigley Jr. CompanyDocument72 pagesCase 34 - The Wm. Wrigley Jr. CompanyQUYNH100% (1)

- Mercuryathleticfootwera Case AnalysisDocument8 pagesMercuryathleticfootwera Case AnalysisNATOEEPas encore d'évaluation

- Compagnie Du FroidDocument18 pagesCompagnie Du FroidSuryakant Kaushik0% (3)

- Maximizing Shareholder Value Through Optimal Dividend and Buyback PolicyDocument2 pagesMaximizing Shareholder Value Through Optimal Dividend and Buyback PolicyRichBrook7Pas encore d'évaluation

- Polar SportDocument4 pagesPolar SportKinnary Kinnu0% (2)

- Hill Country Snack Foods CoDocument1 pageHill Country Snack Foods CoKriti AhujaPas encore d'évaluation

- Pacific Grove Spice CompanyDocument7 pagesPacific Grove Spice CompanySajjad Ahmad100% (1)

- NHDC Solution EditedDocument5 pagesNHDC Solution EditedShreesh ChandraPas encore d'évaluation

- Analyzing Mercury Athletic Footwear AcquisitionDocument5 pagesAnalyzing Mercury Athletic Footwear AcquisitionCuong NguyenPas encore d'évaluation

- Questions - Linear Technologies CaseDocument1 pageQuestions - Linear Technologies CaseNathan Toledano100% (1)

- Exhibit 1Document2 pagesExhibit 1Natasha PerryPas encore d'évaluation

- Friendly Cards CaseDocument3 pagesFriendly Cards CaseJeff Farley50% (2)

- Continental Carriers Debt vs EquityDocument10 pagesContinental Carriers Debt vs Equitynipun9143Pas encore d'évaluation

- Online AnswerDocument4 pagesOnline AnswerYiru Pan100% (2)

- Flash Inc Financial StatementsDocument14 pagesFlash Inc Financial Statementsdummy306075% (4)

- LinearDocument6 pagesLinearjackedup211Pas encore d'évaluation

- Blain Kitchenware Inc.: Capital StructureDocument7 pagesBlain Kitchenware Inc.: Capital StructureRoy Lambert100% (4)

- AirThread Valuation MethodsDocument21 pagesAirThread Valuation MethodsSon NguyenPas encore d'évaluation

- Case AnalysisDocument11 pagesCase AnalysisSagar Bansal50% (2)

- Flash Memory, Inc. - Group 8Document1 pageFlash Memory, Inc. - Group 8Bryan MezaPas encore d'évaluation

- New Heritage DollDocument26 pagesNew Heritage DollJITESH GUPTAPas encore d'évaluation

- Tire City Spreadsheet SolutionDocument7 pagesTire City Spreadsheet SolutionSyed Ali MurtuzaPas encore d'évaluation

- Toy World CaseDocument9 pagesToy World Casedwchief100% (1)

- Pacific Grove Spice CompanyDocument1 pagePacific Grove Spice CompanyLauren KlaassenPas encore d'évaluation

- Pacific Grove Spice's acquisition of High Country Seasonings and TV show sponsorshipDocument9 pagesPacific Grove Spice's acquisition of High Country Seasonings and TV show sponsorshipdiddiPas encore d'évaluation

- Financial Performance Analysis of Exide IndustriesDocument11 pagesFinancial Performance Analysis of Exide IndustriesAnupriya SenPas encore d'évaluation

- PESTEL Analysis of The Rise and Fall of BlackberryDocument4 pagesPESTEL Analysis of The Rise and Fall of BlackberryVino DhanapalPas encore d'évaluation

- BUS 1102 - Week 7 - Statement of The Cash FlowDocument6 pagesBUS 1102 - Week 7 - Statement of The Cash FlowEmad AldenPas encore d'évaluation

- 1 Main Capital Quarterly LetterDocument10 pages1 Main Capital Quarterly LetterYog MehtaPas encore d'évaluation

- Sony ProjectDocument12 pagesSony ProjectfkkfoxPas encore d'évaluation

- Adjusted SG&ADocument6 pagesAdjusted SG&AJOHN KAISERPas encore d'évaluation

- Industrial SicknessDocument19 pagesIndustrial SicknessAnkit SoniPas encore d'évaluation

- Biolase MD&A AnalysisDocument2 pagesBiolase MD&A Analysisps67% (3)

- Chartered Professional Accountants of Canada, Cpa Canada, Cpa. © 2015, Chartered Professional Accountants of Canada. All Rights ReservedDocument19 pagesChartered Professional Accountants of Canada, Cpa Canada, Cpa. © 2015, Chartered Professional Accountants of Canada. All Rights ReservedHassleBustPas encore d'évaluation

- GMACCase (Feb2007)Document5 pagesGMACCase (Feb2007)norcaldbnPas encore d'évaluation

- Use More SoapsDocument9 pagesUse More SoapsAbhinandan SinghPas encore d'évaluation

- 13 Earned Value ManagementDocument9 pages13 Earned Value ManagementAbhinandan Singh100% (1)

- Positioning Book ReviewDocument35 pagesPositioning Book ReviewSmat JacerPas encore d'évaluation

- Stratergic Management Case Study On StarbucksDocument30 pagesStratergic Management Case Study On StarbucksRahul Sttud50% (2)

- Merve BEKTAŞ Didem ŞAHİN Sara OsmanoğluDocument22 pagesMerve BEKTAŞ Didem ŞAHİN Sara OsmanoğluAbhinandan SinghPas encore d'évaluation

- G GeniusDocument26 pagesG GeniusAbhinandan SinghPas encore d'évaluation

- World CSR Congress: Integrating Sustainability Into A Global OrganizationDocument12 pagesWorld CSR Congress: Integrating Sustainability Into A Global OrganizationAbhinandan SinghPas encore d'évaluation

- Visualmerchandising 121126111353 Phpapp02Document145 pagesVisualmerchandising 121126111353 Phpapp02Abhinandan SinghPas encore d'évaluation

- Mortein Vaporizer Marketing StrategyDocument26 pagesMortein Vaporizer Marketing Strategymukesh chavanPas encore d'évaluation

- Category Management 2Document9 pagesCategory Management 2Abhinandan SinghPas encore d'évaluation

- Merchandise Presentation in Retail Store - Intro, Demo, Floor Layout and SignageDocument26 pagesMerchandise Presentation in Retail Store - Intro, Demo, Floor Layout and SignageAbhinandan SinghPas encore d'évaluation

- Starbucks Deliveringcustomerservice 160222181028Document11 pagesStarbucks Deliveringcustomerservice 160222181028Abhinandan SinghPas encore d'évaluation

- Product Palaning Refe1Document58 pagesProduct Palaning Refe1rafiq5002Pas encore d'évaluation

- The Wonder of Mumbai Dabbawallas Inspiration of ManagementDocument23 pagesThe Wonder of Mumbai Dabbawallas Inspiration of ManagementSeema Mehta SharmaPas encore d'évaluation

- Starbucks: Delivering Customer ServiceDocument23 pagesStarbucks: Delivering Customer ServiceVishakha Rl RanaPas encore d'évaluation

- Saatchi&SaatchiDocument5 pagesSaatchi&SaatchiAbhinandan SinghPas encore d'évaluation

- 5 Fastest Frontend Web Dev Frameworks - Fonbell SolutionDocument13 pages5 Fastest Frontend Web Dev Frameworks - Fonbell SolutionAbhinandan SinghPas encore d'évaluation

- Leading Supply Chain Without Suits and TiesDocument11 pagesLeading Supply Chain Without Suits and TiesAnoop AgrawalPas encore d'évaluation

- General Motors and Its SuppliersDocument8 pagesGeneral Motors and Its SuppliersAbhinandan SinghPas encore d'évaluation

- Batiste 2in1 Dry Shampoo & Conditioner: Refreshes Roots and Targets Dryness For Gorgeously Soft, Conditioned HairDocument11 pagesBatiste 2in1 Dry Shampoo & Conditioner: Refreshes Roots and Targets Dryness For Gorgeously Soft, Conditioned HairAbhinandan SinghPas encore d'évaluation

- FINAL - New Product Development and Feasibility PDFDocument7 pagesFINAL - New Product Development and Feasibility PDFRenz PamintuanPas encore d'évaluation

- Valuation of 5000 stock options using Black Scholes model over 5 yearsDocument4 pagesValuation of 5000 stock options using Black Scholes model over 5 yearsAbhinandan Singh0% (2)

- Six Sigma - IDocument133 pagesSix Sigma - INitin PatelPas encore d'évaluation

- Teuer Furniture (A)Document14 pagesTeuer Furniture (A)Abhinandan SinghPas encore d'évaluation

- Freelancing ListDocument29 pagesFreelancing ListAbhinandan SinghPas encore d'évaluation

- Job Satisfaction and Employee Engagement Case StudyDocument11 pagesJob Satisfaction and Employee Engagement Case StudyMuneeb Ur-Rehman0% (1)

- TR EB Data Breach ResponseDocument5 pagesTR EB Data Breach ResponseAbhinandan SinghPas encore d'évaluation

- Atlantic Computer - A Bundling of Pricing OptionsDocument15 pagesAtlantic Computer - A Bundling of Pricing OptionsAbhinandan SinghPas encore d'évaluation

- XLRI Strategic Management of Apple Inc. in 2015Document6 pagesXLRI Strategic Management of Apple Inc. in 2015Abhinandan SinghPas encore d'évaluation

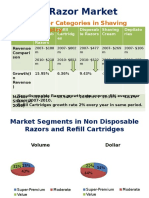

- US Razor Market ParamountDocument17 pagesUS Razor Market ParamountAbhinandan SinghPas encore d'évaluation

- KATU Investigates: Shelter Operation Costs in OregonDocument1 pageKATU Investigates: Shelter Operation Costs in OregoncgiardinelliPas encore d'évaluation

- Dean Divina J Del Castillo and OtherDocument113 pagesDean Divina J Del Castillo and OtheracolumnofsmokePas encore d'évaluation

- CH08 Location StrategyDocument45 pagesCH08 Location StrategyfatinS100% (5)

- OathDocument5 pagesOathRichard LazaroPas encore d'évaluation

- Virgin Atlantic Strategic Management (The Branson Effect and Employee Positioning)Document23 pagesVirgin Atlantic Strategic Management (The Branson Effect and Employee Positioning)Enoch ObatundePas encore d'évaluation

- Project Management in Practice 6th Edition Meredith Solutions ManualDocument25 pagesProject Management in Practice 6th Edition Meredith Solutions ManualMatthewFosteroeqyp98% (48)

- Lawyer Disciplinary CaseDocument8 pagesLawyer Disciplinary CaseRose De JesusPas encore d'évaluation

- VisitBit - Free Bitcoin! Instant Payments!Document14 pagesVisitBit - Free Bitcoin! Instant Payments!Saf Bes100% (3)

- Final Project Taxation Law IDocument28 pagesFinal Project Taxation Law IKhushil ShahPas encore d'évaluation

- The First, First ResponderDocument26 pagesThe First, First ResponderJose Enrique Patron GonzalezPas encore d'évaluation

- English Final Suggestion - HSC - 2013Document8 pagesEnglish Final Suggestion - HSC - 2013Jaman Palash (MSP)Pas encore d'évaluation

- Đa S A The PESTEL Analysis of VinamilkDocument2 pagesĐa S A The PESTEL Analysis of VinamilkHiền ThảoPas encore d'évaluation

- Symptomatic-Asymptomatic - MedlinePlus Medical EncyclopediaDocument4 pagesSymptomatic-Asymptomatic - MedlinePlus Medical EncyclopediaNISAR_786Pas encore d'évaluation

- Essential Rabbi Nachman meditation and personal prayerDocument9 pagesEssential Rabbi Nachman meditation and personal prayerrm_pi5282Pas encore d'évaluation

- Taiping's History as Malaysia's "City of Everlasting PeaceDocument6 pagesTaiping's History as Malaysia's "City of Everlasting PeaceIzeliwani Haji IsmailPas encore d'évaluation

- Poland Country VersionDocument44 pagesPoland Country VersionAlbert A. SusinskasPas encore d'évaluation

- Module 6 ObliCon Form Reformation and Interpretation of ContractsDocument6 pagesModule 6 ObliCon Form Reformation and Interpretation of ContractsAngelica BesinioPas encore d'évaluation

- Mission Youth PPT (Ramban) 06-11-2021Document46 pagesMission Youth PPT (Ramban) 06-11-2021BAWANI SINGHPas encore d'évaluation

- 0 - Dist Officers List 20.03.2021Document4 pages0 - Dist Officers List 20.03.2021srimanraju vbPas encore d'évaluation

- 1964 Letter From El-Hajj Malik El-ShabazzDocument2 pages1964 Letter From El-Hajj Malik El-Shabazzkyo_9Pas encore d'évaluation

- CHAPTER-1 FeasibilityDocument6 pagesCHAPTER-1 FeasibilityGlads De ChavezPas encore d'évaluation

- Dissertation 1984 OrwellDocument6 pagesDissertation 1984 OrwellCanSomeoneWriteMyPaperForMeMadison100% (1)

- American Bible Society Vs City of Manila 101 Phil 386Document13 pagesAmerican Bible Society Vs City of Manila 101 Phil 386Leomar Despi LadongaPas encore d'évaluation

- 1 Herzfeld, Michael - 2001 Sufferings and Disciplines - Parte A 1-7Document7 pages1 Herzfeld, Michael - 2001 Sufferings and Disciplines - Parte A 1-7Jhoan Almonte MateoPas encore d'évaluation

- What Does The Bible Say About Hell?Document12 pagesWhat Does The Bible Say About Hell?revjackhowell100% (2)

- Definition of Internal Order: Business of The Company (Orders With Revenues)Document6 pagesDefinition of Internal Order: Business of The Company (Orders With Revenues)MelaniePas encore d'évaluation

- 3-D Secure Vendor List v1 10-30-20181Document4 pages3-D Secure Vendor List v1 10-30-20181Mohamed LahlouPas encore d'évaluation

- Tax Invoice / Receipt: Total Paid: USD10.00 Date Paid: 12 May 2019Document3 pagesTax Invoice / Receipt: Total Paid: USD10.00 Date Paid: 12 May 2019coPas encore d'évaluation

- Adventures in Antarctica: 12 Days / 9 Nights On BoardDocument2 pagesAdventures in Antarctica: 12 Days / 9 Nights On BoardVALENCIA TORENTHAPas encore d'évaluation

- Pakistan Money MarketDocument2 pagesPakistan Money MarketOvais AdenwallaPas encore d'évaluation