Vous aimerez peut-être aussi

- Modern Debt Management - The Most Effective Debt Management SolutionsD'EverandModern Debt Management - The Most Effective Debt Management SolutionsPas encore d'évaluation

- A Presentation ON Banking LoansDocument18 pagesA Presentation ON Banking LoansKaran Jain100% (1)

- Revolving Credit ManagementDocument2 pagesRevolving Credit ManagementmirehoPas encore d'évaluation

- Households - Chapter 17 - DraftDocument12 pagesHouseholds - Chapter 17 - DraftFazra FarookPas encore d'évaluation

- Predatory Lending PDFDocument2 pagesPredatory Lending PDFgordomanotasPas encore d'évaluation

- Banking Law NotesDocument5 pagesBanking Law NotesBilal Ahmed Bilal AhmedPas encore d'évaluation

- Capital MarketDocument19 pagesCapital MarketUrbano, Lourene Fe S. BSBA FM 2CPas encore d'évaluation

- What Is Revolving Credit?Document3 pagesWhat Is Revolving Credit?Niño Rey LopezPas encore d'évaluation

- 8 Banker Customer Relationship PDFDocument20 pages8 Banker Customer Relationship PDFkhuram MehmoodPas encore d'évaluation

- 8 Banker Customer RelationshipDocument20 pages8 Banker Customer RelationshipRajitha LakmalPas encore d'évaluation

- Unit 2Document15 pagesUnit 2nothinghereguyzPas encore d'évaluation

- What Is A Credit Line?: Compare and ContrastDocument5 pagesWhat Is A Credit Line?: Compare and Contrastvivekananda RoyPas encore d'évaluation

- Current Liabilities ManagementDocument7 pagesCurrent Liabilities ManagementJack Herer100% (1)

- Consumer FinanceDocument16 pagesConsumer Financenageshalways100% (1)

- CIBILDocument11 pagesCIBILViji RangaPas encore d'évaluation

- Unit 05 - Principles of Bank LendingDocument18 pagesUnit 05 - Principles of Bank LendingSayak GhoshPas encore d'évaluation

- CreditDocument62 pagesCreditapi-262728967Pas encore d'évaluation

- Banker Customer Relationship: Nature, Type - General and SpecialDocument59 pagesBanker Customer Relationship: Nature, Type - General and Specialrajin_rammsteinPas encore d'évaluation

- Money & Banking Mix TopicsDocument35 pagesMoney & Banking Mix TopicsAAMINA ZAFARPas encore d'évaluation

- Presentation of Money and Banking FinalDocument25 pagesPresentation of Money and Banking FinalGHANI BUTTPas encore d'évaluation

- Mortgage and Consumer FinancingDocument11 pagesMortgage and Consumer FinancingAsad AkhlaqPas encore d'évaluation

- Banker As LenderDocument19 pagesBanker As Lendervanishachhabra5008Pas encore d'évaluation

- CreditcreationDocument16 pagesCreditcreationShadab UsmaniPas encore d'évaluation

- What Is A Nonperforming Loan NPLDocument6 pagesWhat Is A Nonperforming Loan NPLJacksonPas encore d'évaluation

- TYPES OF CREDIT Week13Document61 pagesTYPES OF CREDIT Week13Richard Santiago JimenezPas encore d'évaluation

- Lines of Credit: Key TakeawaysDocument2 pagesLines of Credit: Key TakeawaysKurt Del RosarioPas encore d'évaluation

- ch-4 Public DebtDocument30 pagesch-4 Public DebtyebegashetPas encore d'évaluation

- Principles of LendingDocument32 pagesPrinciples of LendingsugirajamsrPas encore d'évaluation

- Week 6-7: Chapter 6: Personal/Consumer CreditDocument24 pagesWeek 6-7: Chapter 6: Personal/Consumer CreditGiselle Bronda CastañedaPas encore d'évaluation

- 3.2 HouseholdsDocument3 pages3.2 HouseholdsRatna PuspitasariPas encore d'évaluation

- Chapter 3 (Lending)Document13 pagesChapter 3 (Lending)Mohammad Minhaz Hossain RiyadPas encore d'évaluation

- Working Capital ManagementDocument30 pagesWorking Capital ManagementEvangelinePas encore d'évaluation

- Working Capital Finance: Vikesh KumarDocument29 pagesWorking Capital Finance: Vikesh KumarAnonymous V4oDAKH3QdPas encore d'évaluation

- Basic Principles of Sound LendingDocument20 pagesBasic Principles of Sound LendingEknath Birari90% (21)

- AFN 221 W05 Consumer Credit vF2021Document23 pagesAFN 221 W05 Consumer Credit vF2021Dina SboulPas encore d'évaluation

- John Young - Banking Background - Capital FocusDocument53 pagesJohn Young - Banking Background - Capital FocusAndrewPas encore d'évaluation

- By Zohaib Javed Satti MBA-6Document22 pagesBy Zohaib Javed Satti MBA-6Zohaib Javed SattiPas encore d'évaluation

- Topic1-Concept of LendingDocument16 pagesTopic1-Concept of LendingPrEm GaBriel50% (2)

- E-Notes HouseholdsDocument3 pagesE-Notes HouseholdsGodfreyFrankMwakalingaPas encore d'évaluation

- Working Capital Finance: Vikesh KumarDocument29 pagesWorking Capital Finance: Vikesh KumarPrateek MarathaPas encore d'évaluation

- File 319334Document23 pagesFile 319334louise carinoPas encore d'évaluation

- Chapter - 14: Loans and AdvancesDocument24 pagesChapter - 14: Loans and AdvancesDevid LuizPas encore d'évaluation

- Economic Aspect of Public DebtDocument22 pagesEconomic Aspect of Public DebtHazel Valdez CasaldonPas encore d'évaluation

- Can I Afford A LoanDocument7 pagesCan I Afford A LoanBorisPas encore d'évaluation

- Unit-6: Commercial & Industrial LendingDocument28 pagesUnit-6: Commercial & Industrial LendingRaaz Key Run ChhatkuliPas encore d'évaluation

- Credit SystemDocument57 pagesCredit SystemHakdog CheesePas encore d'évaluation

- CreditDocument57 pagesCreditArundhuti RoyPas encore d'évaluation

- The Consumption FunctionDocument21 pagesThe Consumption Functionsadhu124Pas encore d'évaluation

- Advantages and Disadvantages of Any Kind of CreditDocument4 pagesAdvantages and Disadvantages of Any Kind of CreditJane Carla BorromeoPas encore d'évaluation

- Ch2-Classes and Kinds of CreditDocument45 pagesCh2-Classes and Kinds of CreditWilsonPas encore d'évaluation

- T.Y.Bbi Personal LoanDocument49 pagesT.Y.Bbi Personal LoanCh TarunPas encore d'évaluation

- Bankers Code, Debt Millionaire, Wealthy CodeDocument91 pagesBankers Code, Debt Millionaire, Wealthy CodeJohn Turner100% (2)

- Banking in Financial System. ProjectDocument40 pagesBanking in Financial System. Projectvickyrawat1983Pas encore d'évaluation

- Equity Cure Provisions and RemediesDocument3 pagesEquity Cure Provisions and RemediesRalph MontejoPas encore d'évaluation

- Lall Interest Rate ProjectDocument19 pagesLall Interest Rate ProjectSourav SsinghPas encore d'évaluation

- Personal Loan ProjectDocument7 pagesPersonal Loan ProjectSudhakar GuntukaPas encore d'évaluation

- Credit Creation & Credit ControlsDocument31 pagesCredit Creation & Credit ControlsVishnu thankachan100% (2)

- Loan Discounts Finance 7Document41 pagesLoan Discounts Finance 7Elvie Anne Lucero ClaudPas encore d'évaluation

- Intermediate Finance: Session 7Document54 pagesIntermediate Finance: Session 7rizaunPas encore d'évaluation

- Econ Course 202 Academy SayDocument909 pagesEcon Course 202 Academy SayKoyakuPas encore d'évaluation

- Current Labor MarketDocument42 pagesCurrent Labor MarketKoyakuPas encore d'évaluation

- Investment and The Stock Market: Stock Capital Same Same StockDocument32 pagesInvestment and The Stock Market: Stock Capital Same Same StockKoyakuPas encore d'évaluation

- Example Example: (5.5) : Continuation of (5.4)Document22 pagesExample Example: (5.5) : Continuation of (5.4)KoyakuPas encore d'évaluation

- Wage Determination: Collective BargainingDocument46 pagesWage Determination: Collective BargainingKoyakuPas encore d'évaluation

- Shifts of The Curve: Price Level Money Supply ExogenousDocument28 pagesShifts of The Curve: Price Level Money Supply ExogenousKoyakuPas encore d'évaluation

- Determination of The Optimal Capital InvestmentDocument34 pagesDetermination of The Optimal Capital InvestmentKoyakuPas encore d'évaluation

- Bond Prices and Interest RatesDocument27 pagesBond Prices and Interest RatesKoyakuPas encore d'évaluation

- Learning ObjectivesDocument33 pagesLearning ObjectivesKoyakuPas encore d'évaluation

- Consumption: Disposable IncomeDocument49 pagesConsumption: Disposable IncomeKoyakuPas encore d'évaluation

- Money: Assets PaymentDocument25 pagesMoney: Assets PaymentKoyakuPas encore d'évaluation

- Monetary Policy and Open Market OperationsDocument37 pagesMonetary Policy and Open Market OperationsKoyakuPas encore d'évaluation

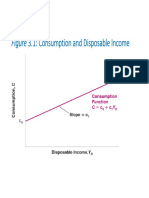

- Figure 3.1: Consumption and Disposable IncomeDocument33 pagesFigure 3.1: Consumption and Disposable IncomeKoyakuPas encore d'évaluation

- The Determination of Equilibrium Output in A Graph: Building Output Fiscal Policy Income Production Equal IncomeDocument33 pagesThe Determination of Equilibrium Output in A Graph: Building Output Fiscal Policy Income Production Equal IncomeKoyakuPas encore d'évaluation

- Money Demand Function: Increase Increases Reduces Increase Increases Reduces One For OneDocument30 pagesMoney Demand Function: Increase Increases Reduces Increase Increases Reduces One For OneKoyakuPas encore d'évaluation

- Market For Goods in The Classical Model: Lower Discourages EncouragesDocument28 pagesMarket For Goods in The Classical Model: Lower Discourages EncouragesKoyakuPas encore d'évaluation

- The Government Sector: - Income Taxes and Automatic StabilizersDocument44 pagesThe Government Sector: - Income Taxes and Automatic StabilizersKoyakuPas encore d'évaluation

- Saving and Wealth Over The Life Cycle: Income High Low Short Long Together Constant ConstantDocument29 pagesSaving and Wealth Over The Life Cycle: Income High Low Short Long Together Constant ConstantKoyakuPas encore d'évaluation

- PT. Ispat Indo Company ProfileDocument2 pagesPT. Ispat Indo Company Profileputri rianiPas encore d'évaluation

- Assam: Udayon MisraDocument16 pagesAssam: Udayon MisraBhaavika ChawlaPas encore d'évaluation

- Clarisonic ITC ComplaintDocument85 pagesClarisonic ITC ComplaintSarah BursteinPas encore d'évaluation

- Assignment 3 Financial Markets Tu Huu Phuc s3812120 1Document10 pagesAssignment 3 Financial Markets Tu Huu Phuc s3812120 1Nguyễn TùngPas encore d'évaluation

- Support and Resistance BasicsDocument17 pagesSupport and Resistance BasicsMong is not herePas encore d'évaluation

- CF 1e PPT Slides Chap04.1 Edited VersionDocument34 pagesCF 1e PPT Slides Chap04.1 Edited VersionMuhamad DzulhazreenPas encore d'évaluation

- IFM 02 Exchange Rate SystemsDocument53 pagesIFM 02 Exchange Rate SystemsTanu GuptaPas encore d'évaluation

- Microeconomics Endterm Q1Document2 pagesMicroeconomics Endterm Q1Sports at it's bestPas encore d'évaluation

- OEM - Fuel Manager Brand Cross Reference P/Ns For Service Filter Elements 99642 - August 2006Document6 pagesOEM - Fuel Manager Brand Cross Reference P/Ns For Service Filter Elements 99642 - August 2006Cleber SilvaPas encore d'évaluation

- Equity CrowdfundingDocument13 pagesEquity CrowdfundingantonyPas encore d'évaluation

- TCS Salary SlipDocument1 pageTCS Salary Slipkrishna100% (1)

- Wage Account November 2020M HN-1Document12 pagesWage Account November 2020M HN-1Pavel ViktorPas encore d'évaluation

- PhilEquity Fund ProspectusDocument42 pagesPhilEquity Fund ProspectuskimencinaPas encore d'évaluation

- Corporate Governance - Christine Mallin - Role of Institutional Investors in Corporate GovernanceDocument3 pagesCorporate Governance - Christine Mallin - Role of Institutional Investors in Corporate GovernanceUzzal Sarker - উজ্জ্বল সরকারPas encore d'évaluation

- Unilever BrasilDocument6 pagesUnilever Brasilhjheredias1Pas encore d'évaluation

- Nuts and Dried Fruits - Statistical - Yearbook - 2019-2020Document80 pagesNuts and Dried Fruits - Statistical - Yearbook - 2019-2020Tânia Sofia OliveiraPas encore d'évaluation

- Yahoo Symbol ListDocument21 pagesYahoo Symbol ListShubham RohatgiPas encore d'évaluation

- The Edge FD - 10 November 2016Document33 pagesThe Edge FD - 10 November 2016mohdkhidirPas encore d'évaluation

- Tarea 2 Bis Caso Hemingway CorporationDocument10 pagesTarea 2 Bis Caso Hemingway CorporationChesse HerPas encore d'évaluation

- Treasury Operation System, Tripura: Payment Data Input SheetDocument1 pageTreasury Operation System, Tripura: Payment Data Input SheetAnonymous JamqEgqqh1Pas encore d'évaluation

- The Gold StandardDocument3 pagesThe Gold Standardzertar60Pas encore d'évaluation

- Latihan Soal Leasing - Nov2019 - SolusiDocument3 pagesLatihan Soal Leasing - Nov2019 - SolusiABDUL KHALIQ BRUTUPas encore d'évaluation

- Case GalanzDocument7 pagesCase GalanzLeonard LiPas encore d'évaluation

- Business Prospects of Honey MarketingDocument14 pagesBusiness Prospects of Honey MarketingAbubakarr SesayPas encore d'évaluation

- General Management and Marketing Specialisation PDFDocument7 pagesGeneral Management and Marketing Specialisation PDFJiten BendlePas encore d'évaluation

- SamplereportsDocument5 pagesSamplereportsMehul MittalPas encore d'évaluation

- Solomon Success - Company Registry Reform in Solomon IslandsDocument23 pagesSolomon Success - Company Registry Reform in Solomon IslandsADBGADPas encore d'évaluation

- Campus PlacementDocument20 pagesCampus PlacementPrasant SharamaPas encore d'évaluation

- Housing Development Finance Corporation: PrintDocument2 pagesHousing Development Finance Corporation: PrintAbdul Khaliq ChoudharyPas encore d'évaluation

- Charles Munger - Psychology Human MisjudgmentDocument21 pagesCharles Munger - Psychology Human MisjudgmentEmily HunterPas encore d'évaluation