Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Tax Cheat Sheet Exam 2 - CH 7,8,10,11Document2 pagesTax Cheat Sheet Exam 2 - CH 7,8,10,11tyg1992Pas encore d'évaluation

- Track Time 24Document1 pageTrack Time 24Jean Carlos Escurra LagosPas encore d'évaluation

- IFS Report R120Document57 pagesIFS Report R120JoePas encore d'évaluation

- Existential Neuroscience: Self-Esteem Moderates Neuronal Responses To Mortality-Related StimuliDocument8 pagesExistential Neuroscience: Self-Esteem Moderates Neuronal Responses To Mortality-Related StimuliJoePas encore d'évaluation

- Genetic and Neural Correlates of Romantic Relationship SatisfactionDocument12 pagesGenetic and Neural Correlates of Romantic Relationship SatisfactionJoePas encore d'évaluation

- Job DescriptionDocument4 pagesJob DescriptionJoePas encore d'évaluation

- A Sniff of Jam - Blog by DR Daria Luchinskaya - Wales Public Services 2025Document4 pagesA Sniff of Jam - Blog by DR Daria Luchinskaya - Wales Public Services 2025JoePas encore d'évaluation

- Asymmetric Frontal Cortical Activity and Negative Affective Responses To OstracismDocument9 pagesAsymmetric Frontal Cortical Activity and Negative Affective Responses To OstracismJoePas encore d'évaluation

- NSW 145Document9 pagesNSW 145JoePas encore d'évaluation

- Culturing The Adolescent Brain: What Can Neuroscience Learn From Anthropology?Document9 pagesCulturing The Adolescent Brain: What Can Neuroscience Learn From Anthropology?JoePas encore d'évaluation

- NSQ 098Document9 pagesNSQ 098JoePas encore d'évaluation

- NSW 164Document11 pagesNSW 164JoePas encore d'évaluation

- NSN 012Document9 pagesNSN 012JoePas encore d'évaluation

- Neural Correlates of Three Types of Negative Life Events During Angry Face Processing in AdolescentsDocument9 pagesNeural Correlates of Three Types of Negative Life Events During Angry Face Processing in AdolescentsJoePas encore d'évaluation

- Beyond Self-Serving Bias: Diffusion of Responsibility Reduces Sense of Agency and Outcome MonitoringDocument8 pagesBeyond Self-Serving Bias: Diffusion of Responsibility Reduces Sense of Agency and Outcome MonitoringJoePas encore d'évaluation

- © The Author (2016) - Published by Oxford University Press. For Permissions, Please EmailDocument32 pages© The Author (2016) - Published by Oxford University Press. For Permissions, Please EmailJoePas encore d'évaluation

- NSW 090Document12 pagesNSW 090JoePas encore d'évaluation

- NSQ 098Document9 pagesNSQ 098JoePas encore d'évaluation

- Neural Mechanisms of Social Influence in AdolescenceDocument10 pagesNeural Mechanisms of Social Influence in AdolescenceJoePas encore d'évaluation

- NSW 182Document35 pagesNSW 182JoePas encore d'évaluation

- The Neural Basis of Improved Cognitive Performance by Threat of ShockDocument10 pagesThe Neural Basis of Improved Cognitive Performance by Threat of ShockJoePas encore d'évaluation

- NSQ 002Document7 pagesNSQ 002JoePas encore d'évaluation

- NST 151Document13 pagesNST 151JoePas encore d'évaluation

- Self-Esteem Modulates Dorsal Medial Prefrontal Cortical Response To Self-Positivity Bias in Implicit Self-Relevant ProcessingDocument5 pagesSelf-Esteem Modulates Dorsal Medial Prefrontal Cortical Response To Self-Positivity Bias in Implicit Self-Relevant ProcessingJoePas encore d'évaluation

- Neuroimaging Self-Esteem: A fMRI Study of Individual Differences in WomenDocument10 pagesNeuroimaging Self-Esteem: A fMRI Study of Individual Differences in WomenJoePas encore d'évaluation

- The Matter of Motivation: Striatal Resting-State Connec-Tivity Is Dissociable Between Grit and Growth MindsetDocument7 pagesThe Matter of Motivation: Striatal Resting-State Connec-Tivity Is Dissociable Between Grit and Growth MindsetJoePas encore d'évaluation

- Neural Correlates of Social Exclusion During Adolescence: Understanding The Distress of Peer RejectionDocument15 pagesNeural Correlates of Social Exclusion During Adolescence: Understanding The Distress of Peer RejectionJoePas encore d'évaluation

- Increased Neural Responses To Empathy For Pain Might Explain How Acute Stress Increases ProsocialityDocument8 pagesIncreased Neural Responses To Empathy For Pain Might Explain How Acute Stress Increases ProsocialityJoePas encore d'évaluation

- Priming For Self-Esteem Influences The Monitoring of One's Own PerformanceDocument9 pagesPriming For Self-Esteem Influences The Monitoring of One's Own PerformanceJoePas encore d'évaluation

- An Event-Related Examination of Neural Activity During Social InteractionsDocument7 pagesAn Event-Related Examination of Neural Activity During Social InteractionsJoePas encore d'évaluation

- Region of Interest Analysis For fMRI: Tools of The TradeDocument4 pagesRegion of Interest Analysis For fMRI: Tools of The TradeJoePas encore d'évaluation

- Culturing The Adolescent Brain: What Can Neuroscience Learn From Anthropology?Document9 pagesCulturing The Adolescent Brain: What Can Neuroscience Learn From Anthropology?JoePas encore d'évaluation

- Downloadfile 30 PDFDocument114 pagesDownloadfile 30 PDFYianniAnd Sophia0% (1)

- 1601 CDocument16 pages1601 CROGELIO QUIAZON100% (1)

- Claims Payer List For Unitedhealthcare, Affiliates and Strategic AlliancesDocument3 pagesClaims Payer List For Unitedhealthcare, Affiliates and Strategic AlliancesSri APas encore d'évaluation

- Concept Notes On International BusinessDocument228 pagesConcept Notes On International BusinessashmitPas encore d'évaluation

- SWOT Analysis - Ex1Document7 pagesSWOT Analysis - Ex1Paresh MehtaPas encore d'évaluation

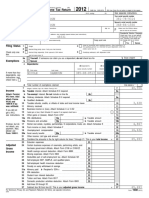

- Omb No. 1545-0008 Omb No. 1545-0008Document2 pagesOmb No. 1545-0008 Omb No. 1545-0008Luke NyePas encore d'évaluation

- Jorion VaR DisclosuresDocument35 pagesJorion VaR DisclosuresMatheus Monteiro RossaPas encore d'évaluation

- Handover Shift Form (Downloadable by Laptop) PDFDocument1 pageHandover Shift Form (Downloadable by Laptop) PDFaldi anggaraPas encore d'évaluation

- Top 100 Contractors Report Fiscal Year 2010Document156 pagesTop 100 Contractors Report Fiscal Year 2010Ansh ShuklaPas encore d'évaluation

- A218 DocumentDocument9 pagesA218 DocumentJose AlmontePas encore d'évaluation

- Creditcardrush JSONDocument31 pagesCreditcardrush JSONAnderson PangestiajiPas encore d'évaluation

- 17.3 - The New DealDocument2 pages17.3 - The New DealPablo DavidPas encore d'évaluation

- RecruiterDocument7 pagesRecruiterashish ojhaPas encore d'évaluation

- Women in Entrepreneurship Report Endeavor Insight and GoogleDocument28 pagesWomen in Entrepreneurship Report Endeavor Insight and GoogleAntonio VieraPas encore d'évaluation

- Gi Bill PowerpointDocument10 pagesGi Bill Powerpointapi-249624179Pas encore d'évaluation

- Exercise 9-5 No 9-20Document9 pagesExercise 9-5 No 9-20Kent LumanasPas encore d'évaluation

- Weekly Sentiment Paper: Distributed By: One Financial Written By: Andrei WogenDocument13 pagesWeekly Sentiment Paper: Distributed By: One Financial Written By: Andrei WogenAndrei Alexander WogenPas encore d'évaluation

- CIR vs. Lednicky (1964)Document1 pageCIR vs. Lednicky (1964)Emil BautistaPas encore d'évaluation

- Colgate-Palmolive Company 2Document20 pagesColgate-Palmolive Company 2Arun JothyPas encore d'évaluation

- MMB November 2022 ForecastDocument102 pagesMMB November 2022 ForecastMichael AchterlingPas encore d'évaluation

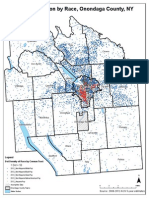

- CNY Segregation MapsDocument13 pagesCNY Segregation MapsTim KnaussPas encore d'évaluation

- Digest RR 8-2019Document2 pagesDigest RR 8-2019Nikki GarciaPas encore d'évaluation

- Fastest Growing Companies - Top 150Document12 pagesFastest Growing Companies - Top 150trungPas encore d'évaluation

- Chapter 31 Open-Economy Macroeconomics - Basic ConceptsDocument26 pagesChapter 31 Open-Economy Macroeconomics - Basic ConceptsHIỀN HOÀNG BẢO MỸPas encore d'évaluation

- De 4Document4 pagesDe 4AmandaPas encore d'évaluation

- 2018 Capitalize For Kids ConferenceDocument1 page2018 Capitalize For Kids Conferencemarketfolly.comPas encore d'évaluation

- CitibankDocument50 pagesCitibankUtsav Mahendra100% (1)

- Citi BankDocument3 pagesCiti Bankmuffadal0307Pas encore d'évaluation