Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- SPA Sample SaleDocument1 pageSPA Sample SalejrfbalamientoPas encore d'évaluation

- Affidavit of Loss of DiplomaDocument1 pageAffidavit of Loss of DiplomajrfbalamientoPas encore d'évaluation

- Securities and Exchange Commission Revokes Rappler Inc.'s RegistrationDocument29 pagesSecurities and Exchange Commission Revokes Rappler Inc.'s RegistrationSunStar Philippine NewsPas encore d'évaluation

- Torts Digest (Damages, 1-6)Document7 pagesTorts Digest (Damages, 1-6)Shailah Leilene Arce BrionesPas encore d'évaluation

- Virgilio S. Delima V. Susan Mercaida Gois GR NO. 178352 - June 17, 2008 FactsDocument6 pagesVirgilio S. Delima V. Susan Mercaida Gois GR NO. 178352 - June 17, 2008 FactsNikki BarenaPas encore d'évaluation

- Aafawafvasfbeargv, Aewewmgemwageaw G Ew Gew G GWG WG WG WG W GW G WG W G WG W GW G WG W GW G WDocument1 pageAafawafvasfbeargv, Aewewmgemwageaw G Ew Gew G GWG WG WG WG W GW G WG W G WG W GW G WG W GW G WjrfbalamientoPas encore d'évaluation

- Affidavit of The Same PersonDocument1 pageAffidavit of The Same PersonjrfbalamientoPas encore d'évaluation

- Do 174Document1 pageDo 174jrfbalamientoPas encore d'évaluation

- Mold AddendumDocument2 pagesMold AddendumjrfbalamientoPas encore d'évaluation

- Legal Edge Bar Review: Lecture On Evidence For 2017 Bar ExaminationDocument258 pagesLegal Edge Bar Review: Lecture On Evidence For 2017 Bar ExaminationjrfbalamientoPas encore d'évaluation

- Preti RalDocument1 pagePreti RaljrfbalamientoPas encore d'évaluation

- Contract of ContractDocument5 pagesContract of ContractjrfbalamientoPas encore d'évaluation

- 1233rasf Asfas Asf A Fas Fa F Af Af Af As F Af A Fa Fa Fa SF As FaDocument1 page1233rasf Asfas Asf A Fas Fa F Af Af Af As F Af A Fa Fa Fa SF As FajrfbalamientoPas encore d'évaluation

- Law 1 ObliconDocument1 pageLaw 1 ObliconjrfbalamientoPas encore d'évaluation

- Deed of LeaseDocument4 pagesDeed of LeasejrfbalamientoPas encore d'évaluation

- Pinsp v. CasimiroDocument14 pagesPinsp v. CasimirojrfbalamientoPas encore d'évaluation

- Maybe The NightDocument4 pagesMaybe The NightjrfbalamientoPas encore d'évaluation

- Ariel v. OrlandoDocument7 pagesAriel v. OrlandojrfbalamientoPas encore d'évaluation

- MotionDocument1 pageMotionjrfbalamientoPas encore d'évaluation

- Motion For Early ResolutionDocument1 pageMotion For Early ResolutionjrfbalamientoPas encore d'évaluation

- Business Permit and Licensing Office: January 17, 2018Document1 pageBusiness Permit and Licensing Office: January 17, 2018jrfbalamientoPas encore d'évaluation

- TrainDocument4 pagesTrainjrfbalamientoPas encore d'évaluation

- Pinsp v. CasimiroDocument14 pagesPinsp v. CasimirojrfbalamientoPas encore d'évaluation

- Pinsp v. CasimiroDocument14 pagesPinsp v. CasimirojrfbalamientoPas encore d'évaluation

- Lease ContractDocument3 pagesLease ContractShingo TakasugiPas encore d'évaluation

- Agreement To Constitute Perpetual Easment - ReviewedDocument3 pagesAgreement To Constitute Perpetual Easment - ReviewedjrfbalamientoPas encore d'évaluation

- Stokes v. Malayan Insurance, 127 SCRA 766 (1984)Document4 pagesStokes v. Malayan Insurance, 127 SCRA 766 (1984)KristineSherikaChyPas encore d'évaluation

- Hizon Notes - Legal EthicsDocument43 pagesHizon Notes - Legal EthicsAQAAPas encore d'évaluation

- UST GN 2011 - Criminal Law ProperDocument262 pagesUST GN 2011 - Criminal Law ProperGhost100% (9)

- How To Conduct Direct Examination #Practice-CourtDocument12 pagesHow To Conduct Direct Examination #Practice-CourtEarl TagraPas encore d'évaluation

- Libertas SRC NotesDocument14 pagesLibertas SRC NotesjrfbalamientoPas encore d'évaluation

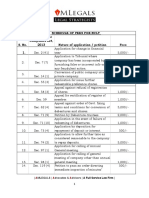

- Schedule of Fees in NCLT 1Document4 pagesSchedule of Fees in NCLT 1Lavkesh BhambhaniPas encore d'évaluation

- IPR Question Paper 2021Document3 pagesIPR Question Paper 2021Prateek DwivediPas encore d'évaluation

- Final Supplementary Report 4Document33 pagesFinal Supplementary Report 4Upamanyu HazarikaPas encore d'évaluation

- Nolasco Vs EnrileDocument11 pagesNolasco Vs EnrileJay-r ValdezPas encore d'évaluation

- Valera Vs InsertoDocument2 pagesValera Vs InsertoElerlenne LimPas encore d'évaluation

- GQ 2.0 - Alternative and Facultative ObligationsDocument6 pagesGQ 2.0 - Alternative and Facultative ObligationsCHARRYSAH TABAOSARESPas encore d'évaluation

- Writ PetitionDocument31 pagesWrit PetitionRoshan Singh100% (1)

- LLDA Vs CADocument2 pagesLLDA Vs CASui100% (1)

- Answer To Tuadles ComplaintDocument6 pagesAnswer To Tuadles ComplaintResci Angelli Rizada-NolascoPas encore d'évaluation

- The Evolution of Criminal Law and Police During The Industrial Revolution - 2007Document40 pagesThe Evolution of Criminal Law and Police During The Industrial Revolution - 2007anaximansPas encore d'évaluation

- Aligarh Muslim University: Malappuram Centre, KeralaDocument11 pagesAligarh Muslim University: Malappuram Centre, KeralaVibhu TeotiaPas encore d'évaluation

- G.R. No. L-10126 October 22, 1957 Salud Villanueva Vda. de Bataclan V. Mariano Medina FactsDocument17 pagesG.R. No. L-10126 October 22, 1957 Salud Villanueva Vda. de Bataclan V. Mariano Medina FactsAudreyPas encore d'évaluation

- Chua-Qua Vs ClaveDocument12 pagesChua-Qua Vs ClaveJose BonifacioPas encore d'évaluation

- 7 AppendicesDocument14 pages7 AppendicesYevrah ZeuqirnePas encore d'évaluation

- Universiti Teknologi Mara Final Examination: Confidential LW/APR 2011/LAW572/342Document5 pagesUniversiti Teknologi Mara Final Examination: Confidential LW/APR 2011/LAW572/342FAZLYNPas encore d'évaluation

- Luzon Brokerage v. Maritime Building, 43 SCRA 93, January 21, 1972Document18 pagesLuzon Brokerage v. Maritime Building, 43 SCRA 93, January 21, 1972Eszle Ann L. ChuaPas encore d'évaluation

- Diane Neal Ruling 9-18-18 PDFDocument3 pagesDiane Neal Ruling 9-18-18 PDFDaily FreemanPas encore d'évaluation

- BNI Membership Application FormDocument2 pagesBNI Membership Application FormSatya PrakashPas encore d'évaluation

- Professional AdjustmentDocument19 pagesProfessional AdjustmentAlsalman AnamPas encore d'évaluation

- Marriage Process at A GlanceDocument4 pagesMarriage Process at A GlanceAlvin YapPas encore d'évaluation

- The BeatitudesDocument3 pagesThe BeatitudesRafael OngPas encore d'évaluation

- United States Court of Appeals Second Circuit.: No. 486, Docket 32662Document3 pagesUnited States Court of Appeals Second Circuit.: No. 486, Docket 32662Scribd Government DocsPas encore d'évaluation

- in Re in The Matter of The Petition To Approve The Will of Ruperta Palagas Vs Palaganas GR No. 169144 January 26, 2011Document4 pagesin Re in The Matter of The Petition To Approve The Will of Ruperta Palagas Vs Palaganas GR No. 169144 January 26, 2011Marianne Shen PetillaPas encore d'évaluation

- Lagcao Vs Labra - DigestDocument2 pagesLagcao Vs Labra - DigestJoseph AlulodPas encore d'évaluation

- Code of Conduct - MetvyDocument5 pagesCode of Conduct - MetvyCherryberryPas encore d'évaluation

- Rubenstein v. Frey - Document No. 11Document3 pagesRubenstein v. Frey - Document No. 11Justia.comPas encore d'évaluation

- Asuncion vs. CADocument6 pagesAsuncion vs. CAKennex de DiosPas encore d'évaluation

- Legal Structure For Non Profit OrganizationDocument4 pagesLegal Structure For Non Profit OrganizationMikey MadRat0% (1)