Vous aimerez peut-être aussi

- Parents Guide To SNT - 05 - 2021Document14 pagesParents Guide To SNT - 05 - 2021YanoPas encore d'évaluation

- Directory of Womens Organization PDFDocument653 pagesDirectory of Womens Organization PDFYano0% (1)

- AIA Philam Life Life Insurance Trust DeedDocument1 pageAIA Philam Life Life Insurance Trust DeedYanoPas encore d'évaluation

- The Best Answer To "Sell Me This Pen" - 4 Tips To Sell in A Super Competitive IndustryDocument4 pagesThe Best Answer To "Sell Me This Pen" - 4 Tips To Sell in A Super Competitive IndustryYanoPas encore d'évaluation

- Abaca Fibre PDFDocument4 pagesAbaca Fibre PDFYanoPas encore d'évaluation

- Registered Veterinary Drugs and Products-Manufacturers Updated PDFDocument5 pagesRegistered Veterinary Drugs and Products-Manufacturers Updated PDFYanoPas encore d'évaluation

- PhilHealth Guidebook PDFDocument127 pagesPhilHealth Guidebook PDFYanoPas encore d'évaluation

- SuperwormsDocument2 pagesSuperwormsYanoPas encore d'évaluation

- 2 Inbar A Manual For Vegetative Propagation of Bamboos PDFDocument74 pages2 Inbar A Manual For Vegetative Propagation of Bamboos PDFYano100% (1)

- Rankings of Insurance Brokers - Premiums Produced - 2016 PDFDocument3 pagesRankings of Insurance Brokers - Premiums Produced - 2016 PDFYanoPas encore d'évaluation

- Bangladesh Seed Production PDFDocument125 pagesBangladesh Seed Production PDFYanoPas encore d'évaluation

- Philippines Electronics 2017 PDFDocument21 pagesPhilippines Electronics 2017 PDFYanoPas encore d'évaluation

- Net Income of Non Life Insurance Companies - Year 2017 PDFDocument2 pagesNet Income of Non Life Insurance Companies - Year 2017 PDFYanoPas encore d'évaluation

- Assets of Non Life Insurance Companies - Year 2017 PDFDocument2 pagesAssets of Non Life Insurance Companies - Year 2017 PDFYanoPas encore d'évaluation

- Premiums Earned of Non Life Insurance Companies - Year 2017 PDFDocument2 pagesPremiums Earned of Non Life Insurance Companies - Year 2017 PDFYanoPas encore d'évaluation

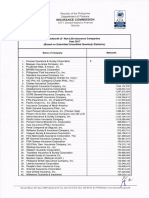

- Networth of Non Life Insurance Companies - Year 2017 PDFDocument2 pagesNetworth of Non Life Insurance Companies - Year 2017 PDFYanoPas encore d'évaluation

- Bacterial Wilt Management in Tomato - South Asia PDFDocument18 pagesBacterial Wilt Management in Tomato - South Asia PDFYanoPas encore d'évaluation

- Freshman RECOMMENDATION FORMS PDFDocument3 pagesFreshman RECOMMENDATION FORMS PDFYanoPas encore d'évaluation

- Pps Arable Vegetable Crops 2009Document17 pagesPps Arable Vegetable Crops 2009YanoPas encore d'évaluation

- Olericulture I PM XIDocument160 pagesOlericulture I PM XIYano100% (1)

- Vegetable Production Best Management Practices To Minimize Nutrient LossDocument6 pagesVegetable Production Best Management Practices To Minimize Nutrient LossYanoPas encore d'évaluation

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Organizing A BusinessDocument27 pagesOrganizing A BusinessMafe Marquez100% (1)

- Chapter 9 - The Organizational PlanDocument14 pagesChapter 9 - The Organizational PlanFatima ChowdhuryPas encore d'évaluation

- 121604053-MIS-Domino-s PizzaDocument32 pages121604053-MIS-Domino-s PizzaAnuj SharmaPas encore d'évaluation

- UNESCO TA AgreementDocument29 pagesUNESCO TA AgreementSandeep JoshiPas encore d'évaluation

- As 60068.2.17-2003 Environmental Testing Tests - Test Q - SealingDocument6 pagesAs 60068.2.17-2003 Environmental Testing Tests - Test Q - SealingSAI Global - APACPas encore d'évaluation

- Laporan Keuangan PT BTEL 31 Des 2021Document141 pagesLaporan Keuangan PT BTEL 31 Des 2021Muhammad Mahdi HakimPas encore d'évaluation

- Nomura Hong Kong Property 120213Document16 pagesNomura Hong Kong Property 120213dickersonwtsPas encore d'évaluation

- Topic 6 Partnership: 6.1 FormationDocument5 pagesTopic 6 Partnership: 6.1 FormationxxpjulxxPas encore d'évaluation

- Notice: Applications, Hearings, Determinations, Etc.: Glacial Ridge Wind Power LLC Et Al.Document2 pagesNotice: Applications, Hearings, Determinations, Etc.: Glacial Ridge Wind Power LLC Et Al.Justia.comPas encore d'évaluation

- 16GM0014-Re-ITB - Bid Docs - FINALDocument104 pages16GM0014-Re-ITB - Bid Docs - FINALReynaldo PesqueraPas encore d'évaluation

- Marketing in Hong KongDocument3 pagesMarketing in Hong KongMeenakshi ShekhawatPas encore d'évaluation

- Ozhouse Clean - PolicyDocument2 pagesOzhouse Clean - Policyanish100% (1)

- Company Law QuestionsDocument9 pagesCompany Law QuestionsBadrinath ChavanPas encore d'évaluation

- Coinbase EulaDocument4 pagesCoinbase Eulafloorman67Pas encore d'évaluation

- Strategic Management : Gregory G. Dess and G. T. LumpkinDocument19 pagesStrategic Management : Gregory G. Dess and G. T. LumpkinJeramz QuijanoPas encore d'évaluation

- Porter's Five Force Analysis of Food Processing Industry: Marketing StrategyDocument30 pagesPorter's Five Force Analysis of Food Processing Industry: Marketing Strategydeepak boraPas encore d'évaluation

- Case Discussion-1Document2 pagesCase Discussion-1gülraPas encore d'évaluation

- Millicon PresentationDocument123 pagesMillicon Presentationjgvp2010Pas encore d'évaluation

- SiddharthaDocument9 pagesSiddharthaprajwolt0150Pas encore d'évaluation

- Terminal Handling Charges: London Heathrow AirportDocument2 pagesTerminal Handling Charges: London Heathrow AirportMuhammad SiddiuqiPas encore d'évaluation

- Web Design Company-ECommerce Software-Website Development - Seo ExpertDocument12 pagesWeb Design Company-ECommerce Software-Website Development - Seo ExpertKrishnaKumarPas encore d'évaluation

- Gabriela A. Dicesare: ObjectivesDocument4 pagesGabriela A. Dicesare: ObjectivesIsabel GilPas encore d'évaluation

- Preface NewDocument30 pagesPreface NewWiddic100% (1)

- Είδη Μεταφοράς ή Συσκευασίας Από Πλαστικές Ύλες.2016714104726Document959 pagesΕίδη Μεταφοράς ή Συσκευασίας Από Πλαστικές Ύλες.2016714104726tracePas encore d'évaluation

- Resume HemaDocument2 pagesResume Hemaanil007rajuPas encore d'évaluation

- Presentation HIRARCDocument12 pagesPresentation HIRARCahmad syouqiPas encore d'évaluation

- Grocery Stocker JD Rev 051117Document2 pagesGrocery Stocker JD Rev 051117Robert PetrutPas encore d'évaluation

- Metrolab Industries Inc Vs Roldan-Confesor - 108855 - February 28 2996 - KapDocument28 pagesMetrolab Industries Inc Vs Roldan-Confesor - 108855 - February 28 2996 - KapJia Chu ChuaPas encore d'évaluation

- Project On NJ India Invest PVT LTDDocument68 pagesProject On NJ India Invest PVT LTDbabloo200650% (2)

- Strategic and Marketing Planning Lesson 5 POMDocument18 pagesStrategic and Marketing Planning Lesson 5 POMJesfie VillegasPas encore d'évaluation