Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Datasheet LIVEO Q7-2243Document2 pagesDatasheet LIVEO Q7-2243felipe geymerPas encore d'évaluation

- Group Risk Management Policy May2021.pdf - DownloadassetDocument6 pagesGroup Risk Management Policy May2021.pdf - DownloadassetMg MgPas encore d'évaluation

- Credit File Dispute Lawyers Do You Have An Error On Your Credit File?Document7 pagesCredit File Dispute Lawyers Do You Have An Error On Your Credit File?Anthony RobertsPas encore d'évaluation

- BN4206 Riks and ValueDocument10 pagesBN4206 Riks and ValueKarma SherpaPas encore d'évaluation

- Interview Q & A - Accenture, Wipro, Ibm, Etc.,-01.05.2018Document9 pagesInterview Q & A - Accenture, Wipro, Ibm, Etc.,-01.05.2018Mohamedgous TahasildarPas encore d'évaluation

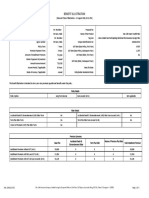

- Benefit Illustration: UIN: 104N116V02 Page 1 of 3Document3 pagesBenefit Illustration: UIN: 104N116V02 Page 1 of 3Ravindar aPas encore d'évaluation

- PPSSH Aligned Opcrf Career Stage 2 Scoring Standards Tool Final V3Document17 pagesPPSSH Aligned Opcrf Career Stage 2 Scoring Standards Tool Final V3RIZA Y. LABUSTROPas encore d'évaluation

- Prajya June 23 - Digital VersionDocument68 pagesPrajya June 23 - Digital VersionaniashokPas encore d'évaluation

- PROJECT-PROPOSAL-NSTP (1) DDDDocument9 pagesPROJECT-PROPOSAL-NSTP (1) DDDNavarro, Marianne B. BSBA FMPas encore d'évaluation

- "Pioneer or Imitate? An Analysis of Business Imitations": AuthorsDocument8 pages"Pioneer or Imitate? An Analysis of Business Imitations": AuthorsThuong Vy MinhPas encore d'évaluation

- Mohamed Ismail Mohamed Riyath - An Overview of Asset Pricing Models (2005, GRIN Verlag)Document39 pagesMohamed Ismail Mohamed Riyath - An Overview of Asset Pricing Models (2005, GRIN Verlag)EVERYTHING FOOTBALLPas encore d'évaluation

- What Can I Do With My Degree in (2837)Document18 pagesWhat Can I Do With My Degree in (2837)Trần Phương QuyênPas encore d'évaluation

- 3rd GovAcc 1SAY2324Document9 pages3rd GovAcc 1SAY2324Grand DuelistPas encore d'évaluation

- Thesis. Bui Tung LamDocument89 pagesThesis. Bui Tung LamTuấn ĐinhPas encore d'évaluation

- Jun18l1-Ep02 QaDocument29 pagesJun18l1-Ep02 Qajuan0% (1)

- Exemplu TEZA - Baba - Camelia - Mirela-Teza - de - Abilitare - ENGDocument141 pagesExemplu TEZA - Baba - Camelia - Mirela-Teza - de - Abilitare - ENGgabir98Pas encore d'évaluation

- Market Participants in Equities Name:-Sayali Ramesh Keluskar STD: - S.Y.Bfm ROLL NO: - 18Document7 pagesMarket Participants in Equities Name:-Sayali Ramesh Keluskar STD: - S.Y.Bfm ROLL NO: - 18Chikna ballPas encore d'évaluation

- Public Health Budget (2012-2022)Document3 pagesPublic Health Budget (2012-2022)Fahim HasnatPas encore d'évaluation

- Configuration Management SystemDocument4 pagesConfiguration Management SystemAngel Rose ZamoraPas encore d'évaluation

- Geovisions Terms and ConditionsDocument3 pagesGeovisions Terms and ConditionssanjinPas encore d'évaluation

- Money Habits - Saddleback ChurchDocument80 pagesMoney Habits - Saddleback ChurchAndriamihaja MichelPas encore d'évaluation

- API SP - POP.TOTL DS2 en Excel v2 820893Document53 pagesAPI SP - POP.TOTL DS2 en Excel v2 820893ajaywadhwaniPas encore d'évaluation

- QSCM Upto 1st I.A.Document10 pagesQSCM Upto 1st I.A.Md.saifaadil AttarPas encore d'évaluation

- SFM Marking Scheme 2019Document10 pagesSFM Marking Scheme 2019Dilu - SPas encore d'évaluation

- Best of Linkedin Pages Posts: With 8 Best-In-Class ExamplesDocument7 pagesBest of Linkedin Pages Posts: With 8 Best-In-Class ExamplesNeoGellinPas encore d'évaluation

- Business Maths - BBA 1yr - Unit 1Document107 pagesBusiness Maths - BBA 1yr - Unit 1ADISH JAINPas encore d'évaluation

- Group 1 - Planning and Organizing The ConferenceDocument21 pagesGroup 1 - Planning and Organizing The ConferenceJay DimesPas encore d'évaluation

- Virgin Atlantic CaseDocument10 pagesVirgin Atlantic CaseSunny_9897Pas encore d'évaluation

- Samrah Qamar Khan: Roll No. 71Document7 pagesSamrah Qamar Khan: Roll No. 71Samrah QamarPas encore d'évaluation