Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- 261 A Syllabus Spring 2012 Full VersionDocument17 pages261 A Syllabus Spring 2012 Full VersionMikhail StrukovPas encore d'évaluation

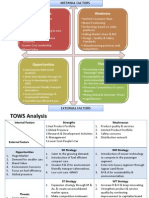

- Tata Motors SWOT TOWS CPM MatrixDocument6 pagesTata Motors SWOT TOWS CPM MatrixPreetam Pandey33% (3)

- M&A CH# 08 (Summary)Document14 pagesM&A CH# 08 (Summary)SheiryPas encore d'évaluation

- TOMCODocument11 pagesTOMCOjanak1208Pas encore d'évaluation

- Strategic Management Project OnDocument12 pagesStrategic Management Project Onashutoshy vermaPas encore d'évaluation

- MarketingDocument13 pagesMarketingashutoshy vermaPas encore d'évaluation

- HRM Case StudyDocument3 pagesHRM Case Studyashutoshy vermaPas encore d'évaluation

- REPORT On Competitive AdvertisingDocument30 pagesREPORT On Competitive Advertisingashutoshy vermaPas encore d'évaluation

- Advertising AwardsDocument9 pagesAdvertising Awardsashutoshy vermaPas encore d'évaluation

- Analysis of Ad CampaignDocument8 pagesAnalysis of Ad Campaignashutoshy vermaPas encore d'évaluation

- Analysis of Ad CampaignDocument8 pagesAnalysis of Ad Campaignashutoshy vermaPas encore d'évaluation

- Crompton Greaves 23octDocument3 pagesCrompton Greaves 23octSumit AroraPas encore d'évaluation

- Rmbe Afar For PrintingDocument18 pagesRmbe Afar For PrintingjxnPas encore d'évaluation

- Creative AdvertisingDocument2 pagesCreative AdvertisingVinit GaikwadPas encore d'évaluation

- Holding Tight: CRISIL Research Survey of Private Equity and Venture CapitalDocument20 pagesHolding Tight: CRISIL Research Survey of Private Equity and Venture CapitalSantosh HiredesaiPas encore d'évaluation

- Complexities of Compliance Can Be Managed: HITRUST Approval For CSF Security AssessmentsDocument17 pagesComplexities of Compliance Can Be Managed: HITRUST Approval For CSF Security AssessmentsSwetha RavichandranPas encore d'évaluation

- Introduction To Business Combinations and The Conceptual FrameworkDocument15 pagesIntroduction To Business Combinations and The Conceptual FrameworkAhmed FahmyPas encore d'évaluation

- Merger AgreementDocument9 pagesMerger AgreementRafael Sosa ArveloPas encore d'évaluation

- PR 373Document3 pagesPR 373Anonymous Feglbx5Pas encore d'évaluation

- Chapter 8 Share Based (874 899)Document26 pagesChapter 8 Share Based (874 899)VijayaPas encore d'évaluation

- FDI in SBR-PublicDocument9 pagesFDI in SBR-PublicflexrajanPas encore d'évaluation

- Dentists: TOP Dental Marketing TipsDocument18 pagesDentists: TOP Dental Marketing TipsteodoraPas encore d'évaluation

- E-Commerce in India: A Game Changer For The EconomyDocument52 pagesE-Commerce in India: A Game Changer For The EconomyGokul BaskerPas encore d'évaluation

- Doing Business in Mexico 2023Document86 pagesDoing Business in Mexico 2023pipanemaPas encore d'évaluation

- Corpo Book Aquino Questions Finals 1Document25 pagesCorpo Book Aquino Questions Finals 1Alex MelegritoPas encore d'évaluation

- The Cash Cows Mathias Bohn, Rodrigo Garcia, Marlène Luce, Roman Zanoli HEC Paris Paris, March 1, 2019Document106 pagesThe Cash Cows Mathias Bohn, Rodrigo Garcia, Marlène Luce, Roman Zanoli HEC Paris Paris, March 1, 2019ArvinPas encore d'évaluation

- Coates's Exhibit CDocument103 pagesCoates's Exhibit CChris HerzecaPas encore d'évaluation

- Note Purchase Agreement Template-With CapDocument14 pagesNote Purchase Agreement Template-With CapDavid Jay Mor50% (2)

- A Project Report On: Indian BankingDocument35 pagesA Project Report On: Indian BankingRishabh GoyalPas encore d'évaluation

- Arcelor Mittal MergerDocument26 pagesArcelor Mittal MergerPuja AgarwalPas encore d'évaluation

- Moore Medical CorporationDocument6 pagesMoore Medical CorporationMitesh Patel100% (1)

- Fast Moving Consumer Goods (FMCG)Document49 pagesFast Moving Consumer Goods (FMCG)Tahira KhanPas encore d'évaluation

- S4HANA Vs ECCDocument32 pagesS4HANA Vs ECCRam C100% (1)

- Transition To PFRS (The Beginning of The Earliest Period For Which Entity Presents Full Comparative InformationDocument8 pagesTransition To PFRS (The Beginning of The Earliest Period For Which Entity Presents Full Comparative InformationMary Joy Morales BuquiranPas encore d'évaluation

- Decision Models For Airline Passenger and Cargo Network AlliancesDocument126 pagesDecision Models For Airline Passenger and Cargo Network AlliancesArathi KrishnaPas encore d'évaluation

- CDD Acctg. For Bus - Co Preliminary ExaminationDocument25 pagesCDD Acctg. For Bus - Co Preliminary ExaminationMaryjoy Sarzadilla JuanataPas encore d'évaluation

- Value Investors Club - Kraton Performance Polymers (Kra)Document5 pagesValue Investors Club - Kraton Performance Polymers (Kra)Lukas SavickasPas encore d'évaluation