Vous aimerez peut-être aussi

- Advice From The OracleDocument211 pagesAdvice From The OracleAyaz Zafar100% (11)

- Investing AdviceDocument9 pagesInvesting AdviceAltrosas100% (1)

- How To Make Money in Value Stocks - First Edition PDFDocument70 pagesHow To Make Money in Value Stocks - First Edition PDFNitin Kumar100% (1)

- Complete Guide To Value InvestingDocument59 pagesComplete Guide To Value InvestingPaulo TrickPas encore d'évaluation

- Warren Buffet PrinciplesDocument6 pagesWarren Buffet PrinciplesRakesh BuffetPas encore d'évaluation

- The Warren Buffett Way (Review and Analysis of Hagstrom's Book)D'EverandThe Warren Buffett Way (Review and Analysis of Hagstrom's Book)Évaluation : 5 sur 5 étoiles5/5 (1)

- Warren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageD'EverandWarren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageÉvaluation : 4.5 sur 5 étoiles4.5/5 (109)

- The Keys To Successful InvestingDocument4 pagesThe Keys To Successful InvestingArnaldoBritoAraújoPas encore d'évaluation

- Value Investing and Behavioral Finance - Chris Browne To Colubia Business School PDFDocument15 pagesValue Investing and Behavioral Finance - Chris Browne To Colubia Business School PDFFavio C. Osorio Polar100% (1)

- Lesson From Top 10 Investor in World PDFDocument14 pagesLesson From Top 10 Investor in World PDFUmang Aggarwal50% (2)

- Warren Buffett: The Life, Lessons & Rules for SuccessD'EverandWarren Buffett: The Life, Lessons & Rules for SuccessÉvaluation : 3.5 sur 5 étoiles3.5/5 (5)

- The Best Investors PDFDocument14 pagesThe Best Investors PDFcocosan100% (2)

- Warren Buffett's Investment StrategiesDocument2 pagesWarren Buffett's Investment StrategiesroasroasroasPas encore d'évaluation

- Your Stock Market Investing Bible: Warren Buffett and Benjamin Graham Value Investing Strategies How to Become Intelligent Investor: Stock Market Investing Books, #1D'EverandYour Stock Market Investing Bible: Warren Buffett and Benjamin Graham Value Investing Strategies How to Become Intelligent Investor: Stock Market Investing Books, #1Évaluation : 5 sur 5 étoiles5/5 (1)

- Discount StocksDocument19 pagesDiscount StocksPete100% (1)

- Corporate Finance EssentialsDocument239 pagesCorporate Finance Essentialsssj9Pas encore d'évaluation

- World's Famous InvestorsDocument9 pagesWorld's Famous InvestorsDasher_No_1Pas encore d'évaluation

- Warren Buffett's Wealth Strategies: How to Get Rich Off Real Estate Investing in a Smart WayD'EverandWarren Buffett's Wealth Strategies: How to Get Rich Off Real Estate Investing in a Smart WayÉvaluation : 3 sur 5 étoiles3/5 (3)

- Warren Buffett: 48 Empowering Lessons from Warren Buffet for Life Changing Success in Investing, Business and LifeD'EverandWarren Buffett: 48 Empowering Lessons from Warren Buffet for Life Changing Success in Investing, Business and LifeÉvaluation : 4 sur 5 étoiles4/5 (5)

- Invest Like Buffett: Learn the Investment Strategies that Made Warren Buffett RichD'EverandInvest Like Buffett: Learn the Investment Strategies that Made Warren Buffett RichÉvaluation : 2 sur 5 étoiles2/5 (1)

- Will Warren Buffett Continue Leading Berkshire Hathaway to SuccessDocument11 pagesWill Warren Buffett Continue Leading Berkshire Hathaway to SuccessJerome Vincent FranciscoPas encore d'évaluation

- The 10 Best Investors in The WorldDocument14 pagesThe 10 Best Investors in The WorldAditya BhidePas encore d'évaluation

- Value Investing: Review of Warren Buffett's Investment Philosophy and PracticeDocument13 pagesValue Investing: Review of Warren Buffett's Investment Philosophy and PracticeMeester KewpiePas encore d'évaluation

- The Seven Golden Rules of InvestingDocument27 pagesThe Seven Golden Rules of InvestingPravin100% (1)

- About Warren BuffetDocument14 pagesAbout Warren BuffetPadregarcia Mps100% (1)

- 100 Stocks That a Young Warren Buffett Might BuyD'Everand100 Stocks That a Young Warren Buffett Might BuyÉvaluation : 5 sur 5 étoiles5/5 (1)

- The Warren Buffett WayDocument5 pagesThe Warren Buffett Waysergiu9886Pas encore d'évaluation

- Stock Market Investing Ultimate Guide For Beginners: Warren Buffett and Benjamin Graham Intelligent Investor Strategies How to Make Money: Stock Market Investing BooksD'EverandStock Market Investing Ultimate Guide For Beginners: Warren Buffett and Benjamin Graham Intelligent Investor Strategies How to Make Money: Stock Market Investing BooksÉvaluation : 2 sur 5 étoiles2/5 (1)

- Stock Market Investing Ultimate Guide For Beginners in 2020: Warren Buffett and Benjamin Graham Intelligent Investor Strategies How to Make Money: Stock Market Investing Ultimate Guide For Beginners, #1D'EverandStock Market Investing Ultimate Guide For Beginners in 2020: Warren Buffett and Benjamin Graham Intelligent Investor Strategies How to Make Money: Stock Market Investing Ultimate Guide For Beginners, #1Évaluation : 5 sur 5 étoiles5/5 (1)

- CHAPTER 10 CASE MitulDocument2 pagesCHAPTER 10 CASE MitulISTIAK Mahmud MitulPas encore d'évaluation

- Think and invest like Warren Buffett: The manual that reveals the mindset and thinking strategies of the greatest investor of all timeD'EverandThink and invest like Warren Buffett: The manual that reveals the mindset and thinking strategies of the greatest investor of all timePas encore d'évaluation

- Trading Volatility Ny 2016Document84 pagesTrading Volatility Ny 2016sebab1Pas encore d'évaluation

- Inventory Management in Power IndustryDocument70 pagesInventory Management in Power Industryvenkatmats100% (12)

- Supreme Court rules PEACe Bonds not deposit substitutesDocument2 pagesSupreme Court rules PEACe Bonds not deposit substitutesCrisbon ApalisPas encore d'évaluation

- Actionable Summary of The Warren Buffet Way by Robert HagstromD'EverandActionable Summary of The Warren Buffet Way by Robert HagstromPas encore d'évaluation

- Simply Trading Forex. A Free Guide On How To Trade The Forex Market. Kevin Greenhall PDFDocument55 pagesSimply Trading Forex. A Free Guide On How To Trade The Forex Market. Kevin Greenhall PDFpaoloPas encore d'évaluation

- Warren Buffett Biography: Think and Grow as an Investor Billionaire: Business Strategies, Personal Life and MoreD'EverandWarren Buffett Biography: Think and Grow as an Investor Billionaire: Business Strategies, Personal Life and MoreÉvaluation : 4.5 sur 5 étoiles4.5/5 (6)

- Synopsis: Warren Buffet - Harmaein Shirlesther G. Kua FM 4-1Document6 pagesSynopsis: Warren Buffet - Harmaein Shirlesther G. Kua FM 4-1Harmaein KuaPas encore d'évaluation

- Warren Buffett's Investment Strategies Revealed in His 90th Birthday DocumentaryDocument12 pagesWarren Buffett's Investment Strategies Revealed in His 90th Birthday Documentaryyogesh patilPas encore d'évaluation

- Warren Buffett Wealth (Review and Analysis of Miles' Book)D'EverandWarren Buffett Wealth (Review and Analysis of Miles' Book)Pas encore d'évaluation

- Warren Buffett :The Life, Lessons & Principles for Success of this Investment Legend: A Comprehensive SummaryD'EverandWarren Buffett :The Life, Lessons & Principles for Success of this Investment Legend: A Comprehensive SummaryPas encore d'évaluation

- Be Like BuffettDocument3 pagesBe Like BuffettCharles GarrettPas encore d'évaluation

- Case StudyDocument6 pagesCase StudyDuy AnhPas encore d'évaluation

- Summary: Warren Buffett Invests Like a Girl: And Why You Should Too: Review and Analysis of Lofton's BookD'EverandSummary: Warren Buffett Invests Like a Girl: And Why You Should Too: Review and Analysis of Lofton's BookPas encore d'évaluation

- Chris Browne Columbia Speech 2000Document12 pagesChris Browne Columbia Speech 2000eric695Pas encore d'évaluation

- Warren Edward Buffet-1Document14 pagesWarren Edward Buffet-1Manasi PatilPas encore d'évaluation

- The Secret Billionaires' Club: Why Study Warren BuffettDocument11 pagesThe Secret Billionaires' Club: Why Study Warren BuffettRenatoPas encore d'évaluation

- Warren Edward BuffettDocument6 pagesWarren Edward BuffettUmer SheikhPas encore d'évaluation

- Warren Buffett Way PDFDocument8 pagesWarren Buffett Way PDFIsrael ZepahuaPas encore d'évaluation

- Warren Buffett's value investing philosophy and practiceDocument13 pagesWarren Buffett's value investing philosophy and practiceRoberto GonzasPas encore d'évaluation

- Explore Warren Buffett's Investment StrategiesDocument24 pagesExplore Warren Buffett's Investment StrategiesAnika Tabassum100% (1)

- Behavioral Traits of Prominent Personalities and Their Effect On Their CompanyDocument7 pagesBehavioral Traits of Prominent Personalities and Their Effect On Their CompanyAkshay K SPas encore d'évaluation

- Buffet (Rohit)Document3 pagesBuffet (Rohit)agrawalrohit_228384Pas encore d'évaluation

- 57 Ronit Ramani Tybba IrmDocument7 pages57 Ronit Ramani Tybba Irmronitramani25Pas encore d'évaluation

- Life of An EntrepreneurDocument15 pagesLife of An EntrepreneurAkshay KulkarniPas encore d'évaluation

- Individual Assignment OF Introduction To ManagementDocument11 pagesIndividual Assignment OF Introduction To ManagementNguyen Ngoc Minh Chau (K15 HL)Pas encore d'évaluation

- Warren Buffet's Approach To Business EthicsDocument4 pagesWarren Buffet's Approach To Business EthicsAmar narayanPas encore d'évaluation

- Warren Buffet BiographyDocument8 pagesWarren Buffet BiographyMark allenPas encore d'évaluation

- Cashflow ch12Document52 pagesCashflow ch12FazulAXPas encore d'évaluation

- Buffett The Making of An American Capitalist by Roger LowensteinDocument8 pagesBuffett The Making of An American Capitalist by Roger LowensteinsimasPas encore d'évaluation

- Prem Jain InterviewDocument6 pagesPrem Jain Interviewanandbajaj0Pas encore d'évaluation

- Warren BuffettDocument4 pagesWarren BuffettJawahirul MahbubiPas encore d'évaluation

- Depriciation Calculation Particulars Year 1 Year 2Document7 pagesDepriciation Calculation Particulars Year 1 Year 2venkatmatsPas encore d'évaluation

- Term4 GSTDocument30 pagesTerm4 GSTvenkatmatsPas encore d'évaluation

- RitwickGoswami (4,6)Document3 pagesRitwickGoswami (4,6)venkatmatsPas encore d'évaluation

- Siddu 1Document3 pagesSiddu 1venkatmatsPas encore d'évaluation

- PremGautham (4,0)Document2 pagesPremGautham (4,0)venkatmatsPas encore d'évaluation

- Krishnan SirDocument4 pagesKrishnan SirvenkatmatsPas encore d'évaluation

- ManasGoswami (4,3)Document3 pagesManasGoswami (4,3)venkatmatsPas encore d'évaluation

- Riddhi Dutta: Senior Opportunity Business AnalystDocument4 pagesRiddhi Dutta: Senior Opportunity Business AnalystvenkatmatsPas encore d'évaluation

- Income Tax PPT 120114083854 Phpapp01Document155 pagesIncome Tax PPT 120114083854 Phpapp01Prâtèék ShâhPas encore d'évaluation

- KunalNagpal (4,0)Document3 pagesKunalNagpal (4,0)venkatmatsPas encore d'évaluation

- IndranilChatterjee (4,0)Document3 pagesIndranilChatterjee (4,0)venkatmatsPas encore d'évaluation

- Karthikarjun (0,3)Document2 pagesKarthikarjun (0,3)venkatmatsPas encore d'évaluation

- DeepikaMendiratta (0,6)Document2 pagesDeepikaMendiratta (0,6)venkatmatsPas encore d'évaluation

- B.tax+Case StudiesDocument19 pagesB.tax+Case StudiesvenkatmatsPas encore d'évaluation

- Particulars Oty Rate AmountDocument6 pagesParticulars Oty Rate AmountvenkatmatsPas encore d'évaluation

- Cash Flow Analysis: (Wavell Corporation) Year 1 2 3 4Document3 pagesCash Flow Analysis: (Wavell Corporation) Year 1 2 3 4venkatmatsPas encore d'évaluation

- Ashok LeylandDocument12 pagesAshok LeylandvenkatmatsPas encore d'évaluation

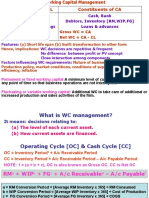

- Working Capital ManagementDocument10 pagesWorking Capital ManagementvenkatmatsPas encore d'évaluation

- Inventory ManagementDocument3 pagesInventory ManagementvenkatmatsPas encore d'évaluation

- Capital BudgetingDocument7 pagesCapital BudgetingvenkatmatsPas encore d'évaluation

- Gurvinder Brar - Text MiningDocument28 pagesGurvinder Brar - Text Miningxy053333Pas encore d'évaluation

- 2,3,4 Ir Uzd PDFDocument31 pages2,3,4 Ir Uzd PDFLeonid LeoPas encore d'évaluation

- Changes in Equity, Cash Flows, NotesDocument3 pagesChanges in Equity, Cash Flows, NotesLucas BantilingPas encore d'évaluation

- INVESTMENTS-HO-5-SOL-GUIDE-PP-1-2 EditedDocument1 pageINVESTMENTS-HO-5-SOL-GUIDE-PP-1-2 EditedKendrew SujidePas encore d'évaluation

- Three (3) Major Decisions The Finance Manager Would TakeDocument11 pagesThree (3) Major Decisions The Finance Manager Would TakeJohn Verlie EMpsPas encore d'évaluation

- SBI Mutual Fund Report on Portfolio Management and AnalysisDocument50 pagesSBI Mutual Fund Report on Portfolio Management and AnalysisShivaji Rao Karthik VagmorePas encore d'évaluation

- Cost of CapitalDocument15 pagesCost of CapitalShainaPas encore d'évaluation

- Management Accounting Level 3: LCCI International QualificationsDocument14 pagesManagement Accounting Level 3: LCCI International QualificationsHein Linn Kyaw50% (2)

- Solar Panel Stock Analysis and ValuationDocument10 pagesSolar Panel Stock Analysis and ValuationAkuw AjahPas encore d'évaluation

- Revised Syllabus for Economics PapersDocument34 pagesRevised Syllabus for Economics PapersRUPESH SHIDPas encore d'évaluation

- MBAB 5P01 - Chapter 1Document3 pagesMBAB 5P01 - Chapter 1Priya MehtaPas encore d'évaluation

- The Deal Private Credit's '24 Tech ResolutionsDocument7 pagesThe Deal Private Credit's '24 Tech Resolutionsshelby.wintersPas encore d'évaluation

- S&P500 Handbook SheetDocument2 pagesS&P500 Handbook SheetRavi Swaminathan0% (1)

- Chapter 7Document13 pagesChapter 7lov3m3Pas encore d'évaluation

- ACC 102.Exercise1.Inventory Cost Flow and LCNRVDocument5 pagesACC 102.Exercise1.Inventory Cost Flow and LCNRVMa. Lou Erika BALITEPas encore d'évaluation

- Reduce Agency Costs in Corporate Governance with Proper IncentivesDocument20 pagesReduce Agency Costs in Corporate Governance with Proper IncentivesCamella CandonPas encore d'évaluation

- Depreciation MethodsDocument21 pagesDepreciation MethodsPawan PoynauthPas encore d'évaluation

- Tax Principles Broad Basing Simplicity EfficiencyDocument8 pagesTax Principles Broad Basing Simplicity EfficiencyPrithvi PrasadPas encore d'évaluation

- Project TopicsDocument2 pagesProject TopicsAkhil SaiPas encore d'évaluation

- Portfolio Management - Chapter 13Document39 pagesPortfolio Management - Chapter 13Dr Rushen SinghPas encore d'évaluation

- Operation Costing, Just-In-Time System, and Backflush CostingDocument15 pagesOperation Costing, Just-In-Time System, and Backflush CostingJeremy Cyrus TrinidadPas encore d'évaluation

- Financial Accounting-I Sem-1 (GU-DEC-2014)Document12 pagesFinancial Accounting-I Sem-1 (GU-DEC-2014)Ekta RanaPas encore d'évaluation

- PR Academy Financial Ratio Analysis GuideDocument22 pagesPR Academy Financial Ratio Analysis GuideMadesh KuppuswamyPas encore d'évaluation

- Chapter 5 Implementation Search Through ClosingDocument23 pagesChapter 5 Implementation Search Through ClosingMeshaFrisnaYozaPas encore d'évaluation

- SSRN Id4220449Document51 pagesSSRN Id4220449pnjohn2822Pas encore d'évaluation