Vous aimerez peut-être aussi

- Mega Project Assurance: Volume One - The Terminological DictionaryD'EverandMega Project Assurance: Volume One - The Terminological DictionaryPas encore d'évaluation

- Liabilities - Debt RestructuringDocument4 pagesLiabilities - Debt RestructuringChinchin Ilagan DatayloPas encore d'évaluation

- ACTGIA2 - CH01 2 3 4 - Liabilities Etc.Document44 pagesACTGIA2 - CH01 2 3 4 - Liabilities Etc.chingPas encore d'évaluation

- PAS 19 Employee Benefits: Short-Term Employee Benefits Are Employee Benefits (Other Than Termination BenDocument5 pagesPAS 19 Employee Benefits: Short-Term Employee Benefits Are Employee Benefits (Other Than Termination BenKaila Clarisse CortezPas encore d'évaluation

- NC Concept MapDocument3 pagesNC Concept MapMitch MindanaoPas encore d'évaluation

- Liability and ProvisionDocument45 pagesLiability and ProvisionDenise RoquePas encore d'évaluation

- Probiotec Annual Report 2021 6Document8 pagesProbiotec Annual Report 2021 6楊敬宇Pas encore d'évaluation

- Aud Prob Part 1Document106 pagesAud Prob Part 1Ma. Hazel Donita DiazPas encore d'évaluation

- Megaworld Corporation: Liabilities and Equity 2010 2009 2008Document9 pagesMegaworld Corporation: Liabilities and Equity 2010 2009 2008Owdray CiaPas encore d'évaluation

- Restricted Cash - GAAP and IFRSDocument49 pagesRestricted Cash - GAAP and IFRSTai D GiangPas encore d'évaluation

- Probiotec Annual Report 2022 6Document8 pagesProbiotec Annual Report 2022 6楊敬宇Pas encore d'évaluation

- SBR - Chapter 5Document6 pagesSBR - Chapter 5Jason KumarPas encore d'évaluation

- Employer Benefit - Part 2Document9 pagesEmployer Benefit - Part 2Julian Adam PagalPas encore d'évaluation

- Chapter 1 Liabilities PDFDocument9 pagesChapter 1 Liabilities PDFKesiah FortunaPas encore d'évaluation

- ACCT 10001 Accounting Reports & Analysis Review Questions - Topic 4 Chapter 5: Balance Sheet-Liabilities & EquityDocument7 pagesACCT 10001 Accounting Reports & Analysis Review Questions - Topic 4 Chapter 5: Balance Sheet-Liabilities & EquityBáchHợpPas encore d'évaluation

- Chapter 6 Employee Benefits (Part 2)Document21 pagesChapter 6 Employee Benefits (Part 2)not funny didn't laughPas encore d'évaluation

- Leases Course NotesDocument14 pagesLeases Course NotescatalineuuPas encore d'évaluation

- Chapter 03 - Analyzing Financing ActivitiDocument72 pagesChapter 03 - Analyzing Financing ActivitiMuhammad HamzaPas encore d'évaluation

- Employee BenefitsDocument9 pagesEmployee BenefitstinydmpPas encore d'évaluation

- FARAP-4413 (Post-Employment Benefits)Document5 pagesFARAP-4413 (Post-Employment Benefits)Dizon Ropalito P.Pas encore d'évaluation

- Post Employment BenefitsDocument31 pagesPost Employment BenefitsSky SoronoiPas encore d'évaluation

- Module 7 - Notes Payable & Debt RestructuringDocument4 pagesModule 7 - Notes Payable & Debt RestructuringLuiPas encore d'évaluation

- Note FinantionalDocument4 pagesNote FinantionalhvhvmPas encore d'évaluation

- Accounting Standard 16: Borrowing Costs This StandardDocument3 pagesAccounting Standard 16: Borrowing Costs This StandardborsutkarPas encore d'évaluation

- Analysis of Finanacing ActivitiesDocument48 pagesAnalysis of Finanacing ActivitiesPrateek SinglaPas encore d'évaluation

- Ia 2 - ReviewerDocument3 pagesIa 2 - ReviewerCenelyn PajarillaPas encore d'évaluation

- Week 9 - Analysis of Financing Liabilities & Off-Balance Sheet DebtDocument13 pagesWeek 9 - Analysis of Financing Liabilities & Off-Balance Sheet DebtJarida La UongoPas encore d'évaluation

- Module 4 COMPONENTS OF FINANCIAL STATEMENTS PDFDocument15 pagesModule 4 COMPONENTS OF FINANCIAL STATEMENTS PDFErmelyn GayoPas encore d'évaluation

- IAS 37 Provisions PoliticaDocument9 pagesIAS 37 Provisions PoliticaCandySlimePas encore d'évaluation

- Ias 19 Employee BenefitsDocument43 pagesIas 19 Employee BenefitsHasan Ali BokhariPas encore d'évaluation

- Ias 19Document59 pagesIas 19Leonardo BritoPas encore d'évaluation

- Pas 19,20,21Document53 pagesPas 19,20,21ssamporna19157Pas encore d'évaluation

- Learning Material 1Document7 pagesLearning Material 1salduaerossjacobPas encore d'évaluation

- Employee BenefitsDocument9 pagesEmployee BenefitstinydmpPas encore d'évaluation

- CH - 03financial Statement Analysis Solution Manual CH - 03Document63 pagesCH - 03financial Statement Analysis Solution Manual CH - 03OktarinaPas encore d'évaluation

- Chapter 4 - Accounting For Other Liabilities: A. Post Employment BenefitsDocument50 pagesChapter 4 - Accounting For Other Liabilities: A. Post Employment BenefitsLovely AbadianoPas encore d'évaluation

- Provisions, Contingent Liabilities and Contingent AssetsDocument36 pagesProvisions, Contingent Liabilities and Contingent Assetspks009Pas encore d'évaluation

- Financial Staements Duly Authenticated As Per Section 134 (Including Boards Report, Auditors Report and Other Documents) - 29102023Document28 pagesFinancial Staements Duly Authenticated As Per Section 134 (Including Boards Report, Auditors Report and Other Documents) - 29102023mnbvcxzqwerPas encore d'évaluation

- Liabilities by Valix: Intermediate Accounting 2Document34 pagesLiabilities by Valix: Intermediate Accounting 2Trisha Mae AlburoPas encore d'évaluation

- Intermediate Accounting 2: LiabilitiesDocument17 pagesIntermediate Accounting 2: LiabilitiesAngel MilanPas encore d'évaluation

- Module 1-LIABILITIES and PREMIUM LIABILITYDocument10 pagesModule 1-LIABILITIES and PREMIUM LIABILITYKathleen SalesPas encore d'évaluation

- Module 001 Accounting For Liabilities-Current Part 1Document6 pagesModule 001 Accounting For Liabilities-Current Part 1Gab BautroPas encore d'évaluation

- MASB Standard 29 Employee Benefits: Malaysian Accounting Standards BoardDocument78 pagesMASB Standard 29 Employee Benefits: Malaysian Accounting Standards BoardSTUDYBIZPas encore d'évaluation

- Intermediate Acctg Lecture On Liabilities 22Document3 pagesIntermediate Acctg Lecture On Liabilities 22Tracy Lyn Macasieb NavidadPas encore d'évaluation

- Accounting Standard 16Document7 pagesAccounting Standard 16Gaurav JadhavPas encore d'évaluation

- Chapter 6 Emplooyee Benefit Part 2Document8 pagesChapter 6 Emplooyee Benefit Part 2maria isabellaPas encore d'évaluation

- Pugosa Final 581-600 Audtg. 1 Adv Part 2 BookDocument20 pagesPugosa Final 581-600 Audtg. 1 Adv Part 2 BookPorferia PugosaPas encore d'évaluation

- Chapter One: Current Liabilities, Provisions, and Contingencies The Nature, Type and Valuation of Current LiabilitiesDocument12 pagesChapter One: Current Liabilities, Provisions, and Contingencies The Nature, Type and Valuation of Current LiabilitiesJuan KermaPas encore d'évaluation

- IND AS NotesDocument3 pagesIND AS NotesKhushi SoniPas encore d'évaluation

- Accounting For Employment BenefitsDocument5 pagesAccounting For Employment BenefitsiamacrusaderPas encore d'évaluation

- SM ch10Document67 pagesSM ch10Rendy KurniawanPas encore d'évaluation

- IAS 19 Employee BenefitsDocument22 pagesIAS 19 Employee Benefitsanon_419651076Pas encore d'évaluation

- LOB 10 ReviewerDocument5 pagesLOB 10 ReviewernmabaningPas encore d'évaluation

- Module 13 PAS 37Document6 pagesModule 13 PAS 37Jan JanPas encore d'évaluation

- Accounts ReceivableDocument3 pagesAccounts ReceivableJin Ian VincentPas encore d'évaluation

- Loan Loss ProvisionDocument6 pagesLoan Loss Provisiontanim7Pas encore d'évaluation

- Writing Up A Case StudyDocument3 pagesWriting Up A Case StudyalliahnahPas encore d'évaluation

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingD'EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingPas encore d'évaluation

- The Handbook for Reading and Preparing Proxy Statements: A Guide to the SEC Disclosure Rules for Executive and Director Compensation, 6th EditionD'EverandThe Handbook for Reading and Preparing Proxy Statements: A Guide to the SEC Disclosure Rules for Executive and Director Compensation, 6th EditionPas encore d'évaluation

- Account Name K1 K2 A1 A2 A5 F1 F2 F3 B5 B 3 N Total Cs. Payment Utang ProfitDocument2 pagesAccount Name K1 K2 A1 A2 A5 F1 F2 F3 B5 B 3 N Total Cs. Payment Utang ProfitJudith CastroPas encore d'évaluation

- Branches of GovernmentDocument1 pageBranches of GovernmentJudith CastroPas encore d'évaluation

- Sample Moa 3 19 14Document3 pagesSample Moa 3 19 14Judith CastroPas encore d'évaluation

- 5.takeover GGSRDocument9 pages5.takeover GGSRJudith CastroPas encore d'évaluation

- 2.agency Problem Principal-AgentDocument6 pages2.agency Problem Principal-AgentJudith Castro100% (1)

- Ojt Performance Evaluation Form: General Impressions and Observations of The TraineeDocument1 pageOjt Performance Evaluation Form: General Impressions and Observations of The TraineeJudith CastroPas encore d'évaluation

- Pages 891027Document9 pagesPages 891027Judith CastroPas encore d'évaluation

- AFS 2016 - Towncall Rural Bank, Inc. Page 28 of 42Document3 pagesAFS 2016 - Towncall Rural Bank, Inc. Page 28 of 42Judith CastroPas encore d'évaluation

- Financial Assets Recognized in Balance SheetsDocument2 pagesFinancial Assets Recognized in Balance SheetsJudith CastroPas encore d'évaluation

- GGSR Question Chapter 5 DoxDocument3 pagesGGSR Question Chapter 5 DoxJudith CastroPas encore d'évaluation

- Towncall Rural Bank, Inc.: To Adjust Retirement Fund Based On Retirement Benefit Obligation BalanceDocument1 pageTowncall Rural Bank, Inc.: To Adjust Retirement Fund Based On Retirement Benefit Obligation BalanceJudith CastroPas encore d'évaluation

- Voidable Contract1.Docx CompleteDocument3 pagesVoidable Contract1.Docx CompleteJudith CastroPas encore d'évaluation

- AFS 2016 - Towncall Rural Bank, Inc. Page 28 of 42Document3 pagesAFS 2016 - Towncall Rural Bank, Inc. Page 28 of 42Judith CastroPas encore d'évaluation

- Voidable Contract1.Docx CompleteDocument3 pagesVoidable Contract1.Docx CompleteJudith CastroPas encore d'évaluation

- Accounting For LeaseDocument75 pagesAccounting For LeaseKenncy33% (3)

- Quiz No. 06: Financial InstrumentsDocument2 pagesQuiz No. 06: Financial InstrumentsPHI NGUYEN HOANGPas encore d'évaluation

- Long Term: Notes ReceivableDocument17 pagesLong Term: Notes Receivablekrisha milloPas encore d'évaluation

- Chart of Accounts: Appendix UDocument3 pagesChart of Accounts: Appendix UThea LicupPas encore d'évaluation

- Topic 6 - ACCA Cash Flow Q SDocument8 pagesTopic 6 - ACCA Cash Flow Q SGeorge Wang100% (1)

- ReceivablesDocument20 pagesReceivablesGemmalyn FolguerasPas encore d'évaluation

- FS (3 Years) : A. Income StatementDocument10 pagesFS (3 Years) : A. Income StatementchiahwalousettePas encore d'évaluation

- Module 2d Loan ReceivableDocument24 pagesModule 2d Loan ReceivableChen HaoPas encore d'évaluation

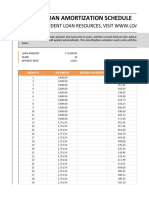

- Excel Student Loan Amortization TableDocument18 pagesExcel Student Loan Amortization TableIsmail UsmanPas encore d'évaluation

- Muh - Syukur (A031191077) Akuntansi Keuangan - Exercise E.12.9Document3 pagesMuh - Syukur (A031191077) Akuntansi Keuangan - Exercise E.12.9RismayantiPas encore d'évaluation

- Expedia JPM InitiationDocument26 pagesExpedia JPM Initiationexaltedangel09Pas encore d'évaluation

- Beiersdorf AG 2019 Annual Financial Statements PDFDocument40 pagesBeiersdorf AG 2019 Annual Financial Statements PDFPotato ChanPas encore d'évaluation

- RJR Nabisco - SpreadsheetDocument10 pagesRJR Nabisco - SpreadsheetSurajPas encore d'évaluation

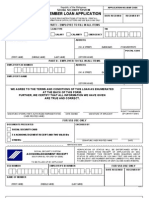

- SSS Member Loan Application FormDocument2 pagesSSS Member Loan Application FormJr Sam90% (49)

- Intermediate Accounting: Arlyn C. Pasion Prelim Bsa 2Document19 pagesIntermediate Accounting: Arlyn C. Pasion Prelim Bsa 2Marvin OrdinesPas encore d'évaluation

- 1907 Notes Receivable and Loan ImpairmentDocument4 pages1907 Notes Receivable and Loan ImpairmentCykee Hanna Quizo Lumongsod100% (2)

- Auditing Problem SolutionsDocument13 pagesAuditing Problem SolutionsjhobsPas encore d'évaluation

- Financial Mathematics Lecture Notes Fina PDFDocument71 pagesFinancial Mathematics Lecture Notes Fina PDFTram HoPas encore d'évaluation

- 1911 Investments Investment in Associate and Bond InvestmentDocument13 pages1911 Investments Investment in Associate and Bond InvestmentCykee Hanna Quizo LumongsodPas encore d'évaluation

- CH 11 Lessee Accounting - Other IssuesDocument4 pagesCH 11 Lessee Accounting - Other IssuesGenebabe LoquiasPas encore d'évaluation

- 2.1. Finance & Financial Statement Analysis by CA Pramod JainDocument69 pages2.1. Finance & Financial Statement Analysis by CA Pramod JainAnjaneyulu SadhuPas encore d'évaluation

- IBIG 06 01 Three Statements 30 Minutes CompleteDocument5 pagesIBIG 06 01 Three Statements 30 Minutes CompletenisPas encore d'évaluation

- IAS#38Document43 pagesIAS#38Shah KamalPas encore d'évaluation

- Albania Chart of Accounts For DCs 2007 W0866907Document33 pagesAlbania Chart of Accounts For DCs 2007 W0866907Koleksi Buku BekasPas encore d'évaluation

- Q1 2011 Return On Tangible Capital PDFDocument1 pageQ1 2011 Return On Tangible Capital PDFVenkat Sai Kumar KothalaPas encore d'évaluation

- Bus Math Grade 11 q2 m2 w2Document7 pagesBus Math Grade 11 q2 m2 w2Ronald AlmagroPas encore d'évaluation

- Attachments - Rainbow RowellDocument29 pagesAttachments - Rainbow RowellAlvin Yerc0% (1)

- Problem 7 Bonds Payable - Straight Line Method Journal Entries Date Account Title & ExplanationDocument15 pagesProblem 7 Bonds Payable - Straight Line Method Journal Entries Date Account Title & ExplanationLovely Anne Dela CruzPas encore d'évaluation

- Chapter 12 PAS 38 INTANGIBLE ASSETSDocument4 pagesChapter 12 PAS 38 INTANGIBLE ASSETSJeanette LampitocPas encore d'évaluation

- Atlassian Roadshow Pitch Deck Draft - November 2015 - COMPLETE DECK - FINALDocument48 pagesAtlassian Roadshow Pitch Deck Draft - November 2015 - COMPLETE DECK - FINALTechCrunch100% (1)