Vous aimerez peut-être aussi

- Summary of Anthony Crescenzi's The Strategic Bond Investor, Third EditionD'EverandSummary of Anthony Crescenzi's The Strategic Bond Investor, Third EditionPas encore d'évaluation

- Reform The International Monetary SystemDocument3 pagesReform The International Monetary SystemMarcel CasellaPas encore d'évaluation

- International Monetary FundDocument5 pagesInternational Monetary FundAastha sharmaPas encore d'évaluation

- 4.B IMF Lending and ConditionalityDocument12 pages4.B IMF Lending and Conditionalityarian.sajjadi7Pas encore d'évaluation

- Pension Funds and Domestic Debt Markets in Emerging EconomiesDocument22 pagesPension Funds and Domestic Debt Markets in Emerging EconomiesGabriel DAnnunzioPas encore d'évaluation

- Transformation of Developing Economy Debt Under Financial Capital: Effects of Financial Growth On Developing Economies Since The 1970sDocument15 pagesTransformation of Developing Economy Debt Under Financial Capital: Effects of Financial Growth On Developing Economies Since The 1970sSaumil SharmaPas encore d'évaluation

- Managing Financial Crises in Emerging Markets: Barry Eichengreen Richard PortesDocument34 pagesManaging Financial Crises in Emerging Markets: Barry Eichengreen Richard PortesBruno Ramirez RevoredoPas encore d'évaluation

- Epr 2022 Fima-Repo ChoiDocument22 pagesEpr 2022 Fima-Repo ChoiKelvin MishoshoPas encore d'évaluation

- Chapter 13Document3 pagesChapter 13Hazell DPas encore d'évaluation

- Pakistan Approaches IMF PDFDocument3 pagesPakistan Approaches IMF PDFsalmanyz6Pas encore d'évaluation

- Articel 1 Regina ElisabethDocument89 pagesArticel 1 Regina ElisabethIMELDA YUNI BUTAR BUTAR 2204010030Pas encore d'évaluation

- The Debt CrisisDocument3 pagesThe Debt CrisismestrumPas encore d'évaluation

- Life After Debt - Debtless by 2012, The U.S and The World Without US Treasury Bonds (FOIA Document)Document43 pagesLife After Debt - Debtless by 2012, The U.S and The World Without US Treasury Bonds (FOIA Document)Ephraim DavisPas encore d'évaluation

- Monetary Policy.: Economic Money Credit InterestDocument27 pagesMonetary Policy.: Economic Money Credit Interestchemy_87Pas encore d'évaluation

- Eco International Monetary FundDocument34 pagesEco International Monetary FundAbbasPas encore d'évaluation

- Assignment 4 Subprime Mortgage Crisis 2008: Case BackgroundDocument6 pagesAssignment 4 Subprime Mortgage Crisis 2008: Case BackgroundShrey ChaudharyPas encore d'évaluation

- 1.international Financial InstitutionsDocument9 pages1.international Financial Institutionswaseem20062007_35082Pas encore d'évaluation

- International Financial InstitutionsDocument9 pagesInternational Financial InstitutionsgzalyPas encore d'évaluation

- ESAPDocument8 pagesESAPsimbarashe chitsaPas encore d'évaluation

- The Structure and Functions of The Federal Reserve System: Policy, Banking Supervision, Financial ServicesDocument18 pagesThe Structure and Functions of The Federal Reserve System: Policy, Banking Supervision, Financial ServicesJapish MehtaPas encore d'évaluation

- IMF Con 2011Document26 pagesIMF Con 2011anashussainPas encore d'évaluation

- Case Study Solution: Future of World Bank and IMFDocument5 pagesCase Study Solution: Future of World Bank and IMFJithu Jose ParackalPas encore d'évaluation

- SETHUDocument12 pagesSETHUMadhavi M KatakiaPas encore d'évaluation

- Global Money Notes #14: The Safe Asset GlutDocument16 pagesGlobal Money Notes #14: The Safe Asset GlutPhilippe100% (1)

- For Release On Delivery 10:00 A.M. ESTDocument12 pagesFor Release On Delivery 10:00 A.M. ESTZerohedgePas encore d'évaluation

- Financial Markets (Chapter 6)Document2 pagesFinancial Markets (Chapter 6)Kyla DayawonPas encore d'évaluation

- Fitch Rating MethodologyDocument16 pagesFitch Rating Methodologyrash2014Pas encore d'évaluation

- A More Focused IMF: Eeches and PapersDocument6 pagesA More Focused IMF: Eeches and PapersJitesh MaheshwariPas encore d'évaluation

- Exchange Rate and Capital Account Management For Developing CountriesDocument10 pagesExchange Rate and Capital Account Management For Developing CountriesJace BezzitPas encore d'évaluation

- Chapter 7: International Banking and Money MarketDocument2 pagesChapter 7: International Banking and Money MarketVeeranjaneyulu KacherlaPas encore d'évaluation

- Standards For Crisis PreventionDocument17 pagesStandards For Crisis Preventionanon_767585351Pas encore d'évaluation

- Stepping Up Crisis LendingDocument2 pagesStepping Up Crisis Lendingjasswin2Pas encore d'évaluation

- Independence? Discuss at Least Two Cases Which Contributed To The Bankruptcy of The Old Central Bank ofDocument3 pagesIndependence? Discuss at Least Two Cases Which Contributed To The Bankruptcy of The Old Central Bank ofHazel Gayle De PerioPas encore d'évaluation

- ch03Document4 pagesch03simonrosariojohnpeterPas encore d'évaluation

- Economic Outlook Emerging Mkts Oct 2013 FINALDocument6 pagesEconomic Outlook Emerging Mkts Oct 2013 FINALkunalwarwickPas encore d'évaluation

- Global Liquidity and International RiskDocument3 pagesGlobal Liquidity and International RiskGurinder singhPas encore d'évaluation

- Finanzas Internacionales: Ejercicios de La Tarea 5Document10 pagesFinanzas Internacionales: Ejercicios de La Tarea 5gerardoPas encore d'évaluation

- The Bond Market in GhanaDocument12 pagesThe Bond Market in GhanaJohn Kennedy Akotia100% (3)

- Regulation of Financial Markets Take Home ExamDocument22 pagesRegulation of Financial Markets Take Home ExamBrandon TeePas encore d'évaluation

- Project Report On Internatinal Monetary FundDocument60 pagesProject Report On Internatinal Monetary FundRiSHI KeSH GawaIPas encore d'évaluation

- World Bank and ImfDocument14 pagesWorld Bank and ImfSaket ShaharePas encore d'évaluation

- Global Money Notes #18Document14 pagesGlobal Money Notes #18lerhlerh100% (1)

- IMF and WTODocument28 pagesIMF and WTOFahmiatul JannatPas encore d'évaluation

- Empowering The IMF: Should Reform Be A Requirement For Increasing The Fund's Resources?Document26 pagesEmpowering The IMF: Should Reform Be A Requirement For Increasing The Fund's Resources?Center for Economic and Policy Research100% (9)

- Global Money Notes #21Document9 pagesGlobal Money Notes #21shortmycds75% (4)

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamPas encore d'évaluation

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamPas encore d'évaluation

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamPas encore d'évaluation

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamPas encore d'évaluation

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamPas encore d'évaluation

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamPas encore d'évaluation

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamPas encore d'évaluation

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamPas encore d'évaluation

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamPas encore d'évaluation

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamPas encore d'évaluation

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamPas encore d'évaluation

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamPas encore d'évaluation

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamPas encore d'évaluation

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamPas encore d'évaluation

- Pengaruh Torefaksi Terhadap Sifat Kimia Pelet TandDocument8 pagesPengaruh Torefaksi Terhadap Sifat Kimia Pelet TandkongbengPas encore d'évaluation

- K 112Document2 pagesK 112kongbengPas encore d'évaluation

- Destination: Innovation For YourDocument4 pagesDestination: Innovation For YourkongbengPas encore d'évaluation

- He Usantara Anifesto: #L U C CDocument40 pagesHe Usantara Anifesto: #L U C CWan Hadi Wan ZainalPas encore d'évaluation

- Employment AgreementDocument9 pagesEmployment AgreementkongbengPas encore d'évaluation

- LOIDocument1 pageLOIVinci PoncardasPas encore d'évaluation

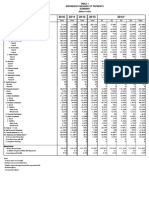

- Items 2010 2011 2012 2013 2014 : (Millions of USD)Document12 pagesItems 2010 2011 2012 2013 2014 : (Millions of USD)kongbengPas encore d'évaluation

- CFPB Sample Revocation Letter To Your Bank or Credit UnionDocument2 pagesCFPB Sample Revocation Letter To Your Bank or Credit UnionkongbengPas encore d'évaluation

- YC Form SaaS AgreementDocument10 pagesYC Form SaaS AgreementYan BaglieriPas encore d'évaluation

- Avtest Summary Homeuser 2017-06Document18 pagesAvtest Summary Homeuser 2017-06kongbengPas encore d'évaluation

- Negative Net Resource Transfers As A Minskyian Hedge Profile and The Stability of The International Financial SystemDocument13 pagesNegative Net Resource Transfers As A Minskyian Hedge Profile and The Stability of The International Financial SystemkongbengPas encore d'évaluation

- Press Release Saratoga 9M2015Document3 pagesPress Release Saratoga 9M2015kongbengPas encore d'évaluation

- Notice of Payment: Court DetailsDocument1 pageNotice of Payment: Court DetailskongbengPas encore d'évaluation

- Appendix 7 Pa ContractDocument5 pagesAppendix 7 Pa ContractkongbengPas encore d'évaluation

- End User CertificateDocument2 pagesEnd User CertificatekongbengPas encore d'évaluation

- Porsche DownloadDocument14 pagesPorsche DownloadkongbengPas encore d'évaluation

- CFPB Sample Revocation Letter To Your Bank or Credit UnionDocument2 pagesCFPB Sample Revocation Letter To Your Bank or Credit UnionkongbengPas encore d'évaluation

- From TO Asat (: Balance Sheet Information Profit & Loss InformationDocument1 pageFrom TO Asat (: Balance Sheet Information Profit & Loss InformationkongbengPas encore d'évaluation

- Sample Org ContractDocument3 pagesSample Org ContractEmma FarcasPas encore d'évaluation

- Template BulletDocument1 pageTemplate BulletccllPas encore d'évaluation

- Company Profile - Apple - Q4 2012Document2 pagesCompany Profile - Apple - Q4 2012kongbengPas encore d'évaluation

- Export Negotiation Collection Schedule-2015Document1 pageExport Negotiation Collection Schedule-2015kongbengPas encore d'évaluation

- Airbus Gcs EbsDocument5 pagesAirbus Gcs EbskongbengPas encore d'évaluation

- Conger - Necessary Art of Persuasion PDFDocument12 pagesConger - Necessary Art of Persuasion PDFkongbengPas encore d'évaluation

- Compass Repeater Price Sheet GA4 0912Document2 pagesCompass Repeater Price Sheet GA4 0912kongbengPas encore d'évaluation

- Press Release Saratoga 9M2015Document3 pagesPress Release Saratoga 9M2015kongbengPas encore d'évaluation

- AT572Document3 pagesAT572kongbengPas encore d'évaluation

- OneCare Global Extended Warranty Pricesheet 0117Document1 pageOneCare Global Extended Warranty Pricesheet 0117kongbengPas encore d'évaluation

- H184a S15Document4 pagesH184a S15kongbengPas encore d'évaluation

- Porsche DownloadDocument14 pagesPorsche DownloadkongbengPas encore d'évaluation

- Influence of Freezing and Pasteurization of The Physical Condition of The Plastik (PE, PP and HDPE) As Selar Fish Packaging (Selaroides Leptolepis) in Sendang Biru, Malang, East Java. IndonesiaDocument7 pagesInfluence of Freezing and Pasteurization of The Physical Condition of The Plastik (PE, PP and HDPE) As Selar Fish Packaging (Selaroides Leptolepis) in Sendang Biru, Malang, East Java. IndonesiaInternational Network For Natural SciencesPas encore d'évaluation

- Routine Maintenance For External Water Tank Pump and Circulation Pump On FID Tower and Rack 2017-014Document5 pagesRoutine Maintenance For External Water Tank Pump and Circulation Pump On FID Tower and Rack 2017-014CONVIERTE PDF JPG WORDPas encore d'évaluation

- Characteristics of Trochoids and Their Application To Determining Gear Teeth Fillet ShapesDocument14 pagesCharacteristics of Trochoids and Their Application To Determining Gear Teeth Fillet ShapesJohn FelemegkasPas encore d'évaluation

- MPPSC ACF Test Paper 8 (26 - 06 - 2022)Document6 pagesMPPSC ACF Test Paper 8 (26 - 06 - 2022)Hari Harul VullangiPas encore d'évaluation

- PC Engines APU2 Series System BoardDocument11 pagesPC Engines APU2 Series System Boardpdy2Pas encore d'évaluation

- E-Waste: Name: Nishant.V.Naik Class: F.Y.Btech (Civil) Div: VII SR - No: 18 Roll No: A050136Document11 pagesE-Waste: Name: Nishant.V.Naik Class: F.Y.Btech (Civil) Div: VII SR - No: 18 Roll No: A050136Nishant NaikPas encore d'évaluation

- PP Checklist (From IB)Document2 pagesPP Checklist (From IB)Pete GoodmanPas encore d'évaluation

- 4D Beijing (Muslim) CHINA MATTA Fair PackageDocument1 page4D Beijing (Muslim) CHINA MATTA Fair PackageSedunia TravelPas encore d'évaluation

- Die Openbare BeskermerDocument3 pagesDie Openbare BeskermerJaco BesterPas encore d'évaluation

- Weekly Lesson Plan: Pry 3 (8years) Third Term Week 1Document12 pagesWeekly Lesson Plan: Pry 3 (8years) Third Term Week 1Kunbi Santos-ArinzePas encore d'évaluation

- 5G NR Essentials Guide From IntelefyDocument15 pages5G NR Essentials Guide From IntelefyUzair KhanPas encore d'évaluation

- (Kazantzakis Nikos) Freedom or DeathDocument195 pages(Kazantzakis Nikos) Freedom or DeathTarlan FisherPas encore d'évaluation

- 1 s2.0 S2238785423001345 MainDocument10 pages1 s2.0 S2238785423001345 MainHamada Shoukry MohammedPas encore d'évaluation

- IEEE 802 StandardsDocument14 pagesIEEE 802 StandardsHoney RamosPas encore d'évaluation

- GladioDocument28 pagesGladioPedro Navarro SeguraPas encore d'évaluation

- Presentación de Power Point Sobre Aspectos de La Cultura Inglesa Que Han Influido en El Desarrollo de La HumanidadDocument14 pagesPresentación de Power Point Sobre Aspectos de La Cultura Inglesa Que Han Influido en El Desarrollo de La HumanidadAndres EduardoPas encore d'évaluation

- Subject: PSCP (15-10-19) : Syllabus ContentDocument4 pagesSubject: PSCP (15-10-19) : Syllabus ContentNikunjBhattPas encore d'évaluation

- Schermer 1984Document25 pagesSchermer 1984Pedro VeraPas encore d'évaluation

- Patricio Gerpe ResumeDocument2 pagesPatricio Gerpe ResumeAnonymous 3ID4TBPas encore d'évaluation

- Analysis of MMDR Amendment ActDocument5 pagesAnalysis of MMDR Amendment ActArunabh BhattacharyaPas encore d'évaluation

- Ocr A Level History Russia CourseworkDocument7 pagesOcr A Level History Russia Courseworkbcrqhr1n100% (1)

- Albert-Einstein-Strasse 42a, D-63322 Roedermark, Germany Tel.: 0049 (0) 6074-7286503 - Fax: 0049 (0) 6074-7286504Document19 pagesAlbert-Einstein-Strasse 42a, D-63322 Roedermark, Germany Tel.: 0049 (0) 6074-7286503 - Fax: 0049 (0) 6074-7286504Ilias Asimakis100% (1)

- Reflective Memo 1-PracticumDocument5 pagesReflective Memo 1-Practicumapi-400515862Pas encore d'évaluation

- Engine Stalls at Low RPM: Diagnostic CodesDocument3 pagesEngine Stalls at Low RPM: Diagnostic CodesAmir Bambang YudhoyonoPas encore d'évaluation

- Genie PDFDocument277 pagesGenie PDFOscar ItzolPas encore d'évaluation

- Evolution of Campus Switching: Marketing Presentation Marketing PresentationDocument35 pagesEvolution of Campus Switching: Marketing Presentation Marketing PresentationRosal Mark JovenPas encore d'évaluation

- Poka-Yoke or Mistake Proofing: Historical Evolution.Document5 pagesPoka-Yoke or Mistake Proofing: Historical Evolution.Harris ChackoPas encore d'évaluation

- CP3 - June2019 2Document5 pagesCP3 - June2019 2Sifei ZhangPas encore d'évaluation

- HC+ Shoring System ScaffoldDocument31 pagesHC+ Shoring System ScaffoldShafiqPas encore d'évaluation

- Science Grade 10 (Exam Prep)Document6 pagesScience Grade 10 (Exam Prep)Venice Solver100% (3)