Vous aimerez peut-être aussi

- 2015: Outlook for Stocks, Bonds, Commodities, Currencies and Real EstateD'Everand2015: Outlook for Stocks, Bonds, Commodities, Currencies and Real EstatePas encore d'évaluation

- Westpac WeeklyDocument10 pagesWestpac WeeklysugengPas encore d'évaluation

- DI Canada OutlookDocument8 pagesDI Canada OutlookGeorge KapellosPas encore d'évaluation

- India Investment Strategy - November 18Document26 pagesIndia Investment Strategy - November 18shahavPas encore d'évaluation

- Peru Economic Outlook 1Q17Document30 pagesPeru Economic Outlook 1Q17Deepak SamavedamPas encore d'évaluation

- Swiss Re Canada Economic Outlook 3Q19Document2 pagesSwiss Re Canada Economic Outlook 3Q19Fox WalkerPas encore d'évaluation

- Recent Economic Developments in Singapore: 5 September 2017Document20 pagesRecent Economic Developments in Singapore: 5 September 2017Aroos AhmadPas encore d'évaluation

- Economic Outlook - Risk Is A Sharper-Than-Expected Slowdown in in The 2H, Not A Double Dip - 18/6/2010Document14 pagesEconomic Outlook - Risk Is A Sharper-Than-Expected Slowdown in in The 2H, Not A Double Dip - 18/6/2010Rhb InvestPas encore d'évaluation

- Deloitte Au Cip Tourism Hotel Outlook Edition 1 2019 120419Document13 pagesDeloitte Au Cip Tourism Hotel Outlook Edition 1 2019 120419deadlsweetyPas encore d'évaluation

- WTO Trade Statistics and Outlook April 2017Document21 pagesWTO Trade Statistics and Outlook April 2017Coleman NeePas encore d'évaluation

- Economic Outlook 2016 12Document13 pagesEconomic Outlook 2016 12vae2797Pas encore d'évaluation

- Ups and Downs: Inside..Document9 pagesUps and Downs: Inside..buddhacrisPas encore d'évaluation

- Global inflation outlook and monetary policy challengesDocument4 pagesGlobal inflation outlook and monetary policy challengesUneth CityPas encore d'évaluation

- Director ReportDocument48 pagesDirector ReportAakash DasPas encore d'évaluation

- Performance of Debt Markt: An Article ReviewDocument11 pagesPerformance of Debt Markt: An Article ReviewNida SubhaniPas encore d'évaluation

- Global Economic ResearchDocument6 pagesGlobal Economic ResearchAndyPas encore d'évaluation

- Us Real Estate Outlook 2018Document28 pagesUs Real Estate Outlook 2018gollumPas encore d'évaluation

- BRICS Economies: An AnalysisDocument6 pagesBRICS Economies: An AnalysismilagrosPas encore d'évaluation

- Mid-Year Investment Outlook For 2023Document14 pagesMid-Year Investment Outlook For 2023ShreyPas encore d'évaluation

- MI WP YearAhead2023 PDFDocument13 pagesMI WP YearAhead2023 PDFJPas encore d'évaluation

- ARTICLEDocument2 pagesARTICLEMj BollenaPas encore d'évaluation

- Weo Update July 2017 PDFDocument7 pagesWeo Update July 2017 PDFhgfed4321Pas encore d'évaluation

- Statement of The Monetary Policy Committee - 24 January 2017Document10 pagesStatement of The Monetary Policy Committee - 24 January 2017Tiso Blackstar GroupPas encore d'évaluation

- Crisil Sme Connect Feb10Document36 pagesCrisil Sme Connect Feb10ramanindiaPas encore d'évaluation

- US Economic Outlook - For 2017 and BeyondDocument6 pagesUS Economic Outlook - For 2017 and BeyondpiyushPas encore d'évaluation

- Croatia GDP Growth to Remain Strong Despite RisksDocument2 pagesCroatia GDP Growth to Remain Strong Despite RisksHasan DelibaltaPas encore d'évaluation

- Swedbank Economic Outlook Update, November 2015Document17 pagesSwedbank Economic Outlook Update, November 2015Swedbank AB (publ)Pas encore d'évaluation

- Directors' Report: I. Economic Backdrop and Banking EnvironmentDocument53 pagesDirectors' Report: I. Economic Backdrop and Banking EnvironmentPuja BhallaPas encore d'évaluation

- Oct 21st Bank of Canada Rate AnnouncementDocument2 pagesOct 21st Bank of Canada Rate AnnouncementMortgage ResourcesPas encore d'évaluation

- Factors Affecting Investments in Pakistan's EconomyDocument7 pagesFactors Affecting Investments in Pakistan's EconomyHome PhonePas encore d'évaluation

- Asian Development Outlook: Paths Diverge in Recovery From The PandemicDocument7 pagesAsian Development Outlook: Paths Diverge in Recovery From The PandemicChea ChetraPas encore d'évaluation

- Chinese Economy - Macroeconomic Analysis For Tesla's Investment DecisionDocument6 pagesChinese Economy - Macroeconomic Analysis For Tesla's Investment DecisionVrajesh ChitaliaPas encore d'évaluation

- NZ Economic OutlookDocument15 pagesNZ Economic OutlookJohn ChoiPas encore d'évaluation

- Crisil Ecoview: March 2010Document32 pagesCrisil Ecoview: March 2010Aparajita BasakPas encore d'évaluation

- Nedbank Se Rentekoers-Barometer Vir Mei 2016Document4 pagesNedbank Se Rentekoers-Barometer Vir Mei 2016Netwerk24SakePas encore d'évaluation

- BC - Projects Portfolio Overview - Oct - LR1 Austrialia Hotel GroupDocument39 pagesBC - Projects Portfolio Overview - Oct - LR1 Austrialia Hotel GroupEshwar KumarPas encore d'évaluation

- Australia and New ZealandDocument11 pagesAustralia and New ZealandedgarmerchanPas encore d'évaluation

- PreBudgetExpectations2011-12 Anagram 180211Document18 pagesPreBudgetExpectations2011-12 Anagram 180211chaterji_aPas encore d'évaluation

- SEB Report: Asian Recovery - Please Hold The LineDocument9 pagesSEB Report: Asian Recovery - Please Hold The LineSEB GroupPas encore d'évaluation

- Happy New Year?: Liftoff!Document1 pageHappy New Year?: Liftoff!babbabeuPas encore d'évaluation

- Philippine Economy Growth Slows in 2019 but Poverty Reduction ContinuesDocument5 pagesPhilippine Economy Growth Slows in 2019 but Poverty Reduction ContinuesMichaelAngeloBattungPas encore d'évaluation

- In Union Budget 2023 Detailed Analysis NoexpDocument78 pagesIn Union Budget 2023 Detailed Analysis NoexppatrodeskPas encore d'évaluation

- Crisil Sme Connect Dec09Document32 pagesCrisil Sme Connect Dec09Rahul JainPas encore d'évaluation

- Natixis Asia 2020 Outlook: Growth Still Slowing: C2 - Inter Nal NatixisDocument2 pagesNatixis Asia 2020 Outlook: Growth Still Slowing: C2 - Inter Nal NatixisAlezNgPas encore d'évaluation

- March Market Outlook: Equities & Commodities Under PressureDocument8 pagesMarch Market Outlook: Equities & Commodities Under PressureMoed D'lhoxPas encore d'évaluation

- Americas: Economic Review January 2011: at A GlanceDocument9 pagesAmericas: Economic Review January 2011: at A Glancemathew_rexPas encore d'évaluation

- Country Report India February 2022Document5 pagesCountry Report India February 2022Daniel DannyPas encore d'évaluation

- GX Global Powers of Retailing 2022Document52 pagesGX Global Powers of Retailing 2022Ngoc Ngan LyPas encore d'évaluation

- WEOupdateJan2019 PDFDocument8 pagesWEOupdateJan2019 PDFsalt1322Pas encore d'évaluation

- Annual ReportDocument10 pagesAnnual Reportcharu555Pas encore d'évaluation

- JPM2019-09 MI - 2020outlook - 112719Document12 pagesJPM2019-09 MI - 2020outlook - 112719RyanPas encore d'évaluation

- Statement by Philip Lowe, Governor: Monetary Policy Decision - Media Releases - RBADocument3 pagesStatement by Philip Lowe, Governor: Monetary Policy Decision - Media Releases - RBATraderPas encore d'évaluation

- Through The Looking Glass Chinas 2023 GDP and The Year AheadDocument11 pagesThrough The Looking Glass Chinas 2023 GDP and The Year Aheadt8enedPas encore d'évaluation

- Subsidiaries of Icici Bank Ar Fy2018Document512 pagesSubsidiaries of Icici Bank Ar Fy2018AladdinPas encore d'évaluation

- Global Economic Outlook1Document2 pagesGlobal Economic Outlook1Harry CerqueiraPas encore d'évaluation

- Monetary Policy Report - CanadaDocument12 pagesMonetary Policy Report - CanadaHeenaPas encore d'évaluation

- BC Economic Forecast BC Economic Forecast 2013-17013-17 - Feb13Document15 pagesBC Economic Forecast BC Economic Forecast 2013-17013-17 - Feb13pikevrPas encore d'évaluation

- What Is The Outlook For BRICsDocument7 pagesWhat Is The Outlook For BRICstrolaiPas encore d'évaluation

- 2023 AsiaDocument8 pages2023 AsiaJuan LaredoPas encore d'évaluation

- MPR NOV 2017 - v3Document36 pagesMPR NOV 2017 - v3Rossana CairaPas encore d'évaluation

- Wbc-Ec 2020Document6 pagesWbc-Ec 2020mrfutschPas encore d'évaluation

- Ops PDFDocument43 pagesOps PDFmrfutschPas encore d'évaluation

- Bank Pac WeeklyDocument14 pagesBank Pac WeeklymrfutschPas encore d'évaluation

- Aus Chamber Westpac 2018 Q2Document14 pagesAus Chamber Westpac 2018 Q2mrfutschPas encore d'évaluation

- China Economic Update 15 April 2019Document3 pagesChina Economic Update 15 April 2019mrfutschPas encore d'évaluation

- ANU Key Dates WestpacDocument1 pageANU Key Dates WestpacmrfutschPas encore d'évaluation

- Eoy Doc 2018 PDFDocument3 pagesEoy Doc 2018 PDFmrfutschPas encore d'évaluation

- NAB CEO Press Conference Transcript PDFDocument4 pagesNAB CEO Press Conference Transcript PDFmrfutschPas encore d'évaluation

- ANZ Media CommentsDocument3 pagesANZ Media CommentsmrfutschPas encore d'évaluation

- 2018 ANZ Stadium Event Calendar: A-League, NRL, Concerts & MoreDocument1 page2018 ANZ Stadium Event Calendar: A-League, NRL, Concerts & MoremrfutschPas encore d'évaluation

- NAB Residential Property Survey Q1 2018Document11 pagesNAB Residential Property Survey Q1 2018mrfutschPas encore d'évaluation

- 2018 ANZ Stadium Event Calendar: A-League, NRL, Concerts & MoreDocument1 page2018 ANZ Stadium Event Calendar: A-League, NRL, Concerts & MoremrfutschPas encore d'évaluation

- West Pac WeeklyDocument12 pagesWest Pac WeeklymrfutschPas encore d'évaluation

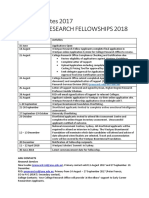

- Mailer 2017 Westpac Research Fellowships Opening of ApplicationsDocument1 pageMailer 2017 Westpac Research Fellowships Opening of ApplicationsmrfutschPas encore d'évaluation

- ANZ Subordinated Offer DocumentDocument99 pagesANZ Subordinated Offer DocumentmrfutschPas encore d'évaluation

- Australian Markets Weekly: Underemployment Dragging On Wages GrowthDocument6 pagesAustralian Markets Weekly: Underemployment Dragging On Wages GrowthmrfutschPas encore d'évaluation

- Westpac Future Leaders Scholarship Presentation 2016Document7 pagesWestpac Future Leaders Scholarship Presentation 2016mrfutschPas encore d'évaluation

- US Economic Update Points to Stronger Growth in Q2 2017Document5 pagesUS Economic Update Points to Stronger Growth in Q2 2017mrfutschPas encore d'évaluation

- Westpac Group Financial CalendarDocument4 pagesWestpac Group Financial CalendarmrfutschPas encore d'évaluation

- Budget PaperDocument308 pagesBudget PapermrfutschPas encore d'évaluation

- RandDocument9 pagesRandalfredPas encore d'évaluation

- West Pac WeeklyDocument10 pagesWest Pac WeeklymrfutschPas encore d'évaluation

- Cults of Cthulhu - H.P. Lovecraft and The Occult TraditionDocument26 pagesCults of Cthulhu - H.P. Lovecraft and The Occult TraditionTsigalko77100% (2)

- Teaching and Learning 21st Century SkillsDocument37 pagesTeaching and Learning 21st Century SkillsMac SensPas encore d'évaluation

- Dagon Rising - The Litany of Dagon by Phil HineDocument28 pagesDagon Rising - The Litany of Dagon by Phil HineDru De Nicola De Nicola100% (1)

- Parent Orientation Powerpoint-2013-2014 PreschoolDocument46 pagesParent Orientation Powerpoint-2013-2014 PreschoolmrfutschPas encore d'évaluation

- Quotes HieroclesDocument1 pageQuotes HieroclesmrfutschPas encore d'évaluation

- Economic OutlookDocument70 pagesEconomic OutlookmrfutschPas encore d'évaluation

- Chapter1 - Fundamental Principles of ValuationDocument21 pagesChapter1 - Fundamental Principles of ValuationだみPas encore d'évaluation

- MOTIVATION - Strategy For UPSC Mains and Tips For Answer Writing - Kumar Ashirwad, Rank 35 CSE - 2015 - InSIGHTSDocument28 pagesMOTIVATION - Strategy For UPSC Mains and Tips For Answer Writing - Kumar Ashirwad, Rank 35 CSE - 2015 - InSIGHTSDhiraj Kumar PalPas encore d'évaluation

- 03-F05 Critical Task Analysis - DAMMAMDocument1 page03-F05 Critical Task Analysis - DAMMAMjawad khanPas encore d'évaluation

- PRMG 6007 - Procurement Logistics and Contracting Uwi Exam Past Paper 2012Document3 pagesPRMG 6007 - Procurement Logistics and Contracting Uwi Exam Past Paper 2012tilshilohPas encore d'évaluation

- Contact Sushant Kumar Add Sushant Kumar To Your NetworkDocument2 pagesContact Sushant Kumar Add Sushant Kumar To Your NetworkJaspreet Singh SahaniPas encore d'évaluation

- PsychographicsDocument12 pagesPsychographicsirenek100% (2)

- HR ManagementDocument7 pagesHR ManagementAravind 9901366442 - 9902787224Pas encore d'évaluation

- Contract: Organisation Details Buyer DetailsDocument4 pagesContract: Organisation Details Buyer DetailsMukhiya HaiPas encore d'évaluation

- Role of Market ResearchDocument2 pagesRole of Market ResearchGaurav AgarwalPas encore d'évaluation

- Subcontracting Process in Production - SAP BlogsDocument12 pagesSubcontracting Process in Production - SAP Blogsprasanna0788Pas encore d'évaluation

- Jay Abraham - Let Them Buy Over TimeDocument2 pagesJay Abraham - Let Them Buy Over TimeAmerican Urban English LoverPas encore d'évaluation

- Acca FeeDocument2 pagesAcca FeeKamlendran BaradidathanPas encore d'évaluation

- NSU FALL 2012 FIN254.9 Term Paper On Aramit LimitedDocument24 pagesNSU FALL 2012 FIN254.9 Term Paper On Aramit LimitedSamaan RishadPas encore d'évaluation

- Theory of Value - A Study of Pre-Classical, Classical andDocument11 pagesTheory of Value - A Study of Pre-Classical, Classical andARKA DATTAPas encore d'évaluation

- Non Disclosure AgreementDocument2 pagesNon Disclosure AgreementReginaldo BucuPas encore d'évaluation

- Partnership Worksheet 7Document4 pagesPartnership Worksheet 7Timo wernerePas encore d'évaluation

- International Trade Statistics YearbookDocument438 pagesInternational Trade Statistics YearbookJHON ALEXIS VALENCIA MENESESPas encore d'évaluation

- Medical Insurance Premium Receipt 2019-20Document4 pagesMedical Insurance Premium Receipt 2019-20Himanshu Tater43% (7)

- Résumé Rodrigo Marcelo Irribarra CartesDocument3 pagesRésumé Rodrigo Marcelo Irribarra CartesRodrigo IrribarraPas encore d'évaluation

- Business Continuity Plan 2023Document8 pagesBusiness Continuity Plan 2023asdasdPas encore d'évaluation

- Operations Management Syllabus for Kelas Reguler 60 BDocument4 pagesOperations Management Syllabus for Kelas Reguler 60 BSeftian MuhardyPas encore d'évaluation

- My Project Report On Reliance FreshDocument67 pagesMy Project Report On Reliance FreshRajkumar Sababathy0% (1)

- Banglalink (Final)Document42 pagesBanglalink (Final)Zaki Ahmad100% (1)

- JDA Demand - Focus 2012Document43 pagesJDA Demand - Focus 2012Abbas Ali Shirazi100% (1)

- Human Resourse Management 1Document41 pagesHuman Resourse Management 1Shakti Awasthi100% (1)

- Cases in Civil ProcedureDocument3 pagesCases in Civil ProcedureJaayPas encore d'évaluation

- Google SWOT 2013Document4 pagesGoogle SWOT 2013Galih Eka PutraPas encore d'évaluation

- O2C Cycle in CloudDocument24 pagesO2C Cycle in Cloudmani100% (1)

- Application of Game TheoryDocument65 pagesApplication of Game Theorymithunsraj@gmail.com100% (2)

- Licensing ProposalDocument6 pagesLicensing ProposalKungfu SpartaPas encore d'évaluation

- The Coaching Habit: Say Less, Ask More & Change the Way You Lead ForeverD'EverandThe Coaching Habit: Say Less, Ask More & Change the Way You Lead ForeverÉvaluation : 4.5 sur 5 étoiles4.5/5 (186)

- Scaling Up: How a Few Companies Make It...and Why the Rest Don't, Rockefeller Habits 2.0D'EverandScaling Up: How a Few Companies Make It...and Why the Rest Don't, Rockefeller Habits 2.0Pas encore d'évaluation

- Leadership Skills that Inspire Incredible ResultsD'EverandLeadership Skills that Inspire Incredible ResultsÉvaluation : 4.5 sur 5 étoiles4.5/5 (11)

- Transformed: Moving to the Product Operating ModelD'EverandTransformed: Moving to the Product Operating ModelÉvaluation : 4 sur 5 étoiles4/5 (1)

- How to Lead: Wisdom from the World's Greatest CEOs, Founders, and Game ChangersD'EverandHow to Lead: Wisdom from the World's Greatest CEOs, Founders, and Game ChangersÉvaluation : 4.5 sur 5 étoiles4.5/5 (94)

- The First Minute: How to start conversations that get resultsD'EverandThe First Minute: How to start conversations that get resultsÉvaluation : 4.5 sur 5 étoiles4.5/5 (55)

- How to Talk to Anyone at Work: 72 Little Tricks for Big Success Communicating on the JobD'EverandHow to Talk to Anyone at Work: 72 Little Tricks for Big Success Communicating on the JobÉvaluation : 4.5 sur 5 étoiles4.5/5 (36)

- Spark: How to Lead Yourself and Others to Greater SuccessD'EverandSpark: How to Lead Yourself and Others to Greater SuccessÉvaluation : 4.5 sur 5 étoiles4.5/5 (130)

- How the World Sees You: Discover Your Highest Value Through the Science of FascinationD'EverandHow the World Sees You: Discover Your Highest Value Through the Science of FascinationÉvaluation : 4 sur 5 étoiles4/5 (7)

- The 7 Habits of Highly Effective PeopleD'EverandThe 7 Habits of Highly Effective PeopleÉvaluation : 4 sur 5 étoiles4/5 (2564)

- 7 Principles of Transformational Leadership: Create a Mindset of Passion, Innovation, and GrowthD'Everand7 Principles of Transformational Leadership: Create a Mindset of Passion, Innovation, and GrowthÉvaluation : 5 sur 5 étoiles5/5 (51)

- Billion Dollar Lessons: What You Can Learn from the Most Inexcusable Business Failures of the Last Twenty-five YearsD'EverandBillion Dollar Lessons: What You Can Learn from the Most Inexcusable Business Failures of the Last Twenty-five YearsÉvaluation : 4.5 sur 5 étoiles4.5/5 (52)

- The Introverted Leader: Building on Your Quiet StrengthD'EverandThe Introverted Leader: Building on Your Quiet StrengthÉvaluation : 4.5 sur 5 étoiles4.5/5 (35)

- Work Stronger: Habits for More Energy, Less Stress, and Higher Performance at WorkD'EverandWork Stronger: Habits for More Energy, Less Stress, and Higher Performance at WorkÉvaluation : 4.5 sur 5 étoiles4.5/5 (12)

- Transformed: Moving to the Product Operating ModelD'EverandTransformed: Moving to the Product Operating ModelÉvaluation : 4 sur 5 étoiles4/5 (1)

- The 4 Disciplines of Execution: Revised and Updated: Achieving Your Wildly Important GoalsD'EverandThe 4 Disciplines of Execution: Revised and Updated: Achieving Your Wildly Important GoalsÉvaluation : 4.5 sur 5 étoiles4.5/5 (48)

- The 12 Week Year: Get More Done in 12 Weeks than Others Do in 12 MonthsD'EverandThe 12 Week Year: Get More Done in 12 Weeks than Others Do in 12 MonthsÉvaluation : 4.5 sur 5 étoiles4.5/5 (411)

- Unlocking Potential: 7 Coaching Skills That Transform Individuals, Teams, & OrganizationsD'EverandUnlocking Potential: 7 Coaching Skills That Transform Individuals, Teams, & OrganizationsÉvaluation : 4.5 sur 5 étoiles4.5/5 (27)

- Get Scalable: The Operating System Your Business Needs To Run and Scale Without YouD'EverandGet Scalable: The Operating System Your Business Needs To Run and Scale Without YouÉvaluation : 5 sur 5 étoiles5/5 (1)

- The Power of People Skills: How to Eliminate 90% of Your HR Problems and Dramatically Increase Team and Company Morale and PerformanceD'EverandThe Power of People Skills: How to Eliminate 90% of Your HR Problems and Dramatically Increase Team and Company Morale and PerformanceÉvaluation : 5 sur 5 étoiles5/5 (22)

- The 12 Week Year: Get More Done in 12 Weeks than Others Do in 12 MonthsD'EverandThe 12 Week Year: Get More Done in 12 Weeks than Others Do in 12 MonthsÉvaluation : 4.5 sur 5 étoiles4.5/5 (90)

- Summary: Choose Your Enemies Wisely: Business Planning for the Audacious Few: Key Takeaways, Summary and AnalysisD'EverandSummary: Choose Your Enemies Wisely: Business Planning for the Audacious Few: Key Takeaways, Summary and AnalysisÉvaluation : 4.5 sur 5 étoiles4.5/5 (3)

- Sustainability Management: Global Perspectives on Concepts, Instruments, and StakeholdersD'EverandSustainability Management: Global Perspectives on Concepts, Instruments, and StakeholdersÉvaluation : 5 sur 5 étoiles5/5 (1)

- The Little Big Things: 163 Ways to Pursue ExcellenceD'EverandThe Little Big Things: 163 Ways to Pursue ExcellencePas encore d'évaluation

- Management Mess to Leadership Success: 30 Challenges to Become the Leader You Would FollowD'EverandManagement Mess to Leadership Success: 30 Challenges to Become the Leader You Would FollowÉvaluation : 4.5 sur 5 étoiles4.5/5 (27)