Vous aimerez peut-être aussi

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Drastic - Wireless Network Site Survey Form Rev1Document11 pagesDrastic - Wireless Network Site Survey Form Rev1Michell AntunesPas encore d'évaluation

- BVCA Guide To Corporate Venture CapitalDocument16 pagesBVCA Guide To Corporate Venture CapitalPeter PandaPas encore d'évaluation

- Ieee Standard For Interconnection and Interoperability of DistriDocument138 pagesIeee Standard For Interconnection and Interoperability of DistriDouglas Silva50% (2)

- Absolyte Engineering PDFDocument110 pagesAbsolyte Engineering PDFwizlishPas encore d'évaluation

- Report On Smart GridsDocument16 pagesReport On Smart GridsTeja Dhft NtrPas encore d'évaluation

- Smart Grid in TransmissionDocument46 pagesSmart Grid in TransmissionAnil PalamwarPas encore d'évaluation

- What Happens To Chinese Oil If US-North Korea War Erupts - This Week in Asia - South China Morning PostDocument6 pagesWhat Happens To Chinese Oil If US-North Korea War Erupts - This Week in Asia - South China Morning PostPeter PandaPas encore d'évaluation

- Characteristics: C5 Petrochemical ProductDocument3 pagesCharacteristics: C5 Petrochemical ProductPeter PandaPas encore d'évaluation

- 2017 MIP Report China Online EdtechDocument29 pages2017 MIP Report China Online EdtechPeter PandaPas encore d'évaluation

- North Korea Conflict: International Industry Research and Economics DepartmentDocument9 pagesNorth Korea Conflict: International Industry Research and Economics DepartmentPeter PandaPas encore d'évaluation

- IO Ethanol 2018 enDocument7 pagesIO Ethanol 2018 enPeter PandaPas encore d'évaluation

- mati08-2537 มติคณะกรรมการสิ่งแวดล้อมDocument4 pagesmati08-2537 มติคณะกรรมการสิ่งแวดล้อมPeter PandaPas encore d'évaluation

- News Articles 2018-01-16 The-Flow-OfDocument5 pagesNews Articles 2018-01-16 The-Flow-OfPeter PandaPas encore d'évaluation

- Christie's Launches Sale of Western Art in Hong Kong To Test Asian Demand - South China Morning PostDocument3 pagesChristie's Launches Sale of Western Art in Hong Kong To Test Asian Demand - South China Morning PostPeter PandaPas encore d'évaluation

- Shell Marine Imo BrochureDocument6 pagesShell Marine Imo BrochurePeter PandaPas encore d'évaluation

- Thai NessDocument17 pagesThai NessPeter PandaPas encore d'évaluation

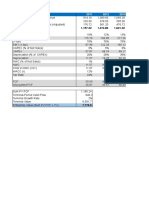

- Total Revenue 1,157.32 1,374.80 1,621.32: (Unit: Million USD)Document6 pagesTotal Revenue 1,157.32 1,374.80 1,621.32: (Unit: Million USD)Peter PandaPas encore d'évaluation

- Role Play Scenario 1:: Group No. .Document1 pageRole Play Scenario 1:: Group No. .Peter PandaPas encore d'évaluation

- LucerneDocument52 pagesLucernePeter PandaPas encore d'évaluation

- Evaluation Form For MassageDocument1 pageEvaluation Form For MassagePeter PandaPas encore d'évaluation

- Brexit: A Look at The Repercussions of Britain's Possible Exit From The European UnionDocument17 pagesBrexit: A Look at The Repercussions of Britain's Possible Exit From The European UnionPeter PandaPas encore d'évaluation

- BSC Thesis Electrical EngineeringDocument6 pagesBSC Thesis Electrical EngineeringWhitney Anderson100% (1)

- Modern Hydroelectric Engineering Practice in India Electro-Mechanical WorksDocument10 pagesModern Hydroelectric Engineering Practice in India Electro-Mechanical WorksvenkatPas encore d'évaluation

- Smart Grid SyllabiDocument2 pagesSmart Grid SyllabiSandeep ChawdaPas encore d'évaluation

- Hopewell ('), Castro-Sayas (L), Bailey (') : Optimising The Design of Offshore Wind Farm Collection NetworksDocument5 pagesHopewell ('), Castro-Sayas (L), Bailey (') : Optimising The Design of Offshore Wind Farm Collection NetworksAmmar LateefPas encore d'évaluation

- A Control Methodology of Three Phase Grid Connected PV SystemDocument8 pagesA Control Methodology of Three Phase Grid Connected PV SystemBojan BankovicPas encore d'évaluation

- Wind Energy ProjectDocument17 pagesWind Energy ProjectOmer DhillownPas encore d'évaluation

- A Smart Iot Based System For Monitoring and Controlling The TransformersDocument5 pagesA Smart Iot Based System For Monitoring and Controlling The TransformersAiman AyyubPas encore d'évaluation

- Power Intruption 1Document5 pagesPower Intruption 1yalewlet tarekeggnPas encore d'évaluation

- Energies: AC Transmission Emulation Control Strategies For The BTB VSC HVDC System in The Metropolitan Area of SeoulDocument15 pagesEnergies: AC Transmission Emulation Control Strategies For The BTB VSC HVDC System in The Metropolitan Area of Seoulnikon reddyPas encore d'évaluation

- Conference Guide - IsieDocument52 pagesConference Guide - IsiePaulo CesarPas encore d'évaluation

- Power Transformer Asset Management: ColumnDocument5 pagesPower Transformer Asset Management: ColumnMayur ChavdaPas encore d'évaluation

- ELK-04 C 145 2GHV008915 0315enDocument20 pagesELK-04 C 145 2GHV008915 0315enmuraliPas encore d'évaluation

- Smart Grid Concept and CharacteristicsDocument3 pagesSmart Grid Concept and CharacteristicshafizgPas encore d'évaluation

- CEP 2021 Executive Summary FINALDocument10 pagesCEP 2021 Executive Summary FINALCaleb HollowayPas encore d'évaluation

- Energy Meter ManualDocument2 pagesEnergy Meter ManualClaris muthoniPas encore d'évaluation

- Professor Massoud Amin ! Smart GridDocument4 pagesProfessor Massoud Amin ! Smart GridMassoud AminPas encore d'évaluation

- JWG Smart Grid Report - V1 0Document164 pagesJWG Smart Grid Report - V1 0sevilla00Pas encore d'évaluation

- SKEE 4653 - Chapter 1 - Introduction 20212022 1Document97 pagesSKEE 4653 - Chapter 1 - Introduction 20212022 1gdd ddPas encore d'évaluation

- WR Operating Procedure 2017Document286 pagesWR Operating Procedure 20171981todurkarPas encore d'évaluation

- EEBus UC TS ControlOfBattery V1.0.0 RC3 PublicDocument105 pagesEEBus UC TS ControlOfBattery V1.0.0 RC3 PublicWnenjin ZhangPas encore d'évaluation

- SMART GRID Seminar Report PDFDocument23 pagesSMART GRID Seminar Report PDFSaurav KumarPas encore d'évaluation

- The New EE LAW of 1995 and Other Related Laws: Learning Module 01Document24 pagesThe New EE LAW of 1995 and Other Related Laws: Learning Module 01Jimwell Arnie Dela CruzPas encore d'évaluation

- 9-AEP Smart Grid Project Overview - Tom WalkerDocument17 pages9-AEP Smart Grid Project Overview - Tom WalkerGheorghe VucPas encore d'évaluation

- Lecture 7 Integration of Renewable Energy SourcesDocument48 pagesLecture 7 Integration of Renewable Energy Sourcesas2899142Pas encore d'évaluation

- 0712 Gas InsulatedDocument7 pages0712 Gas InsulatedmohamedayazuddinPas encore d'évaluation